1. Company Profile

2. Business Overview

3. Industry Overview

4. Culture and Leadership

5. Financials

6. Risks & Opportunities

7. Valuation

8. Investment thesis

1. Company Profile

PayPal Holdings Inc. (“Company”, “Group”, and “PayPal”) was spun off from eBay in 2015 and is a leading technology platform that enables digital payments and simplifies commerce experiences of merchants and consumers worldwide. By leveraging technology to make financial services and commerce more convenient, affordable and secure, the PayPal platform is empowering people and businesses to join and thrive in the global economy.

In addition to PayPal platform, the Company owns amongst others, Xoom, an international money transfer business, Braintree, a payment gateway business, Zettle, Point of Sale solutions and Venmo, a peer-to-peer payment platform. PayPal recently acquired Honey (completed in 1/2020) for $4B, a technology company that aggregates and applies coupons on ecommerce websites and Paidy (completed in 10/2021) for $2.7B, a buy now, pay later solutions business in Japan.

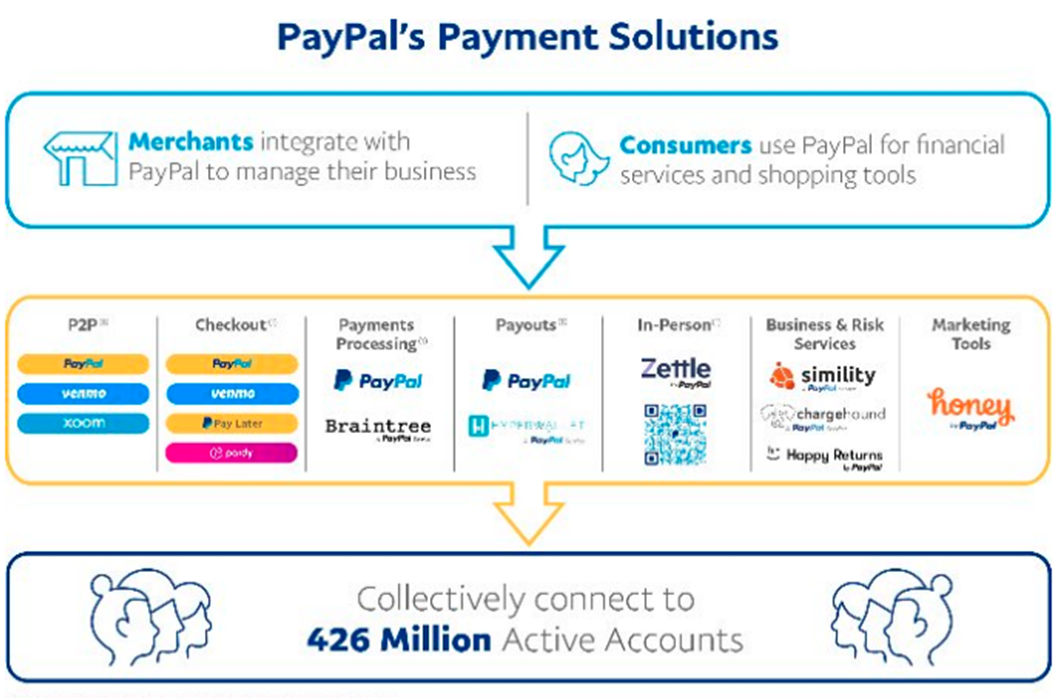

The Company operates a global two-sided network that connects merchants and consumers, reaching 426M active consumer and merchant accounts (34M) in more than 200 markets around the world. The total payment volume (“TPV”) that was completed successfully on PayPal’s platforms or enabled by PayPal’s partner payment solutions for 2021 was $1.25T (CAGR of 29.15% since 2018) with total payment transactions of 19.3B (CAGR of 25.15% since 2018) and revenues of $25.4B (CAGR of 17.98% since 2018).

Stock Performance (as of 03/03/2022)

Market Cap: $118.4B

Current Price: $101.34

P/E: 28.87

52W L-H: $94.5-$310.16

5Y, 1Y and YTD Stock Performance: 136%, -60%, -46%

Analysts’ estimates: Moderate Buy (27 Buy, 9 Hold, 1 Sell), Target Price: $184.42 (82%)

2. Business Overview

The Company generates revenue from net transaction fees charged to merchants and consumers on a transaction basis based on the TPV completed on the payments platform (92% of total revenue) and from other value added services (8% of total revenue) such as partnerships, referral fees, subscription fees, gateway fees, interest and fees from loan receivables etc. The key markets of PayPal are US (54%) and UK (9%).

