Not Just Toys: Jumbo's Silent Compounding Story

For May’s deep dive, we’re shifting away from the technology names we've covered in the past two months (Fortinet and Intuit) and turning our focus to a company with a more straightforward retail business model. It holds a leading market position, delivers high and growing returns on invested capital, and fits well into the "boring yet reliable" type of investment we like.

This company made its way onto our watchlist after standing out in one of the various screeners we regularly run. While it may be under the radar for most investors, it's certainly not for us, since we’re based in Cyprus, where the company has a strong presence. That’s why we think it’s worth bringing to your attention.

Whether or not the stock is currently attractively priced is something we’ll explore in the valuation section, but one thing is clear: it’s a solid defensive name that deserves a spot on your radar.

Without further ado, let’s dive in.

Contents:

Key Facts

Business Overview

Management

Industry

Financial Analysis

Competitive Advantages, Opportunities and Risks

Valuation

Conclusion

1. Key Facts

Description: Jumbo S.A. (Ticker: BELA - “Jumbo”, “Company”) is a leading diversified retailer known for its affordable pricing and broad product offering, primarily focused on toys, baby products, stationery, seasonal items, and home goods. The Company offers over 40,000 SKUs and operates 89 owned/leased stores across Greece, Cyprus, Bulgaria and Romania, and has presence in North Macedonia, Albania, Kosovo, Serbia, Bosnia, Montenegro and Israel through 40 franchised stores operating under the JUMBO brand.

Key Financials: Over the period FY15 to FY24, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 7.4% and operating income CAGR of 11.7%, reaching an FY24 revenue of €1.1 billion and adjusted operating income of €372 million (margin of 32.4%). Jumbo has cash and short term investments of €444.8 million compared to nil total debt and lease liabilities of €75 million.

Price & Market Cap (as of 30th May 2025): Its market cap is €3.85 billion with a 52-week low of €21.68 and a 52-week high of €29.04, whereas it currently trades at €28.62.

Valuation: Jumbo trades at a TTM EV/EBITDA of 8.2x (5 Year average of 7.2x) and a TTM EV/Sales of 3.0x (5 Year average of 2.5x).

2. Business Overview

a. The Story of Jumbo S.A.

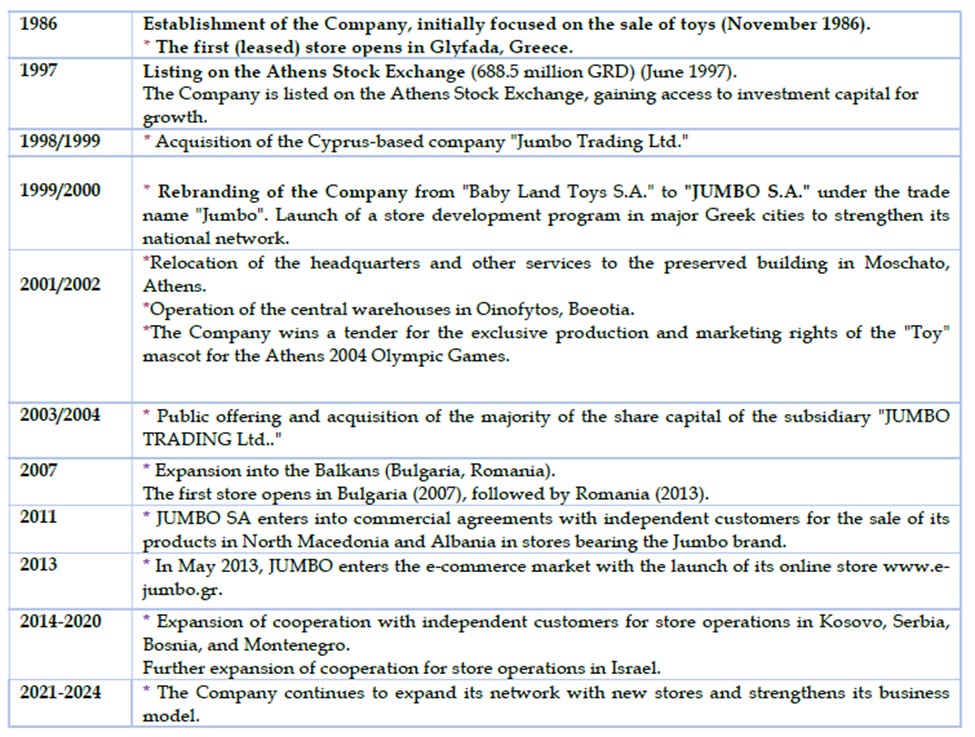

Jumbo S.A. was founded in 1986 by Apostolos Vakakis, who opened the first toy store in Glyfada. But Jumbo’s roots stretch back further, to Vakakis’s upbringing in a business-minded Greek family.

Born in Alexandria, Egypt in 1954, Vakakis came from a family that fled political unrest during the Nasser revolution, resettling in Greece in 1962. His father, George, had produced insulation materials and later worked in a toy-making workshop in Italy. This exposure led the family to establish the toy company El Greco in Greece, which Apostolos helped rebuild after a devastating fire in one of its manufacturing facilities in mid 80s. In 1985, he took over leadership of the company and eventually sold it to Hasbro in 1990, remaining involved as an executive within Hasbro Europe.

