For May’s deep dive, we’re shifting away from the technology names we've covered in the past two months (Fortinet and Intuit) and turning our focus to a company with a more straightforward retail business model. It holds a leading market position, delivers high and growing returns on invested capital, and fits well into the "boring yet reliable" type of investment we like.

This company made its way onto our watchlist after standing out in one of the various screeners we regularly run. While it may be under the radar for most investors, it's certainly not for us, since we’re based in Cyprus, where the company has a strong presence. That’s why we think it’s worth bringing to your attention.

Whether or not the stock is currently attractively priced is something we’ll explore in the valuation section, but one thing is clear: it’s a solid defensive name that deserves a spot on your radar.

Without further ado, let’s dive in.

Contents:

Key Facts

Business Overview

Management

Industry

Financial Analysis

Competitive Advantages, Opportunities and Risks

Valuation

Conclusion

1. Key Facts

Description: Jumbo S.A. (Ticker: BELA - “Jumbo”, “Company”) is a leading diversified retailer known for its affordable pricing and broad product offering, primarily focused on toys, baby products, stationery, seasonal items, and home goods. The Company offers over 40,000 SKUs and operates 89 owned/leased stores across Greece, Cyprus, Bulgaria and Romania, and has presence in North Macedonia, Albania, Kosovo, Serbia, Bosnia, Montenegro and Israel through 40 franchised stores operating under the JUMBO brand.

Key Financials: Over the period FY15 to FY24, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 7.4% and operating income CAGR of 11.7%, reaching an FY24 revenue of €1.1 billion and adjusted operating income of €372 million (margin of 32.4%). Jumbo has cash and short term investments of €444.8 million compared to nil total debt and lease liabilities of €75 million.

Price & Market Cap (as of 30th May 2025): Its market cap is €3.85 billion with a 52-week low of €21.68 and a 52-week high of €29.04, whereas it currently trades at €28.62.

Valuation: Jumbo trades at a TTM EV/EBITDA of 8.2x (5 Year average of 7.2x) and a TTM EV/Sales of 3.0x (5 Year average of 2.5x).

2. Business Overview

a. The Story of Jumbo S.A.