In the last 10 years, the Company achieved superb growth rates growing revenue from $5.6B in 2012 to $25.4B in 2021 (CAGR of 18.2%) due to its product offering/ecosystem expansion, which in effect enabled growth in the number of users and engagement. For example, in 2021, after the launch of the new digital wallet globally the following trends were observed; +700% in merchant leads, +200% first time users in Bill pay, +330% first time users In-app donations, +40% Crypto first-time users, 25% less churn, 2x ARPA (average revenue per active) of Digital Wallet and BNPL users Vs checkout only users.

The product offering expanded from a checkout and P2P business to:

Consumer-> Payments (Checkout, P2P, QR code, Charitable Giving), Financial Services (Debit/Credit card, Buy now pay later, Remittances, Goals, Crypto etc.) and Shopping Tools (Deals and Offers, Droplist, Price Tracking, Rewards).

Merchants-> Payment Processing (Checkout, Unbranded Processing), Merchant Services (Business Debit Card, PayPal working capital, Point of Sale, Business loans, Risk Services, Invoicing etc.) and Marketing Tools (Shopper Insights, Deals Engine, Dynamic Banners etc.).

A screenshot extracted from 2021 10K Report summarizes PayPal’s payment solutions.

Industry Overview

PayPal operates in a fast-growing industry (fintech) and is expected to maintain its leadership position due to the network effect it created by being a first mover and by building a massive number of active users (426M active accounts).

E-commerce and the shift to online / digital payments is expected to continue but not with the same exponential growth as it was observed during the pandemic. A few articles that are mentioned below show the positive dynamics in the industry.

Ecommerce Statistics: Insider Intelligence. – US retail ecommerce sales are expected to cross $1.06T in 2022, up by 16.1%, whereas B2B ecommerce sales are expected to reach $1.77T, up by 12.0%. Worldwide ecommerce sales are expected to reach $5T in 2022 and $6T by 2024.

Global Digital Payments. – The Global Digital Payment market is expected to grow from c.$5.9T in 2021 to c.$9.1T in 2025 (CAGR of 11%). Major players in the digital payments market are Alipay, Amazon Pay, Apple Pay, Tencent, Google Pay, First Data, PayPal, Fiserv, Visa Inc., and MasterCard.

Statista - retail ecommerce sales – worldwide retail e-commerce sales of c. $4.9 trillion in 2021 and forecasted to reach c. $7.4 trillion by 2025 (CAGR of 11%).

The above industry estimates along with PayPal’s TPV Total Addressable Market of $110T as indicated by Management, shows that PayPal’s best days lie ahead rather than in the past.

Competition

PayPal has numerous competitors either at the wide product offering or at a specific product offering. Competitors include among others the companies mentioned above as well as Block Inc., Stripe, TransferWise, Adyen, Paysafe (Skrill, Neteller) etc.

One of the key competitors of PayPal is Block Inc., therefore, a high-level head-to-head comparison is made below.

During 2021 Block reported $167.7B Gross Payment Volume (GPV), up by 49% (or $55.4B); whereas PayPal’s TPV increased from $936B to $1.25T, up by 33% (or $310B).

Total Revenue of Block was $17.7B, up by 86% (or $8.2B); whereas PayPal’s revenue increased to $25.4B, up by 18% (or $3.9B). It shall be noted that $5.4B of the increase in Block’s revenue comes from Bitcoin revenue ($10.0B in 2021). Although Bitcoin revenue accounts for 57% of total revenue, it only accounts for 5% ($218M out of $4.4B) of the Gross Profit.

Total operating income of Block is $161M i.e., less than 1% operating margin and includes an impairment of $71M arising from the decline in Bitcoin value, whereas PayPal’s operating margin stands at 16.8% for 2021.

Cash App, a P2P mobile app, and a direct competitor of Venmo (PayPal), showed a massive revenue growth in 2021 of $900M or 65%, reaching $2.3B (excluding Bitcoin), whereas Venmo’s revenue in 2021 was c. $900M. PayPal also has similar functionalities as Cash App. Cash App had more than 44M monthly transacting actives in December 2021 Vs 83M people using Venmo as stated by the CEO on the latest earnings transcript.