By then, Vakakis had already shifted toward retail, having founded Jumbo in 1986. With its big-box format and low-price model, the brand quickly resonated with Greek consumers. A major milestone was achieved in 1997, when Jumbo went public on the Athens Stock Exchange, enabling access to capital markets.

In 1998, it acquired Jumbo Trading Ltd in Cyprus, followed by entry into Bulgaria in 2007 and Romania in 2013. Vakakis essentially expanded into neighboring markets with cultural similarities and logistical advantages. It’s worth noting that apart from the fire during the El Greco years, bad luck struck again in 2000 when a fire destroyed Jumbo’s headquarters and warehouse. The Company then moved its base to Moschato, where it is still located today.

One of its most noticeable achievements came in 2004, when Jumbo secured exclusive rights to produce and distribute the Athens Olympic mascot, helping push annual revenues towards €500 million.

Today, the company operates 89 owned or leased stores in Greece, Cyprus, Bulgaria, and Romania, along with 40 franchised stores in Southeast Europe and Israel. Its retail model, a hypermarket without food, fashion, or electronics, features over 40,000 SKUs and continues to draw strong consumer traffic.

Source: Company’s 2024 Annual Report

Jumbo remains a family-influenced business, as Vakakis still owns 16.4% and serves as a Chairman while Vakakis’s daughter Sophia now serves on the Board as an executive member. His younger daughter Christina pursued her passion for culinary arts, while his son George tragically passed away in a car accident in 2017, a loss that deeply affected the family.

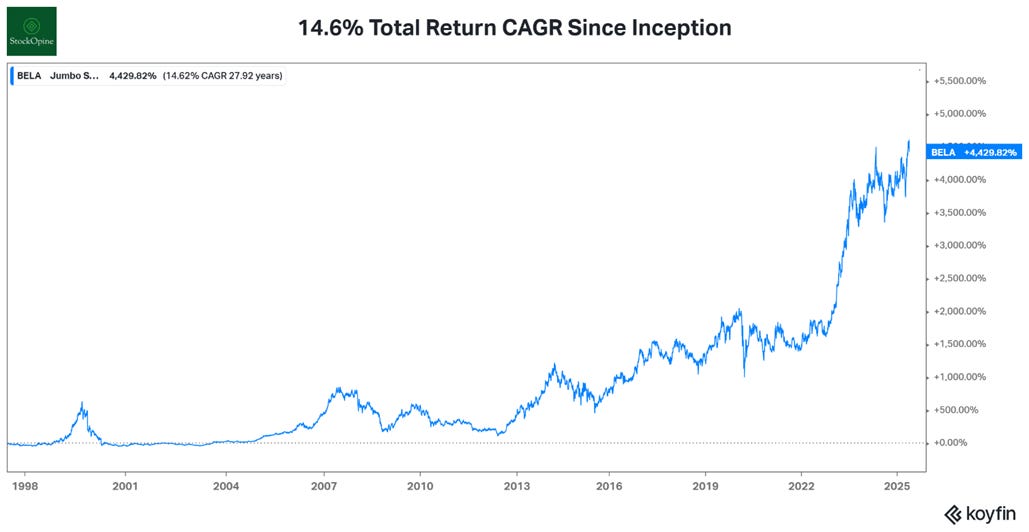

From a single toy shop to a regional retail force, Jumbo has delivered an impressive 14.6% annual total shareholder return since IPO, built on conservative growth, operational discipline, and a product mix designed to endure across cycles.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

b. Business model

Jumbo S.A. operates a value-driven retail model. From the outset, Jumbo has maintained a low-price strategy to foster trust and long-term customer loyalty. Founder Apostolos Vakakis recently reaffirmed this focus, stating:

“There's absolutely no desire to adjust prices upwards. We would be more than happy to adjust prices downwards and pass theoretical gains to our customers in order to consolidate our future…So we always have to be very careful not to create a gap.”

While primarily a retailer, Jumbo also engages in limited wholesale operations requiring strong credit histories from partners to mitigate default risk.

In recent years, Jumbo has strategically moved from leasing to owning stores to reduce operating costs. Between FY2020–FY2024, the Company acquired five previously leased stores for €39M, and most new store rollouts in 2023–2025 are company-owned. Vakakis explains:

“Leasing a store would cost us, let's say, 7.5%, 7% on the estimated value of the store, while owning the store, especially if you are liquid, is 0%.

While Vakakis prefers owning stores to avoid lease costs of 7–7.5%, this strategy draws some criticism. With returns on capital near 20%, critics argue that the capital tied up in real estate could be better used to fund growth or returned to shareholders, a classic opportunity cost trade-off. Still, this reflects Vakakis’s conservative mindset, focused on long-term cost control.

To his credit, this hasn’t limited growth or shareholder returns as Jumbo continues to pay dividends and recently started a buyback program.