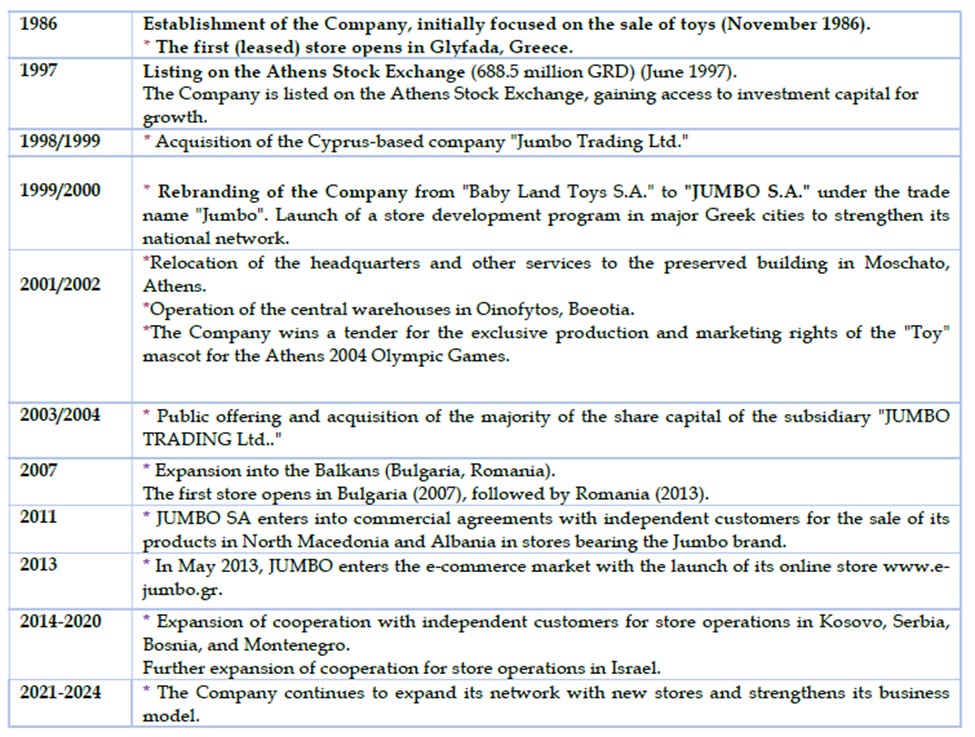

Jumbo S.A. was founded in 1986 by Apostolos Vakakis, who opened the first toy store in Glyfada. But Jumbo’s roots stretch back further, to Vakakis’s upbringing in a business-minded Greek family.

Born in Alexandria, Egypt in 1954, Vakakis came from a family that fled political unrest during the Nasser revolution, resettling in Greece in 1962. His father, George, had produced insulation materials and later worked in a toy-making workshop in Italy. This exposure led the family to establish the toy company El Greco in Greece, which Apostolos helped rebuild after a devastating fire in one of its manufacturing facilities in mid 80s. In 1985, he took over leadership of the company and eventually sold it to Hasbro in 1990, remaining involved as an executive within Hasbro Europe.

By then, Vakakis had already shifted toward retail, having founded Jumbo in 1986. With its big-box format and low-price model, the brand quickly resonated with Greek consumers. A major milestone was achieved in 1997, when Jumbo went public on the Athens Stock Exchange, enabling access to capital markets.

In 1998, it acquired Jumbo Trading Ltd in Cyprus, followed by entry into Bulgaria in 2007 and Romania in 2013. Vakakis essentially expanded into neighboring markets with cultural similarities and logistical advantages. It’s worth noting that apart from the fire during the El Greco years, bad luck struck again in 2000 when a fire destroyed Jumbo’s headquarters and warehouse. The Company then moved its base to Moschato, where it is still located today.

One of its most noticeable achievements came in 2004, when Jumbo secured exclusive rights to produce and distribute the Athens Olympic mascot, helping push annual revenues towards €500 million.

Today, the company operates 89 owned or leased stores in Greece, Cyprus, Bulgaria, and Romania, along with 40 franchised stores in Southeast Europe and Israel. Its retail model, a hypermarket without food, fashion, or electronics, features over 40,000 SKUs and continues to draw strong consumer traffic.

Source: Company’s 2024 Annual Report

Jumbo remains a family-influenced business, as Vakakis still owns 16.4% and serves as a Chairman while Vakakis’s daughter Sophia now serves on the Board as an executive member. His younger daughter Christina pursued her passion for culinary arts, while his son George tragically passed away in a car accident in 2017, a loss that deeply affected the family.

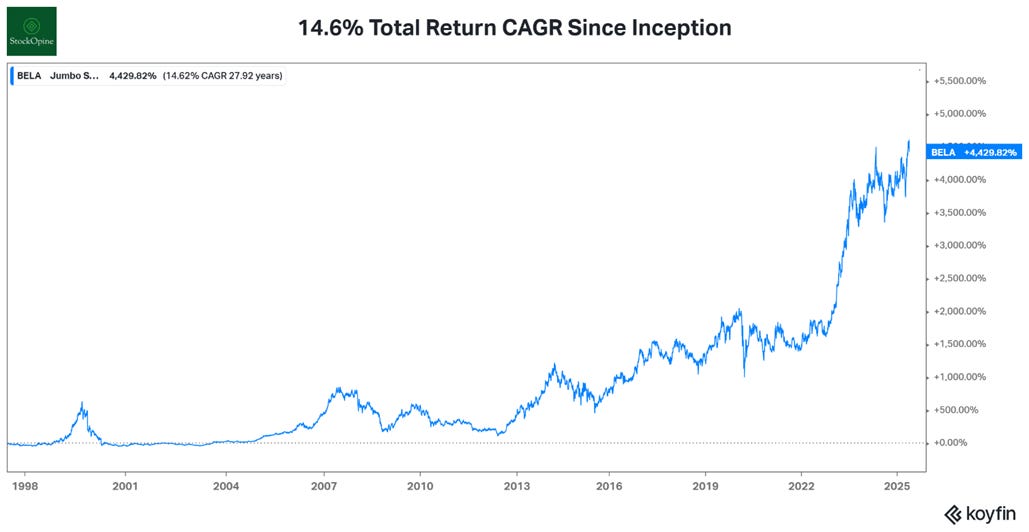

From a single toy shop to a regional retail force, Jumbo has delivered an impressive 14.6% annual total shareholder return since IPO, built on conservative growth, operational discipline, and a product mix designed to endure across cycles.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