Block, through its acquisition of Afterpay - BNPL in 31/1/2022 is expected to also contend PayPal on the BNPL business. As per FY21 Afterpay results (25/8/2021), it has more than 16M active consumers and 100k merchants compared to 12.2M unique consumer accounts and 1.2M Merchants with PayPal BNPL transactions.

Block is a challenger of PayPal in many fronts but given the size of the market and the growing dynamics both can be winners.

4. Culture and Leadership

Employees

Based on Glassdoor (5,867 reviews), the overall score of the Company is 4.1 (out of 5), 80% of the reviewers would recommend to a friend, 78% have a positive business outlook and 91% approve the President and CEO (Dan Schulman). Moreover, as per the 2021 internal annual employee survey, 83% of the respondents indicated that would recommend PayPal to their peers and/or are happy at PayPal.

The above along with the various awards that were achieved by the Company as well as the quote of Dan Schulman President and CEO as shown on the Company’s website (“I believe that the most important constituency for any company is its employees—and at PayPal we work to put our employees first”), displays a healthy culture within the organization.

Note: Block’s Glassdoor comparative scores are 4.3 (overall), 84% (recommend to a friend), 81% (positive outlook) and 94% (Approve of CEO). Stripe’s Glassdoor comparative scores are 4.1 (overall), 77% (recommend to a friend), 87% (positive outlook) and 94% (Approve of CEO). Visa’s Glassdoor comparative scores are 4.0 (overall), 79% (recommend to a friend), 77% (positive outlook) and 94% (Approve of CEO).

Governance and Leadership

As per the diversity, inclusion, and equity metric, 50% of the Board and 56% of senior leadership team are women and/or from a diverse ethnic group (as of December 2021).

It shall also be noted that: a) 11/12 directors are independent, b) all directors stand for annual election, c) Regular review of Board and executive succession planning, d) Annual performance self-evaluations by the full Board and each committee and e) the majority of the Executive Leadership Team has been with the Company since 2015.

The CEO of PayPal, Dan Schulman has been with the Company since 2014 and is the CEO since 2015. As per the latest Form 4 filing, Dan Schulman owns 323,323 shares in the Company which represents 0.03% ownership and a current market value of $32M. For the year ended 2020, his compensation was $23.3M of which $21M was in stock awards.

Executive Officers and Directors own less than 1%, however, in Feb 2022 and after the Company reported its results, 4 insiders, including the President and CEO, purchased 24,894 shares, whereas 1 insider sold 4,245. The net purchase is considered a positive signal for the future stock performance.

5. Financials

Growth and profitability

The Company has consistently grown its revenues and since 2018 an increase from $15.4B to $25.4B was observed. This is partly explained by the fast-forward shift to ecommerce due to the pandemic and by the expansion of the Company’s product offering from a checkout and P2P payment solutions business to a wide range of solutions for both merchants and consumers (refer to the Business Overview section). As per the latest guidance, Revenue is expected to exceed $29B by 2022.

The operating income during 2018-2021 increased from $2.2B to $4.3B, while at the same time operating margin improved from 14.2% to 16.8%. Operating income of 2021 includes a reserve release for credit losses of $312M, whereas the operating income of 2020 includes a reserve build of $296M. Adjusting for these reserve movements it will change the operating margin of 2020 and 2021 to 16.7% and 15.6%, respectively (“Adjusted Operating Margin”).

A key reason of the decline in Adjusted Operating Margin was the reduction in total take rate from 2.29% in 2020 to 2.04% in 2021 (transaction rate from 2.13% to 1.88%) whereas the transaction expense marginally improved from 0.85% to 0.83%. Take rate was down due to lower eBay volumes and due to lower FX fees monetized on cross border transactions. Despite the decline in take rates on an annual basis, in Q4 2021 (2.04%) there was a sequential increase Vs Q3 2021 (1.99%). Please note John Rainey’s (CFO) commentary extracted from the earnings transcript: “Well, we were pleased to see the sequential increase in take rate in the quarter versus the third quarter. And I do think it sort of underscores some of the strength in our business, particularly around pricing and also, as Dan noted, Venmo. Quite excited to see that Venmo, having achieved it's roughly $900 million in revenue last year, that it's starting to be a contributor to take rate”.

Active accounts grew from 267M to 426M, thus driving the expansion of TPV (reaching $1.25T in 2021). The management expects TPV of $1.5T in 2022 as per the latest guidance and $2.8T by 2025, as per the Investor’s Day held in Feb 2021. A key contributor of TPV growth in 2021 was Venmo volume which increased by 44% (or $70B) to $230B.