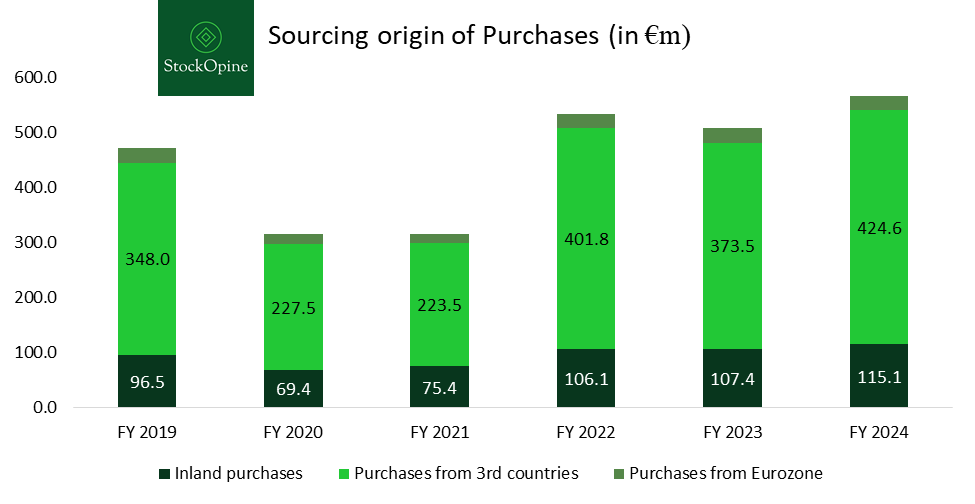

Sourcing, Supply Chain & Risk Management

Roughly 70% of Jumbo’s products are sourced from Asia, particularly China. The Company acts as the exclusive importer for several international toy manufacturers not represented in Greece, while also purchasing from 200+ local suppliers. None of its suppliers represents more than 3% of turnover limiting concentration risk and strengthening its bargaining power.

Source: Jumbo Annual Reports, StockOpine analysis

However, the Company is not immune to global supply chain disruptions. Jumbo manages this by investing heavily in logistics infrastructure and building up inventory buffers when needed. To improve supply chain resilience, the Company owns advanced warehousing and distribution centers in Greece, Cyprus, and Romania (footprint of c. 560.000 sqm), supporting both physical and online operations. Jumbo also plans to add two new distribution hubs, one in Thessaloniki for Northern Greece/Bulgaria and another in Oinofyta for the rest of Greece and exports, with over €60M in investment over the next 3–5 years.

In the near term, the Company stands to benefit from favorable sourcing dynamics, including lower costs from Chinese suppliers and potential pricing leverage due to the US-China tariff tensions and a stronger euro. However, these tailwinds are inherently volatile and short-lived. While margins may benefit temporarily, the long-term outlook remains uncertain, reinforcing the need for supply chain agility.

Seasonality & Inventory

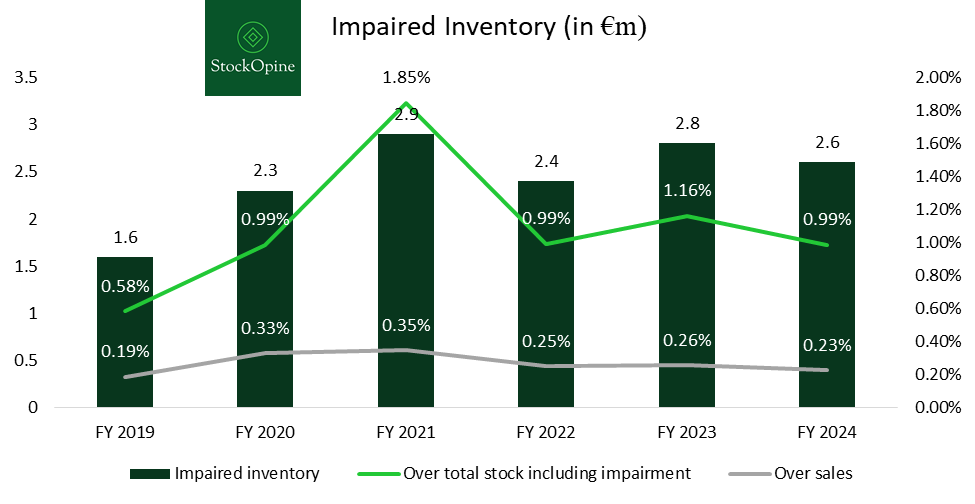

Jumbo’s sales are highly seasonal, with approximately 28% of annual revenue generated in December (Christmas), 12% in April (Easter), and 10% in September (back-to-school). This seasonality requires effective inventory management to minimize the risk of obsolete stock.

In practice, inventory write-offs remain low, highlighting Jumbo’s effective forecasting and stock control across peak periods.

Source: Jumbo Annual Reports, StockOpine analysis

Branding & Advertising

Brand recognition is a key competitive strength for Jumbo, closely associated with products for every occasion at affordable prices. The “JUMBO” brand is trademark-protected through 2032 and promoted through high-visibility TV and social media campaigns, often characterized by a clever, unconventional tone.

One standout example was the 2023 Easter campaign in Greece, where a popular singer was humorously depicted singing about the traditional Easter barbecue, on the moon, after being banished from Earth by vegans. Contradictory, yes; but undeniably effective in capturing public attention and reinforcing Jumbo’s brand visibility.

c. Geographic Segments

The Group reports four core geographical segments, namely, Greece, Cyprus, Bulgaria, and Romania. Greece remains the largest market, with 53 stores and revenue of €559.8 million (excluding franchise collaborations), accounting for 52% of the total sales mix, down from 73.3% in FY2015.

