We recently updated our Substack page and communicated to our subscribers that starting from October 2022, we will aim to share 2-3 company write-ups per month on companies we decided to examine as potential additions to our portfolio. These companies are selected based on initial predetermined screening criteria which will assist us in identifying stocks that fit our strategy. Although the companies analyzed may tick most of the boxes, if the margin of safety is not considered sufficient we will not initiate a position but rather monitor the stock.

At the end of each write-up, we will state whether we decided to buy the stock or not. If not, keep an eye to our Quarterly Portfolio Update releases in which we will update you for all the transactions that took place during the latest quarter.

For October series, the first company is Old Dominion Freight Line, Inc. (“ODFL”, “Old Dominion”, and “Company”).

1. Key Facts

Description: Old Dominion was founded in 1934 and it operates as a less-than-truckload (“LTL”) motor carrier in US and North America. ODFL provides regional, inter-regional and national LTL services through a single integrated, union free organization. The company has a single operating segment with more than 98% of its revenue derived from transporting LTL shipments.

Resources: ODFL employs c. 25,000 people, has 10,566 Tractors, 42,162 Trailers and 255 service centers in 48 states.

Key Financials: Over the period 2012 to 1H 2022, the Company depicted a Revenue Compound Annual Growth Rate (“CAGR”) of 11.4% reaching a Trailing Twelve Month (“TTM”) revenue of c. $6.0B and generated an Operating Income CAGR of 20.4%, increasing its operating margin from 13.4% to 28%, indicating outstanding efficiencies while growing. Old Dominion has a healthy balance sheet with Cash and Short term investments of $420.5M compared to a debt amounting to $100M (excluding leases).

Market Cap (as of 30th September 2022): Its market cap is $27.81B with a 52-week (and all time) high of $373.58 and a 52-week low of $231.31, whereas it currently trades at $248.77, a 33.4% decline from its all-time high.

Insiders: More than 10% of its shares are owned by insiders with David S. Congdon (Executive Chairman) and John R. Congdon, Jr. (Director) owning the chunk of these shares. As per 2021 10K filing, David S. Congdon, John R. Congdon, Jr. and affiliate family members own c. 18% of ODFL shares.

Customers: Per Adam Satterfield, CFO, ODFL customer base is effectively made from 55%-60% industrial and 25%-30% retail whereas per the latest 10K filing, No. 1 customer accounts for 5.4% of revenue and the top 5 for 16.0%, indicating moderated customer concentration.

2. Business and Competitive Positioning

LTL in few words

Motor carriers can range from full truck carriers to moving companies whereas classification is usually based on freight size and type of business.

ODFL 0.00%↑ falls in the LTL category, meaning that it can serve various customers/shipments per route, and usually, the freight size is larger than a parcel but cannot fill a single trailer or being cost efficient to serve a single customer.

LTL transportation services are mainly priced on weight, commodity, and distance and can include other components such as fuel surcharge (which is spiking lately) and accessorial charges. The higher the density per load the better the asset utilization.

Competition

A. In the Industry

ODFL’s key competitors are Yellow Corporation (formerly known as YRC Worldwide Inc.), FedEx Freight (subsidiary of FedEx Corporation), XPO Logistics Inc., SAIA Inc., TFI International and ABF Freight (an ArcBest Company).

The size of the competitors can be inferred from the following tables:

Source: ODFL August 2022 Investor presentation

Source: Motor Freight 2022 Report-Logistics Management

Although Old Dominion is not the leader in the industry (second behind FedEx Freight in terms of Revenue), it managed to grow the number of its service centers (currently 255) by 16% and shipments per day by 79%, i.e. faster than its peers since 2011, thus grabbing market share in the process. For example, in Midwest ($12.8B total market per management) and South ($9.7B total market) it grew its market share from 5.6% and 7.9% in 2010 to 12.8% and 12.3% as of June 2022, respectively.

Greg Gantt, CEO, The disciplined execution of the business fundamentals that form this plan have supported our ability to double our market share over the past 10 years. We are confident that continued execution on this plan positions us to win additional market share over the next 10 years.

The main reason for this achievement is the superior service, i.e. 99% on time deliveries (94% back in 2002) and the reduction in cargo claims to 0.1% of revenue (>1.5% back in 2002) due to highly trained staff and operational best practices.

It is no coincidence that the Company earned the 2021 MASTIO Quality Award for national LTL carriers as the No.1 national carrier for 12 consecutive years. Obtaining the award under this challenging environment (supply chain disruptions) and all time high driver shortages (Costello, ATA) which are expected to double by 2030, demonstrates that ODFL has sustainable business model and invests effectively in its employees. It is no surprise that job postings relating to ‘Drivers’ on the Company’s website are only 22, relative to the 11,802 drivers as of 31 December 2021.

Its great Company culture is also supported by ODFL Glassdoor score, which is above its peers at 3.9* with a CEO approval rate of 86% compared to ABF Freight (2nd) with 3.8* and 81% ratings, respectively.