In Q4’21, 9.8M Net New Active Accounts (“NNA”) were added, including 3.2M from the acquisition of Paidy and affected by 4.5M adjustment for illegitimate accounts. The NNAs were below guidance and John Rainey - Chief Financial Officer and Executive Vice President, Global Customer Operations, indicated on the latest earnings call that the 750M medium-term target is no longer appropriate. The focus will be on “sustainable growth and driving engagement” & “trying to retain high-quality users that largely come to us through organic channels and want to engage with us and increasing that engagement for those customers”.

Despite this, the Company still expects to add 15M to 20M Net New Active Accounts in 2022.

In our opinion, the “new” focus direction makes sense as user engagement has lower acquisition cost and thus higher ROI. A higher user engagement is expected to result to higher payment transactions per active account.

Non-GAAP EPS increased from $2.37 in 2018 to $4.60 in 2021 (CAGR of 24.7%). For 2022, Management expects a flat EPS of $4.60-$4.75, however, it confirmed its belief of achieving a CAGR of 22% for the medium term.

Cash position and cash generation

Cash & cash equivalents, and investments amount to $16.3B as of December 31, 2021, whereas debt totaled approximately $9.0B.

PayPal generated $6.3B cash from operations (up 8%) in FY’21 and returned $3.4B to shareholders.

Free cash flow of $5.4B for FY’21, up 9% and 21% of revenue. During the last 4 years the average FCF/Revenue was 21%. For 2022, FCF of $6B is expected.

6. Risks & Opportunities

Competitive advantages

Network effect: It connects merchants and consumers offering unique end-to-end product experiences and has a global scale of active consumer (392M) and merchant (34M) accounts across more than 200 markets.

PayPal is also the most accepted digital wallet. Dan Schulman, President and CEO: “Today, more than 70% of the top North American and European retailers, including more than 80% of the top U.S. retailers accept PayPal or Venmo at checkout”.

Source: PYPL Q4-21 Investor Update

Per Statista survey, the most widely used online payment service for 2021 in United States is PayPal with 85%, followed by Venmo with 32%, Apple Pay and Google Pay with 25%, Amazon Pay with 24% and Visa checkout with 16%.

Trusted Brands such as PayPal, Braintree, Venmo, Xoom, Zettle, and Honey.

Regulatory licenses around the world, including the payment business license in China (through GoPay acquisition).

Opportunities

Venmo deal with Amazon at checkout options. Management expects a +50% growth in Venmo’s revenue in 2022 (c. $900M in 2021).

Leveraging Paidy’s acquisition in Japan market ($5T economy, 4th largest ecommerce economy - ecommerce-sales-by-country ).

Buy Now Pay Later with Long term installments enabling higher user engagement (c. $7.9B volume in 2021, 12.2M unique consumer accounts and 1.2M Merchants with PayPal BNPL transactions) – figures do not include Paidy.

o As Dan Schulman noted “Buy Now, Pay Later is a perfect example of the type of investment we are making to give shoppers and retailers more reasons to engage with PayPal.”

o As John Rainey commented “we see an over 20% uplift in both of those [increased engagement and increased TPV] for customers that are using buy now pay later.”

Higher utilization / engagement of existing accounts. As John Rainey commented on the 4th Quarter Buyside call “there's a huge opportunity for PayPal in as much as our customers effectively only use us about half the time that they have the option to.”

Crypto checkout using PayPal and ability to buy/hold/sell crypto on Venmo.

Risks

Fierce competition in the fintech/payment solutions industry (e.g., Cash App and Square of Block Inc, Google Pay, Apple Pay, Afterpay – BNPL, Affirm – BNPL, Stripe, Skrill, Wise, Adyen etc.)

Forecasted growth in revenues for Q1 2022 of 6% raises concerns on future growth rates. Despite this, on an ex-eBay basis the expected growth is 14%.

Potential increases in credit losses due to expansion of BNPL offering.

Pressure on margins due to continuous reduction in Total Take Rate, though, Venmo is expected to positively affect take rates.

o As per Dan Schulman “And so, I think you just continue to see Venmo grow. And by the way, when it grows, obviously, its ARPU grows and as I mentioned in my remarks, it starts to add to our ability to grow take rates. Certainly, that adds to an upward pressure on take rate as opposed to a downward one.”