Romania has been the fastest-growing market. Since 2015, the number of stores has increased from 6 to 20, and revenue has grown from €24.3 million to €252.2 million in FY2024, reflecting a CAGR of 27.9%.

In terms of profitability, Greece leads with a gross profit margin of 56.9% in FY2024, averaging 56% over the past five years. Cyprus has the lowest, yet still healthy, margin at 52.1%, with a five-year average of 52.4%.

The margin differences are largely explained by logistics and sourcing efficiency. Shipping from China to Greece is generally cheaper, thanks to Piraeus port, which offers high-capacity container handling and direct sea freight routes. Greece also benefits from local sourcing, further enhancing margins. From Greece, goods can be efficiently transported via land freight to Bulgaria and Romania, while Cyprus requires costlier sea freight, justifying the slightly lower margins in that market.

Source: Jumbo Annual Reports, StockOpine analysis

Note: In FY2019, Jumbo changed its fiscal year-end from June 30 to December 31. As a result, the first FY2019 shown in the chart covers the period 1/7/2018 to 30/6/2019, while the second FY2019 reflects the calendar year 2019 (1/1/2019 to 31/12/2019).

Source: Jumbo Annual Reports, StockOpine analysis

Source: Jumbo Annual Reports, StockOpine analysis

Greece

As noted earlier, Greece currently has 53 stores, the same number as in FY2015. Yet, during this period, revenue has grown at a CAGR of 3.6%, reaching €599.8 million, an increase of €172.7 million. This growth has been driven primarily by organic expansion, not store openings, as average revenue per store rose from €8.1 million to €11.3 million (a CAGR of 3.5%). In Greece, Jumbo’s strategy focuses on optimizing its existing network, including the reassessment and upgrading of older stores. For example, it recently acquired a 5,600 sq.m. property adjacent to its owned store in Corinth to expand that location. While Jumbo aims to open one new store every three years in Greece, it’s clear that future growth in the domestic market will rely more on efficiency improvements than store expansion.

Cyprus

In Cyprus, Jumbo currently operates 6 stores, up from 5 in FY2015. Over this period, revenue has grown at a CAGR of 5.2%, reaching €121.9 million, an increase of €46.9 million since FY15. Similar to Greece, this growth has been primarily organic, with only one new store opening in Nicosia in October 2024. Meanwhile average revenue per store rose from €16.7 million to €22.2 million (a CAGR of 3.0%).

Looking ahead, two new hyper-stores are expected in the next five years, one in Larnaca and another in Protaras. In our view, the Larnaca expansion is well justified, supported by growing local demand and increased investment from Israeli and Lebanese residents. However, the Protaras store raises some questions, given the area’s strongly seasonal, tourist-driven economy. It’s possible that the decision is tied to capturing seasonal summer sales, which are typically overpriced during peak tourist months in the Protaras region.

Bulgaria

In Bulgaria, it currently operates 10 stores, up from 8 in FY2015. During this period, revenue has grown at a CAGR of 10.2%, reaching €114.2 million, an increase of €68.9 million compared to FY2015. Growth was driven by a combination of store expansion and operational improvement, with two additional stores opened and average revenue per store rising from €5.7 million to €11.4 million (a CAGR of 7.7%).

Over the next two to three years, the company plans to add another hyper-store in the country. At the same time, it completed the divestment of a land plot valued at €826 thousand in February 2025, which had originally been bought for development. The sale was completed at a profit. Commenting on the shift, Mr. Vakakis noted that acquiring an existing store is often easier than building one from scratch.

Romania

Romania has been Jumbo’s key growth driver over the past decade, with the number of stores rising from 6 to 20, representing a CAGR of 12.9%. At the same time, average revenue per store increased from €6.1 million to €14.0 million (a CAGR of 9.2%). As a result, total revenue in Romania grew at a CAGR of 27.9%, reaching €252.2 million in FY2024, an increase of €227.9 million compared to FY2015.

The Company plans to continue expanding in Romania, targeting one to two new hyper-stores per year, reinforcing the country’s role as Jumbo’s primary growth lever. However, competition is intensifying with the entry of Action, the Dutch-based international discount chain, into the Romanian market. While this introduces new challenges, Jumbo maintains a competitive edge with a significantly broader product range (40,000 SKUs vs. Action’s 6,000).

Management has expressed confidence, welcoming competition rather than seeing it as a threat. This is supported by Jumbo’s strong EBITDA margins in Romania (~36.5%), which are substantially higher than Action’s EBITDA margin of c.15%, giving the room to absorb pressure if needed. That said, the main risk lies in potential margin compression, which we address in the valuation section of this report.

Partnerships/Collaborations

Though franchise operations represent only ~5% of sales, they’ve seen strong growth as store count rose from 9 in FY2016 to 40 today, and revenue grew from €12.5 million to €61.7 million (20% CAGR).

Israel has been the standout in FY2024. Jumbo, via its agreement with Fox Group, currently operates three stores, with two more opening by end-2025. Despite geopolitical instability, Israel continues to outperform, and management sees room for further expansion. Mr. Vakakis said:

“Israel against logic is doing better than expected. And I'm saying that not because the GDP is not double of the Greek one or double of any of the countries that we are currently operating, but because they have an ongoing war. So for us, it is difficult to understand what exactly goes on. But if we want to make, let's say, a base uninformed judgment, Israel is a success story and can only go better if the war gets out of the way.”