b. Business model

Jumbo S.A. operates a value-driven retail model. From the outset, Jumbo has maintained a low-price strategy to foster trust and long-term customer loyalty. Founder Apostolos Vakakis recently reaffirmed this focus, stating:

“There's absolutely no desire to adjust prices upwards. We would be more than happy to adjust prices downwards and pass theoretical gains to our customers in order to consolidate our future…So we always have to be very careful not to create a gap.”

While primarily a retailer, Jumbo also engages in limited wholesale operations requiring strong credit histories from partners to mitigate default risk.

In recent years, Jumbo has strategically moved from leasing to owning stores to reduce operating costs. Between FY2020–FY2024, the Company acquired five previously leased stores for €39M, and most new store rollouts in 2023–2025 are company-owned. Vakakis explains:

“Leasing a store would cost us, let's say, 7.5%, 7% on the estimated value of the store, while owning the store, especially if you are liquid, is 0%.

While Vakakis prefers owning stores to avoid lease costs of 7–7.5%, this strategy draws some criticism. With returns on capital near 20%, critics argue that the capital tied up in real estate could be better used to fund growth or returned to shareholders, a classic opportunity cost trade-off. Still, this reflects Vakakis’s conservative mindset, focused on long-term cost control.

To his credit, this hasn’t limited growth or shareholder returns as Jumbo continues to pay dividends and recently started a buyback program.

Sourcing, Supply Chain & Risk Management

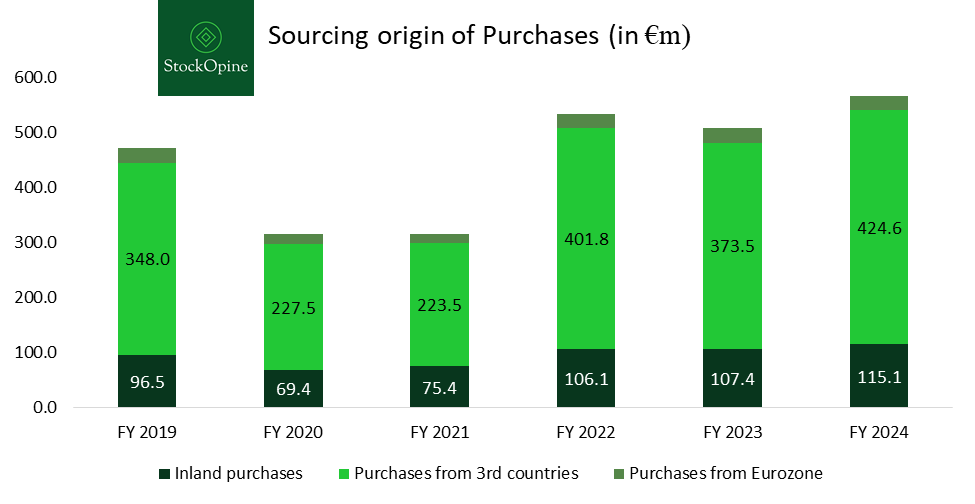

Roughly 70% of Jumbo’s products are sourced from Asia, particularly China. The Company acts as the exclusive importer for several international toy manufacturers not represented in Greece, while also purchasing from 200+ local suppliers. None of its suppliers represents more than 3% of turnover limiting concentration risk and strengthening its bargaining power.