Macroeconomic factors: a) Sanctions imposed to Russia due to Russia/Ukraine war and uncertainty over any further escalation and b) supply chain issues.

7. Valuation

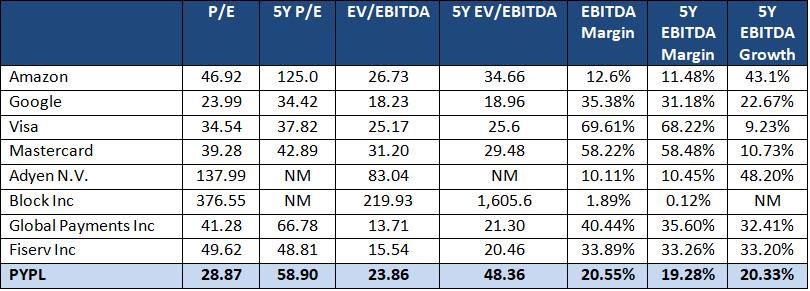

Note: GAAP P/E multiples were used

As per the above table, PayPal’s profitability multiples are well below their 5-year average, however, they stand at the mid-range relative to other big tech companies and other payment solutions companies (except its current P/E which falls in the lowest quartile). This makes sense as its EBITDA margin (current and 5Y average) is around the median level.

Despite the recent drop in price and multiples of PayPal, we still believe it is unlikely to observe a multiple expansion any time soon given the fierce competition in the industry and the low guidance provided for 2022, unless the Company demonstrates a higher-than-expected growth and/or improvement in margins.

On the other hand, PayPal is well positioned in the industry and should be able to benefit from the shift expected in E-Commerce sales as a %age of total retail sales.

Source: Statista

Method A

PayPal’s current Non-GAAP P/E stands at 23.23x with a 5Y average of 45.70x.

Management expects a non-GAAP EPS of $4.60-$4.75 for 2022, whereas from 2023 onwards to 2025 it was indicated that the medium target of 22% growth p.a. is achievable. As a result, by the end of 2025 we calculate a non-GAAP EPS of $8.49. Assuming a multiple P/E of 20x, yields an estimated price of $169.78. Compared to the current price (closing of 3/3/2021) of $101.34, an IRR of 13.8% is expected.

In case the multiple remains at current levels, i.e., 23x, the estimated price is $195.25 with an IRR of 17.8%.

The analysts’ expectations for 2025 non-GAAP EPS stand at $9.22 compared to $8.49 used in the calculation above. The fact that analysts’ expectations exceed Management expectations offers an additional margin of safety, however, any miss compared to such expectations might result to a short-term drop in prices.

Method B

PayPal’s current GAAP P/E stands at 28.87x with a 5Y average of 58.90x.

For the second valuation method we manually estimated and/or stretched the 2025 GAAP EPS using the following key assumptions:

We used Management projections relating to TPV of $2.8T by 2025 and stretched this to $2.5T.

The take rate was assumed to remain =<2%, despite the expectation of stabilization or even increase due to Venmo.

Transaction expense was kept at mid-80s, transaction losses were kept at similar levels as in 2021 (despite the steady decline of 3bps p.a. since 2018) and credit losses were maintained at 2018-2019 levels so as to exclude the reserve build and release observed in 2020 and 2021, respectively.

Taking the above into consideration we calculated a GAAP EPS of $6.22. Assuming a multiple contraction to 25x the estimated price is $155.40 with an IRR of 11.3%.

8. Investment thesis

Leader in digital payments with 426M accounts which provides room to an increase in revenue per customer through additional offerings (i.e. BNPL, Crypto). The shift of management focus from net new active accounts to Average Revenue per User and user engagement makes sense.

Network effect -> the high number of active users and merchants using PayPal makes the product more valuable to new users compared to other offerings, thus making the moat stronger.

Digital Payments and e-commerce sales are expected to grow in double digits in the next 5 years. PayPal will be one of the winners of this trend.

Profitable, growing and with strong financial / liquidity position.

The recent pullback in stock price makes the valuation appealing. We believe that PayPal could outperform the market in the next 5 years.

Thanks you for the analysis. Can you tell why Paypals ROIC is much lower compared to, for example, Visa/Mastercard? Of course these two are different kind of businesses as payment networks and paypal is a payment solution platform. Still what keeps paypals roic so low comparatively and do you see its getting better ?

Well done. Thanks.