In May 2025, Jumbo also signed a deal with Fox to enter Canada, where the first store is expected to open in H2 2026. While Canada presents an exciting opportunity, execution depends on Jumbo’s infrastructure readiness to avoid stretching internal resources.

Management remains cautious, emphasizing that franchise growth should not come at the expense of core subsidiaries. As such, expansion into new countries is possible, but contingent on supply chain capacity and strategic fit.

Source: Jumbo Annual Reports, StockOpine analysis

d. By product category

Over the past decade, the product mix has evolved, reflecting shifting consumer preferences. Toy sales, once dominant, grew modestly from €168.8 million in FY2015 to €216.6 million in FY2024 (a CAGR of 2.7%), with their share of total revenue declining from 29% to 18.8%. Meanwhile, seasonal and home products have become key growth drivers. Seasonal products grew at a 6.7% CAGR, adding €123.2 million, while home goods expanded at a 10.6% CAGR, adding €276.5 million to reach €449.6 million, now accounting for 39% of total sales, up from 29.7% a decade ago. Management remains focused on expanding categories that align with customer needs, excluding electronics, food and fashion, and sees continued opportunity in items that complement core ranges, including pet and family-oriented products.

Source: Jumbo Annual Reports, StockOpine analysis

3. Management

a. Culture

Jumbo has a Glassdoor rating of 3.5 based on 43 reviews, with 54% of employees saying they would recommend the company to a friend. This compares to Action’s 3.3 rating (57 reviews, 57% recommendation rate), and another pan-European discounter (Pepco) with a 3.0 rating and only 40% recommending it to a friend (45 reviews). While the sample sizes are not statistically robust, they suggest that Jumbo may offer a slightly more favorable work environment.

In the past, Jumbo faced criticism regarding working conditions, but today it emphasizes compliance with local standards and that employee remuneration meets or exceeds national collective labor agreements. Additionally, staff also receive meal vouchers, Easter and Christmas gift vouchers, and in-store discounts; benefits that likely contribute to employee satisfaction.

Employee turnover was 30% in 2024 (36% in 2023, 37% in 2022, and 35% in 2021), which is high but expected in the retail industry due to the large number of seasonal roles, especially in Greece. In fact, 1,146 out of 4,260 employees in Greece (27%) were seasonal. Of the 2,234 employees who left in 2024, 1,230 were tied to end-of-contract departures, implying an effective turnover rate of ~13%.

Source: Jumbo FY24 Annual Report

b. Leadership

Jumbo’s leadership combines deep experience with emerging talent. Recent appointments include Anastasia Zante, born in 1999, who became Chief Operating Officer in 2024 after joining Jumbo in 2021 and Mr. Polys Polycarpou who joined in 2022 and became CFO in 2024. Mrs. Zante rapid rise has raised some eyebrows due to her young age, though there is no public indication that she is related to Chairman Apostolos Vakakis.

Konstantina Demiri has been CEO since 2016 and with the Company since 2003, previously serving as CFO. She brings decades of financial and retail experience. Sofia Vakaki, age 38 and daughter of Mr. Vakakis, joined Jumbo in 2012 and now plays a key role in marketing and strategic planning.

Other long-tenured executives include:

Eleni Tsitsopoulou (IT Manager, since 1994)

Stylianos Andrianopoulos (Logistics Head, since 2006)

Ioanna Terzaki (Internal Audit, since 2000)

Amalia Karamitsoli (Investor Relations, since 2007)

Stella Chimara (Risk Management, since 2007)

While the management team is highly experienced and deeply familiar with the Company, Mr. Vakakis, now 71, remains the driving force behind Jumbo’s strategy. His hands-on leadership is reflected in the 36 board meetings held in 2024, consistent with prior years, and his prominent role in earnings calls. This level of involvement underlines his control over strategic decisions, raising the question of how leadership continuity will be managed once he decides to step down.

c. Compensation

Detailed remuneration for Board Members in 2024 has not yet been disclosed. However, in 2023, only fixed salaries were paid, as Jumbo does not have variable compensation or stock option plans in place. Reported amounts include €630.7k for Chairman Apostolos Vakakis, €332.9k for CEO Konstantina Demiri, and €163.5k for Sofia Vakaki.

Using 2019 as a base year, Board of Directors' salaries increased by 10% through 2023, compared to a 28% rise in sales and a 71% increase in earnings, highlighting a conservative approach to pay and a clear alignment with performance.

Source: Remuneration Report 2023

Source: Remuneration Report 2023, StockOpine analysis

While these amounts may appear low by US standards, they are above the average CEO salary in Greece (~€232k), which is reasonable given Jumbo’s €3.8 billion market capitalization. Yet, assessing whether these figures are truly “low” requires context.

We examined Fourlis S.A., a smaller listed Greek retailer (market cap ~€200 million), which operates IKEA and Intersport stores across Greece and the Balkans, and also has significant insider ownership. Despite its smaller scale, Fourlis offers a more incentive-aligned package including bonuses and stock options. In 2023, its Executive Chairman Vasileios Fourlis received €1.05 million, while its CEO Dimitrios Vlachakis, appointed in May 2023, earned €306.6k, implying an annualized fixed salary of approximately €250k.