B. New entrants

There are high fixed entry costs to create and maintain a hub and the process to set-up a network is lengthy, thus the industry seems to be protected from new entrants. For instance, ODFL invests on average 10-15% of its revenue in Capital expenditures (“CAPEX”), with 2021 CAPEX of $550M and $323M for 1H 2022 (expected to close 2022 with $835M). Likewise, FedEx Freight which in general spends less than ODFL (4% in its Fiscal Year (“FY”) 21 and 3.35% in its FY22), recently invested $150M in its Q1’FY23 (e.g. 5.5% of revenue).

C. Substitutes

Nonetheless, the competition does not stop at the LTL level as customers may shift to truckload or intermodal, subject to capacity, service and pricing. As capacity of truckloads becomes available due to the slowdown in the economy there could be a truckload spill over effect. Despite this, management estimates that these type of shipments declined from 5% of revenue to 1.5%, thus the risk is not necessarily material.

3. Financials

As stated above, ODFL had a Revenue CAGR of 11.4% for 2012-1H 2022 (“Historic Period”) while profits and free cash flows were growing at a faster rate reaching an Operating Margin (“OPM”) of 28% and a Free Cash flow (“FCF”) margin of 14.3%.

Due to the above growth observed, Revenue increased from $2.1B in 2012 to $6.0B in 1H 2022 on a TTM basis, Operating income from $285M to $1.7B and Free Cash Flow from a negative $45M to a positive $853M.

Source: Koyfin, StockOpine analysis

Revenue growth was both volume and price driven, as shipments per day increased from 30,571 per day back in 2012 to 53,096 in Q2’2022 (increase of 73.6%) whereas LTL revenue per shipment increased from $271.82 to $484.08 (increase of 78.1%).

While growing, the Company achieved cost efficiencies and during Q2’ 2022 it managed to reduce its operating cost ratio below 70% compared to >85% back in 2012.

To keep growth momentum, other than its best in class service, the Company spends 10-15% of revenue in CAPEX to increase / upgrade its fleet, increase the number of its service centers, to enhance its technological systems/capabilities and to ensure that it has capacity to address demand requirements when there is an inflection point in the industry (similar to what happened in the last couple of years).

Relative to competition (on a Latest fiscal year basis - may vary from company to company) the next best performing company in terms of Operating Margin and FCF margin are FedEx Freight (not FedEx Corporation) with OPM of 17.4% (23.9% in its Q1’FY23 and 12.8% in its FY21) and TFI International with FCF margin of 8.1% (12.4% in prior year).

Lastly, ODFL has a solid financial position with Cash and Short term investments of $420.5M compared to a debt amounting to $100M and estimated leases of c. $105M.

4. Capital Allocation

The Company did not engage in significant M&A transactions recently, but invests its operating cash flows organically (CAPEX) to fund growth while returning excess capital to shareholders.

It initiated the payment of dividends in 2017 and although the yield is insignificant 0.44%, the growth from $0.067 to $0.3 per share per quarter is noteworthy.

Additionally, ODFL engages in a share repurchase program and as of 30 June 2022, $1.22B is outstanding, whereas the total number of shares declined from 129.2M back in 2012 to 111.8M as of 2 August 2022.

The efficiency of capital allocation strategy is justified by results, as it has almost doubled its Returns on Equity (18.0% to 35.7%) and Capital (14.9% to 29.2%) while the equity and capital were increasing. On a Latest Twelve Month basis it rates better than its peers on both metrics.

Source: Koyfin, StockOpine analysis

5. Risks and Opportunities

Opportunities

Benefits from the Bipartisan Infrastructure Law ($110B to repair roads and bridges, 5-year authorization) and the potential passing of the Truck Parking Safety Improvement Act (will authorize $755M over 4 years to address truck parking). As per the White House, in the United States, 1 in 5 miles of highways and major roads, and 45,000 bridges, are in poor condition. $110B in repairing and rebuilding these roads and bridges (and on major transformational projects) will improve supply chain efficiencies and reduce traffic fatalities. Likewise, parking availability will reduce the forced and unsafe and/or illegal parking and constitute to regaining the lost truck driver time per day (estimated at 56 minutes of valuable drive time per day, as per American Trucking Association). Such developments can drive more deliveries, even better delivery times, less cargo claims and happier drivers.

Ecommerce growth is expected to positively impact LTL carriers as small retailers need to send smaller quantities of goods rather than truckload (saves cost and time).

Risks

Driver shortages in the truck industry. On a positive note and considering that infrastructure and parking is one of the primary reasons for shortage, on 22 of September 2022 it was announced that Florida and Tennessee were awarded a combined $37,600,000 in INFRA grant funding to expand their truck parking capacity -- with more states sure to follow.

Ongoing increases in operating costs such as salaries (19.8% for 1H 2022) and fuel. These are easily covered by current revenues and can be partly passed to consumers (see fuel surcharge) but we cannot ignore the recession fears; as any slowdown in demand will not necessarily mean a cut in the number of drivers (who are in shortage). At least, management is committed to “maintain disciplined control over costs to keep our cost inflation on a per shipment basis to a minimum” Adam Satterfield, CFO, and strives to exceed cost per shipment inflation by 1% to 1.5%.