Source: Jumbo Annual Reports, StockOpine analysis

However, the Company is not immune to global supply chain disruptions. Jumbo manages this by investing heavily in logistics infrastructure and building up inventory buffers when needed. To improve supply chain resilience, the Company owns advanced warehousing and distribution centers in Greece, Cyprus, and Romania (footprint of c. 560.000 sqm), supporting both physical and online operations. Jumbo also plans to add two new distribution hubs, one in Thessaloniki for Northern Greece/Bulgaria and another in Oinofyta for the rest of Greece and exports, with over €60M in investment over the next 3–5 years.

In the near term, the Company stands to benefit from favorable sourcing dynamics, including lower costs from Chinese suppliers and potential pricing leverage due to the US-China tariff tensions and a stronger euro. However, these tailwinds are inherently volatile and short-lived. While margins may benefit temporarily, the long-term outlook remains uncertain, reinforcing the need for supply chain agility.

Seasonality & Inventory

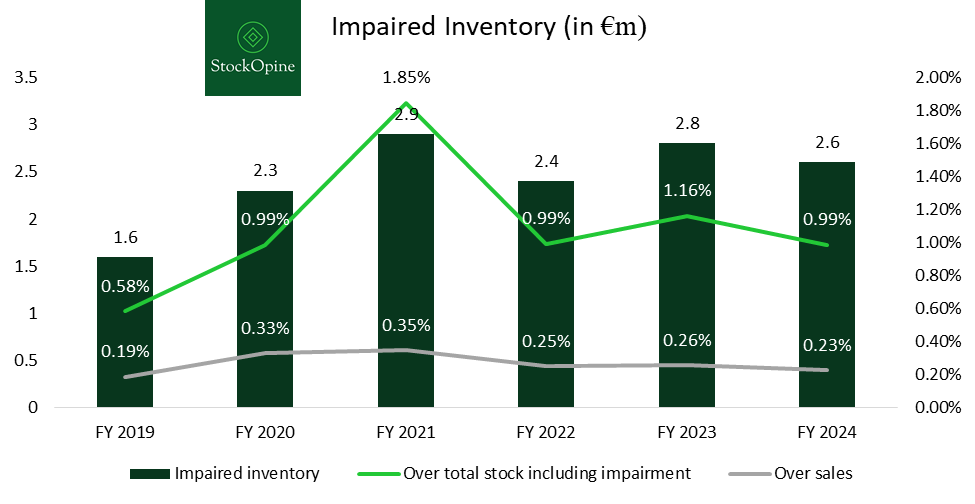

Jumbo’s sales are highly seasonal, with approximately 28% of annual revenue generated in December (Christmas), 12% in April (Easter), and 10% in September (back-to-school). This seasonality requires effective inventory management to minimize the risk of obsolete stock.

In practice, inventory write-offs remain low, highlighting Jumbo’s effective forecasting and stock control across peak periods.

Source: Jumbo Annual Reports, StockOpine analysis

Branding & Advertising

Brand recognition is a key competitive strength for Jumbo, closely associated with products for every occasion at affordable prices. The “JUMBO” brand is trademark-protected through 2032 and promoted through high-visibility TV and social media campaigns, often characterized by a clever, unconventional tone.

One standout example was the 2023 Easter campaign in Greece, where a popular singer was humorously depicted singing about the traditional Easter barbecue, on the moon, after being banished from Earth by vegans. Contradictory, yes; but undeniably effective in capturing public attention and reinforcing Jumbo’s brand visibility.

c. Geographic Segments

The Group reports four core geographical segments, namely, Greece, Cyprus, Bulgaria, and Romania. Greece remains the largest market, with 53 stores and revenue of €559.8 million (excluding franchise collaborations), accounting for 52% of the total sales mix, down from 73.3% in FY2015.

Romania has been the fastest-growing market. Since 2015, the number of stores has increased from 6 to 20, and revenue has grown from €24.3 million to €252.2 million in FY2024, reflecting a CAGR of 27.9%.

In terms of profitability, Greece leads with a gross profit margin of 56.9% in FY2024, averaging 56% over the past five years. Cyprus has the lowest, yet still healthy, margin at 52.1%, with a five-year average of 52.4%.