This comparison shows that Jumbo’s executive compensation is on the conservative side, but sufficient to retain and motivate long-serving leadership.

d. Ownership

Jumbo’s shareholder structure reflects a mix of institutional and concentrated insider ownership. Mr. Apostolos Vakakis, Chairman of the Board, indirectly holds 16.4% through Tanocerian Maritime Cyprus Ltd, a stake managed via the Karpathia Foundation.

This is down from 26.7% in FY2015, following a series of stake reductions (sales in 2017 - 3.5%, 2021 - 3.86%, and 2024 - 2.94%) the latter at €27.2 per share. Mr. Vakakis has attributed his gradual exit to a desire to avoid family conflict, explaining that only one of his daughters, Sofia Vakaki, is actively involved in the business. The rest of the Board holds minimal or no shares.

That said, 16.4% insider ownership is significant, and we like it, particularly when combined with growing institutional participation, which is a vote of confidence in the Company’s long-term outlook.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

4. Industry

Jumbo operates in a fragmented and diverse retail environment across Greece, Cyprus, Bulgaria, and Romania. Competition stems from non-food divisions of supermarket chains, traditional toy retailers, stores specializing in children’s products, stationery outlets, and seasonal item sellers, both offline and online.

The greatest threats come from the expanding footprint of pan-European discounters such as Action and Pepco (already has presence in Bulgaria, Romania and Greece), and the continued rise of e-commerce, an area where Jumbo still lags, generating only 3–4% of its sales online. However, Jumbo’s value-oriented model positions it well to consolidate market share, especially as consumers remain price-conscious. As Mr. Vakakis, puts it:

“We, as I repeat, all the time, we are worried if we don't have competition, because if we have competition, it means that we have to relook our strategies and make sure that we are not arrogant. But Jumbo, size-wise, in Greece and in the Balkans is as strong as any company.”

What truly differentiates Jumbo is its operational efficiency. With EBITDA margins around 36%, it outperforms European discounters like Action and Pepco, which operate at roughly 15% and 20%, respectively, and other competitors such as Danish retailer Normal, whose EBITDA margin is estimated at around 10–11%. This margin advantage underscores Jumbo’s ability to manage costs and pricing effectively across its footprint.

a. Market Size and forecasts

Defining Jumbo’s total addressable market size and growth is difficult given its broad product range, but nominal GDP growth is a useful proxy for the future. Greece, Cyprus, and Bulgaria are set to grow 4–5% annually, while Romania is projected to exceed 6%. This supports a mid-single-digit growth outlook, even without store expansion, with further upside from new locations, store reformatting/expansion and improved e-commerce.

5. Financial Analysis

a. Performance

From FY15 to FY24, Jumbo delivered a 7.4% revenue CAGR, reaching €1.1 billion. Gross profit grew at a 7.9% CAGR, with margins improving from 52.7% to 55.2% while operating income rose from €134 million to €372 million (adjusted for insurance compensation), reflecting an 11.4% CAGR and a 32.4% operating margin. Over the past decade, free cash flow margin averaged 17.3%, with FY24 FCF at €234 million or 20.4% of revenue.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers), StockOpine analysis

Gross margins have steadily improved from 52.7% in FY15 to 55.2% in FY24, with a notable step-up from FY21 onwards. This improvement is likely driven by more efficient inventory management, lower transportation costs following COVID-era supply chain disruptions, and inflation-driven pricing benefits in the post-pandemic period. The fact that Jumbo has maintained these elevated margins suggests they may now represent a sustainable level. For example, for FY23, management had anticipated a reversion to a 54% gross margin due to potential deflationary pressures, yet the margin remained at 55%.

Supported by a strong EUR/USD exchange rate, the tariff uncertainty and stable freight costs Mr. Vakakis sees a potential upside to the margins:

“Our gross margin worries seem to have subsided because the currency has strengthened, the transport cost has been stabilized, and definitely, Chinese are not asking more than before for their products since they are not very sure whether they would sell their products to the states or not.”

“Freight rates, the rates have been stabilized except against wild fluctuations of last year, but they still reflect a cost of going through Africa. And it is fair to expect that if this additional trip is taken out of the picture, freight can improve further in our favor.”

The improved gross margins also translated into higher operating margins post-FY21. Payroll efficiency has been another contributing factor, with average payroll costs declining from 12.8% of sales in the three years before COVID to 11.8% on average since FY2021. Operating margin in FY24 stood at 33.3%, or 32.4% when adjusted for insurance compensation related to store flooding damages in Larissa and Karditsa.

Free cash flow margins generally move in line with operating profitability, except in years when the Company actively adjusts inventory purchases. For example, in FY21, inventory purchases were just 38% of sales due to COVID-related uncertainty, with the Company relying on existing stock (around 9% of sales). In FY22, inventory purchases jumped to 56% of sales during a restocking phase. Despite these fluctuations, inventory turnover has improved significantly, rising to around 2x post-COVID versus 1.5x before, demonstrating effective inventory management. For completeness, not that over the past decade, the Company’s free cash flow conversion averaged 53.7% of EBITDA, reaching 57% in FY24.

b. Financial position

Jumbo maintains a strong financial position, with €444.8 million in cash and short-term investments, no outstanding debt, and lease liabilities of €75 million. The Company had previously issued a bond in 2018 maturing in 2026, but opted for early repayment in May 2023, highlighting Vakakis' conservative approach and preference for low financial risk.