Concerns about moderation in demand and volume which could impact price environment. Nonetheless, it all comes to capacity.

LTL carriers benefited from limited capacity of truckloads but due to potential economic slowdown there could be a truckload spill over effect. That is, customers moving from using LTL carriers back to full truckload given availability. Despite this, management estimates that these type of shipments declined from 5% of revenue to 1.5%.

6. Outlook

The Company has excess capacity of 15%-20% and expects to open multiple new facilities in the 2H of 2022 to increase its excess capacity to 25%, translating to an estimated CAPEX for the year of $835M. The strategy is proactive as the process to expand network is lengthy but as per management, carrying that extra cost is part of the strategy so as to be present and ready when there are positive inflections in the economy.

Greg Gantt, CEO, We remain committed to the ongoing expansion of our service center network, which we believe is important regardless of the short-term macroeconomic outlook.

In terms of operating costs, the Company expects to see in uptick in Q3 (1%-1.5%) compared to Q2 2022 (record operating cost ratio of 69.5%), mainly due to marketing activities and some miscellaneous expenses that trended lower in the first half of the year. This will potentially drive the operating ratio above 70% (higher than the annual goal of 70%) but management does not seem worried about this.

7. Valuation

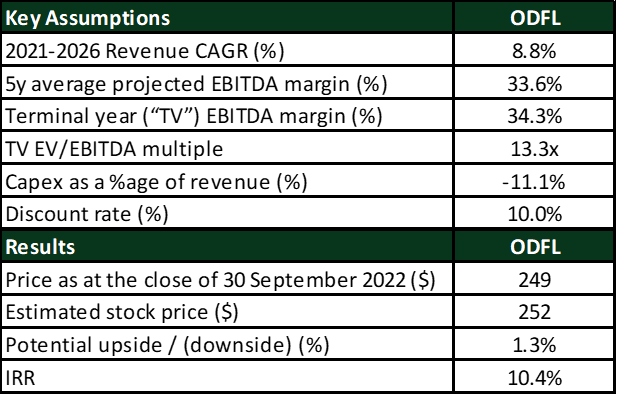

The stock price as of 30th of September 2022 stands at $248.77 and is down by 30.4% YTD. The market cap of the Company stands at $27.8B and trades at an EV/EBITDA TTM multiple of 14.0x. Based on our DCF valuation the estimated price of ODFL stands at $252, which is in line with the current price level, with a resulting IRR over a 5-year period of 10.4%.

Source: StockOpine analysis

To estimate the fair value of Old Dominion we assumed a revenue CAGR of 8.8%. Given that 2022 is already halfway and revenue grew by 29.4% (we model 21% based on analyst’s consensus for the whole year), we apply a 6.0% CAGR for the period 2022 to 2026, i.e. well below the 11.4% of the Historic Period. Per our view, this is reasonable as the demand for ODFL services is linked to industrial production, the US nominal GDP is expected to average at 4% over 2023-2026 (Congressional Budget Office, July 2022 report) and we expect ODFL to win marginal market share during this period.

In terms of profitability, we used an average projected EBITDA margin of 33.6% and a terminal EBITDA margin of 34.3%. Both average and terminal EBITDA margins are higher than the average EBITDA margin for 2018 - 1H 2022 of 28%, however, our assumption accounts for a gradual improvement in margins similar to Company’s execution as of today. For example, EBITDA margin increased from 29.1% in 2020 to 31.4% in 2021 and stands at 33.2% for the first six months of 2022.

To derive the free cash flows to the firm we deducted projected Capex requirements of 10.8% in line with its 5 year average, except for 2022, for which a higher ratio was assumed given management estimates.

In respect to the terminal EV/EBITDA multiple, it is assumed to be around 13.3x which is lower than its 5 year average of 16.4x and its current multiple of 14.0x. Although the Company deserves a premium relative to peers (5Y average of 8.6x and current average of 5.6x) given its execution as of today; we applied a minor haircut from current multiple.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialize at all), we reach a value per share of $252, in line with the current price of $248.77 with a resulting IRR over a 5-year period of 10.4%.

Sensitivity analysis

The below table gives an indication of the potential upside/(downside) %age compared to the current price ($248.77 as of 30th of September) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

8. Concluding Remarks

ODFL is operating in a relatively consolidated industry with high barriers of entry and strong track record of execution.

We believe that ODFL has quality business model considering its financial position, its margins relative to competition, its best in class service, the improvement in returns on capital and how it managed to double its market share over the last ten years.

Despite this, we will not be buyers at this time given that the share price spiked since 30 September 2022, though ODFL makes a good fit to our portfolio and subject to recession developments and price movement we might initiate a position.

You can also find us on Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

Thanks for a good write up

Thanks for the great write-up!