META – Not dead after all

Meta reported its Q4 2022 results on Feb 1st after the bell. Although the results were not great, they were good enough (especially operating expenses and capital expenses outlook) to excite investors, driving the price to over 18% higher after hours.

Key Highlights

Revenue for Q4’22 of $32.2B (down 4% compared to Q4’21 or 2% up on constant currency) beating mid-point guidance by $950M and analysts’ estimates by $475M. Q4’22 had an FX impact of negative $2B. 2022 revenues were relatively flat to $116.6B compared to $117.9B in 2021.

Operating income of $6.4B, down 49% compared to Q4’21, missing estimates by $1.15B. Operating margin was 20% compared to 37% in Q4’21. 2022 operating income declined to $28.9B (by 38%) compared to $46.8B in 2021.

GAAP EPS for Q4’22 of $1.76 (down 52% compared to Q4’21) missing estimates by $0.47. 2022 GAAP EPS declined to $8.59 (by 38%) compared to $13.77 in 2021.

Engagement

Core business is doing fine with increased engagement across Family of Apps Daily Active People (DAP) & Monthly Active People (MAP), and Facebook Daily Active Users (DAU) & Monthly Active Users (MAU).

Under a period where META was considered ‘dead’, it added 140M DAP across its Family of Apps, reaching 2.96B people and 71M DAU on Facebook platform, reaching 2B.

Comparing this to the 56 million DAU added on Snap (total DAU are 375M) one can understand if Facebook remains relevant.

Source: META Earnings presentations, StockOpine analysis

One of the key drivers of engagement is the recommendation engine powered by AI on Facebook and Instagram as people see what interests them the most. At least this is what they strive to achieve. For 2023, the expectation is that 30%-40% of the overall feed will be recommended content.

Revenues & Profitability

Revenue

Family of Apps (“FoA”) revenue of $31.4B declined by 4%, whereas Reality Labs revenue declined to $727M or 17%. Regarding advertising revenue, the company saw strength in travel and healthcare verticals and a significant decline in technology and financial services.

Q4 ad-impressions increased by 23% but price per ad decreased by 22%. This was driven by both lower demand and currency as well as strong impression growth in Rest of World and Asia Pacific.

We do not feel that this is an issue as lower demand is justified by the current environment whereas impression growth in areas with lower monetization provides opportunities for future growth.

For instance, Facebook ARPU ($3.52 RoW, $4.61 in Asia-Pacific) is just a fraction of North America Average Revenue per User of $58.77.

Outlook: Q1’23 Revenue guidance is $26-$28.5B or a 2% decline y/y with a c. 2% FX headwind.

Profitability

Lower operating income of $6.4B (Vs $12.6B) and operating margin of 20% (Vs 37%), were mainly impacted by a 31% increase in cost of sales (write-down of data center assets and growth in infrastructure related expenses) and 39% increase in R&D (lease impairments and employee related costs).

Source: META Earnings presentations, StockOpine analysis

Payroll was still a pressure on Q4 profits due to the inclusion of employees who were laid off. These will not be included in Q1.

META recognized significant restructuring amounts of $4.2B, relating to layoffs, consolidating office facilities and streamlining of future data centers. Excluding these amounts margin would have been 13% higher or 33%.

As good as it sounds, one should not ignore that they got it wrong and this was a cost to the shareholders. However, accepting mistakes and addressing them is a positive attribute. For 2023, a $1B restructuring expense is expected due to offices consolidation.

Outlook: The guidance for total expenses in 2023 was reduced from $94B-$100B to $89B-$95B due to lower payroll growth, restructuring cost and cost of revenue.

One factor contributing to the reduction in cost of revenues is the extension of the useful life of non-AI servers and that’s having an impact of over $1B as implied by Susan Li, CFO. Not really an actual saving.

Management is giving shareholders what they want to hear, changing the perception about the future of the company. Mark Zuckerberg, CEO

“Now before getting into our product priorities, I want to discuss my management theme for 2023, which is the Year of Efficiency.”

“we’re going to be more proactive about cutting projects that aren't performing or may no longer be as crucial, but my main focus is on increasing the efficiency of how we execute our top priorities.”

Don’t be fooled. These costs are still higher compared to 2022 and although Management will try to be efficient, long-term investments should be made to maintain its market position (AI, and potentially generative AI) or to achieve its long term aspirations (Reality Labs). Be ready to see fluctuations and appreciate the fact that long-term investments have long-term (not short-term) results.

Reality labs

Year of Efficiency does not mean less RL spending. RL total operating losses for 2022 were $13.7B up from $10.2B in 2021 and management still expects to continue invest meaningfully in 2023, in line with earlier comments.

For context: Zuck breaks Reality Labs into 3 areas a) Augmented reality, biggest area but still at research phase, b) Virtual Reality that starts to ramp up (Quest 2, Quest Pro) and c) Metaverse software which is critical but the less capital intensive.

Source: META Earnings presentations, StockOpine analysis

Reels

Reels are becoming increasingly important and management continues to see improvements in monetization. They did not update us on the $3B run rate provided last quarter for Instagram and Facebook but they noted that over 40% of advertisers use Reels, monetization doubled in the last 6 months and Reels are close to be revenue neutral by the end of the year/early next year (currently is a headwind).

Mark Zuckerberg, CEO “But at this point, we're at pretty good scale. So I think for now, the right thing to do is to work on monetization efficiency.”