Receivables are minimal, with the bulk of the €76 million in trade and other receivables linked to prepaid inventory purchases (€67 million). While advance payments carry a risk of supplier default, this is mitigated by the Company’s diversified supplier base. Other receivables of €62 million, include €40 million owed by the state, limiting credit risk exposure. Inventory management as we explained throughout has also improved. However, front-loaded inventory purchases today to capitalize on lower prices from Chinese suppliers could pressure margins if demand weakens and inventory becomes obsolete.

Cash discipline remains central to Jumbo’s strategy, shaped by Vakakis’ experience during the 2013 Cypriot banking crisis. At the time, Jumbo held €58 million in uninsured deposits in Cypriot banks. Under the bail-in process, 47.5% of the deposits were converted into Bank of Cyprus shares, while approximately €30 million was written off. Today, those shares are valued at around €16.4 million, implying a total loss of roughly €42 million.

c. Capital allocation

Between FY15 and FY24, Jumbo generated approximately €2.2 billion in operating cash flow (OCF). Of that, it allocated €533 million (25%) to net capital expenditures, €1.2 billion (57%) to dividends, €27 million (1%) to share repurchases, and just €1 million to acquisitions. This capital allocation approach emphasizes reinvestment and consistent shareholder returns, primarily via dividends, with a current trailing yield of 5.1%.

The minimum dividend is set at 35% of net profits after statutory reserves and other adjustments. Despite Vakakis’ cautious stance on extraordinary payouts, highlighted by his preference for strategic inventory purchases over special dividends, Jumbo’s record speaks for itself, returning over half of its OCF to shareholders in dividends alone. As he noted:

“If things go our way, and this is a big if, our recommendation to the general assembly would be not to pay dividends, but to utilize the funds to take advantage of a situation developing in our favor and leave dividends as a last resort when other options more profitable are not being offered anymore…”

In September 2024, the board also approved a share buyback program of up to 10% of shares outstanding, valid through September 2026, with a maximum repurchase price of €27.2 per share, a cap Vakakis stated he does not wish to exceed. As of April 25, 2025, Jumbo had repurchased 1,694,198 shares (1.25% of total), investing €43.07 million at an average price of €25.42.

In our view, Jumbo is shareholder-friendly and capital efficient as seen in both its payout track record and improving returns. Return on invested capital (ROIC) rose from 12.5% in FY18–FY19 to 19% in FY23 and 21.7% in FY24.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

d. Outlook

Jumbo typically updates its forecasts mid-year and has a track record of underpromising and overdelivering. However, due to current uncertainty, management has withheld guidance for now and plans to provide an update following the half-year results. Year-to-date (through April), sales have grown by 7.4%, though this figure is flattered by Easter falling in April this year (vs. May last year), strong January sales to wholesalers and franchise partners, and the opening of a new store in Romania in March 2025. All else equal, we believe a growth assumption above 6% is reasonable.

Regarding capital expenditures, management expects to invest €60–70 million, primarily to expand infrastructure. As stated by the company:

"We are growing comfortably enough, and we need further infrastructure to support our current growth. Our desire is to increase the foothold that we have in Romania."

6. Competitive Advantages, Opportunities and Risks

Competitive Advantages

Cost Leadership and Operational Efficiency: Jumbo benefits from a broad supplier network which enables large-volume purchasing at favorable terms. Combined with strong cash reserves, the Company can act swiftly to capitalize on tactical inventory opportunities. This purchasing power, along with disciplined inventory management and significant investments in modern warehousing and logistics infrastructure, supports best-in-class gross and operating margins. These cost advantages allow Jumbo to maintain competitive pricing while delivering industry-leading profitability, effectively deterring new entrants or aggressive competitors.

Strong Brand Recognition: The "Jumbo" brand is deeply embedded in its core markets and widely associated with affordability, variety, and convenience. This strong brand equity drives customer loyalty and repeat traffic.

Diversified Product Mix: Jumbo's wide range of categories, from toys and homeware to seasonal, limits exposure to any single product group and supports consistent year-round demand.

Experienced Management: The Company is led by long-standing management with deep operational experience. High insider ownership further aligns leadership with long-term shareholder interests.

Opportunities

Store network expansion: Jumbo has a clear strategy to expand its physical store footprint across core, supporting long-term growth. Franchise interest remains strong, as seen with Fox Group in Israel (on track to reach five stores by year-end) and its planned entry into Canada by H2 2026, which, while challenging, represents a promising opportunity for international growth.

Market Penetration: Romania and Bulgaria remain underpenetrated, offering room for increased store density and market share gains. Continued investment in infrastructure will be key to supporting this growth while maintaining operational efficiency.

Online Channel Development: Although physical retail remains the core focus, Jumbo’s existing online operations in Greece, Cyprus, and Romania offer a foundation for scalable growth. With a more proactive approach, the Company can better capture the accelerating shift toward online shopping.

Risks

Limited E-commerce Penetration: With just 3–4% of sales generated online, Jumbo significantly lags behind peers in digital retail. In an era of shifts toward e-commerce, this underinvestment poses a long-term risk to competitiveness, particularly as consumer behavior continues evolving.

Inventory Risk: Jumbo’s strategy of front-loading inventory, especially from Chinese suppliers, can support margins, but also carries the risk of overstocking or obsolescence if demand softens. While similar actions during COVID were ultimately manageable, elevated inventory levels remain a watchpoint.

Key Person Dependency: Founder and Chairman Apostolos Vakakis remains the central figure in all strategic decisions, creating a potential key person risk.

Foreign Exchange Exposure: Jumbo is exposed to currency fluctuations, particularly the US Dollar (for procurement) and the Romanian Leu (for local operations). Movements in these currencies can materially impact financial results.

Geopolitical & Supply Chain Risks: Rising geopolitical instability (e.g., Ukraine war, Middle East tensions) and potential changes in trade policy or shipping routes could disrupt Jumbo’s supply chain or inflate logistics costs. The Company’s reliance on Asian sourcing makes it vulnerable to such external shocks.

Intensifying Competition: The expansion of international discounters like Action (set to enter Romania in 2025) increases pressure in Jumbo’s value-focused segment. These players may challenge market share, potentially pressuring pricing and profitability.

7. Valuation

The stock price as of 30th of May 2025 stands at €28.6 with a year to date return of 10.3%. The Company's market capitalization is €3.85 billion and it trades at an EV/EBITDA TTM multiple of 8.2x and Free Cash Flow to Market Cap yield of 6.1%. Based on our DCF valuation, the estimated price of Jumbo is €36.9, ~29% higher than its current price, and an expected IRR over the projected period of 18.1%.

Source: StockOpine analysis

Revenue Assumptions

To estimate Jumbo’s fair value, we assume a revenue CAGR of 4.8%, reaching €1.45 billion by FY29, broadly aligned with analyst expectations for 2025–2028. For FY29, we apply a growth rate of 3%. These assumptions reflect the 7% growth expected in FY25, gradually tapering in later years, and are supported by the GDP growth outlook of core markets discussed in the ‘Industry’ section.

Profitability Assumptions

We assume an average EBITDA margin of 35.6%, tapering to a terminal margin of 35.1%. This is slightly above the 5-year average of 34.5% but below FY24’s 35.6%. Our figures differ slightly from reported numbers, as we deduct credit card commissions, we treat them as operating rather than financing costs. In FY25 we apply an initial margin uplift of ~60bps due to short-term tailwinds such as strong euro and favorable sourcing conditions, followed by a gradual 110bps decline to account for rising competitive pressure. To test downside risks, we model a pessimistic scenario with a 30% terminal margin, which implies a fair value of €32.3 per share, around 13% above today’s price.

Free Cash Flow and Capital Expenditures

We assume CapEx at 5.8% of revenue, aligned with the higher end of Jumbo’s FY25 guidance (€60–70 million), but slightly below its 5-year average of 6.2%. After accounting for taxes and working capital, we estimate a terminal FCF margin of 24.3%, above the historical average of 22.6%. In our model, the FY29 FCF margin lands at 22%, reflecting the gradual decline in EBITDA margins.

However, the terminal FCF margin increases to 24.3% due to the assumption that CapEx equals depreciation. This implies the business reaches a maintenance phase where capital investment is only needed to sustain existing operations (a conservative valuation assumption). As a result, CapEx as a percentage of revenue drops from 5.8% in FY29 to 3.5% in the terminal year.

Terminal Value

As you'll see in our valuation model, we opted for a Gordon Growth Model rather than applying a terminal EV/EBITDA multiple, using a 10% discount rate and a 3% terminal growth rate.

Valuation summary

To calculate intrinsic value, we apply a 10% discount rate, adjust for net debt and non-operating assets/liabilities, and then divide by the total number of shares outstanding.

Based on our model, the fair value per share is €36.9, which is 29% higher than the current market price, implying an IRR of 18.1% over the forecast period.

a. The Valuation model

Here’s the full year-by-year financial projections from our model.

Source: StockOpine analysis

b. Sensitivity analysis

The table below illustrates the potential upside or downside relative to the current share price (€28.6 as of May 30, 2025), based on varying terminal growth and discount rate assumptions. As shown, the valuation remains attractive across all scenarios, emphasizing the stock’s upside potential.

Source: StockOpine analysis

8. Conclusion

Jumbo offers a compelling mix of strong fundamentals, prudent management, and consistent shareholder returns. Its cost leadership, operational efficiency, and disciplined capital allocation have translated into best-in-class margins and robust free cash flow generation. The Company’s steady expansion strategy, particularly in underpenetrated markets like Romania and Bulgaria, alongside selective international franchising, supports a long growth runway.

That said, risks remain. The Company’s underinvestment in e-commerce could prove costly in the long run as consumer habits shift, and its key-man leadership is a risk. Additionally, rising competition from international discounters may compress margins over time.

All things considered, we view Jumbo as a high-quality business with attractive upside potential. We are keen to open a position, but given that our portfolio is currently fully invested, we need to reassess how it fits within our broader allocation strategy. We will inform you accordingly.