“But we are especially focused on short-form video since Reels is growing so quickly. And I am really proud of our progress here. Reels plays across Facebook and Instagram have more than doubled over the last year, while the social component of people resharing Reels has grown even faster and has more than doubled on both apps in just the last 6 months.”

Javier Olivan, COO “And we've been making good progress with now over 40% of our advertisers use Reels ads across our apps.”

WhatsApp / Business Messaging

Another critical pillar of META is click-to-message ads which are now on a $10B run rate, up from $9B disclosed in last quarter, with developing markets being the key driver. As explained by Susan Li, CFO, this is not only WhatsApp but includes click-to-Messenger and click-to-IG Direct, disclosing that IG direct is the smallest. For the record, in prior quarter $1.5B run-rate was derived from Click-to-WhatsApp.

Susan Li, CFO “Click-to-message ads continue to grow quickly and we believe they’re bringing incremental demand onto our platform, with over half of Click-to-Message advertisers exclusively using click-to-messaging ads on our platform.”

Paid messaging is still at the early innings but it’s a huge opportunity.

“Businesses often tell us that more people open their messages and they get better results on WhatsApp than other channels.”, Mark Zuckerberg, CEO

Financial position, share buybacks and cash flows

Meta has $40.7B cash & marketable securities and $26.6B debt (including leases of $16.7B).

Cash flow from operating activities was $14.5B (45.1% of revenue) in Q4’2022 compared to $18.1B in Q4’2021 (53.8% of revenue) whereas free cash flow was $5.3B (16.4% of revenue) compared to $12.6B in Q4’2021 (37.3% of revenue).

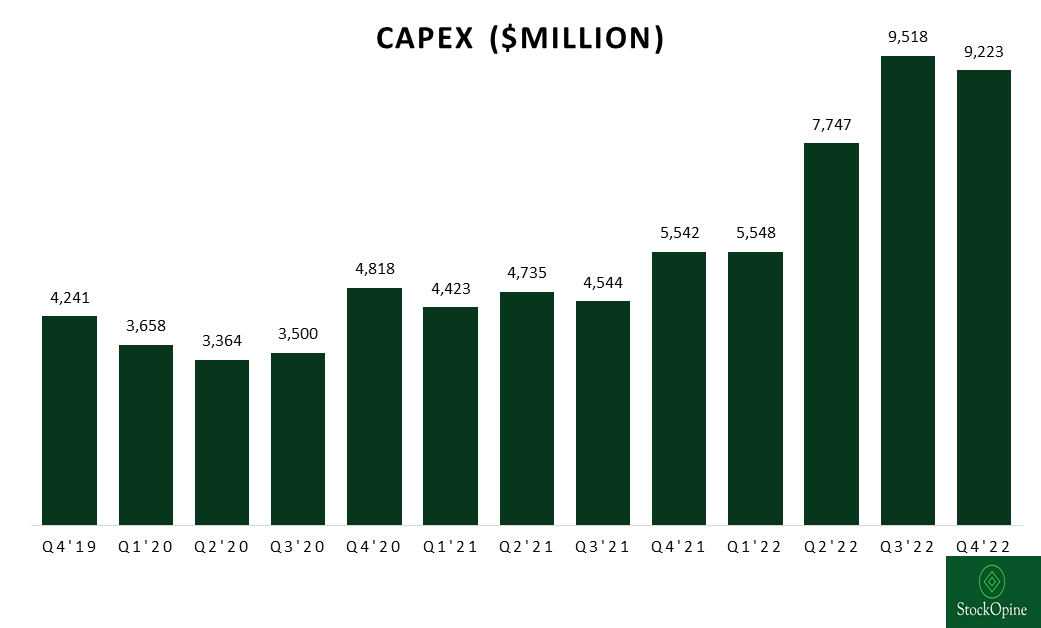

FCF was affected by the substantial increase in CAPEX to $9.2B, up by 66% y/y (relates to servers, data centers and network Infrastructure) and the reduced operating cashflow (due to the substantial reduction in operating income).

Outlook: CAPEX 2023 outlook was reduced from $34B-$37B to $30-$33B mainly due to lower data center spend as a result of changes in architecture (see restructuring costs above). These changes are likely to have a positive impact on the future as well. Substantially all CAPEX relates to FoA.

It appears that AI investments do result to improvements in ads business “as advertisers saw over 20% more conversions than in the year before. And combined with a declining cost per acquisition, this has resulted in higher returns on ad spend.

Source: META Earnings presentations, StockOpine analysis

During the quarter $6.9B shares were repurchased ($27.9B for 2022), with $10.9B available for repurchase. An additional $40B were authorized for share repurchases.

Doing a rough calculation using analysts’ estimated revenue for 2023, i.e. $122B and deducting mid-point guidance of operating expenses and CAPEX we get to a negative free cash flow.

Concluding remarks

Management, after the November layoffs, shows once again that no investment comes at all costs and while it has to invest to maintain its position and overcome challenges such as ATT (App tracking transparency) and macro environment, spending will be more focused. Nevertheless, we do realize that 2023 can be a year of negative free cash flows.

Combining the cost strategy with the increase in users across all platforms, the possibility of Reels to become revenue neutral by the year-end and the upside potential of Click-to-message ads we remain bullish on META.

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.