PayPal’s Q1 2026 report represents the first look at the company under the leadership of President and CEO Enrique Lores, who has initiated a massive three-business-line realignment.

Let’s break down the results to see if this is a visionary leap or a desperate scramble.

1. Financial Results

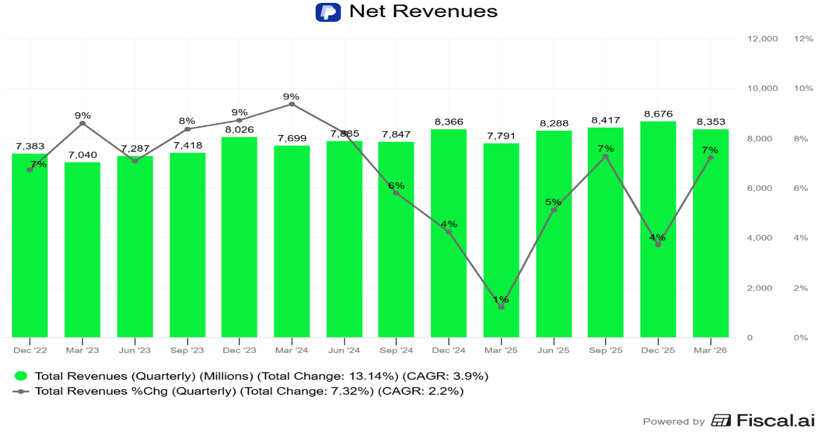

PayPal’s revenue increased to $8.4 billion in the first quarter, representing a 7% year-over-year increase (or 5% when adjusted for currency fluctuations). While this is an acceleration from the 4% seen in Q4’25, it is still low relative to the broader payments industry as the company continues to lose market share on its branded checkout business.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

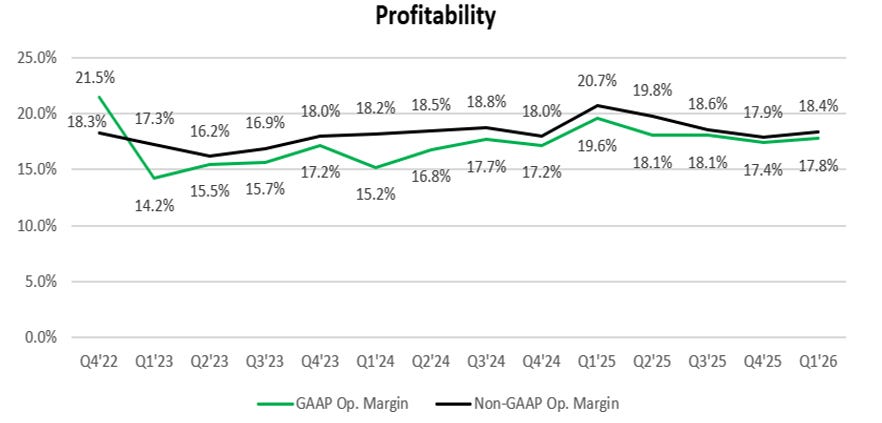

PayPal’s non-GAAP operating income fell 5% to $1.5 billion, resulting in a 229-basis-point contraction of the operating margin to 18.4%. This squeeze was primarily driven by an 8% surge in non-transaction related operating expenses, which exceeded the company’s initial guidance of a mid-single digit growth. Management attributed this spending spike to a strategic pivot to pull forward critical investments in AI technology, marketing and product development into the first half of the year. However, this margin erosion remains highly concerning, as it indicates that the core business is becoming structurally more expensive to operate.

Non-GAAP EPS was $1.34, up 1% YoY, as opposed to the company’s internal guidance of mid-single digit decline. This was largely boosted by the aggressive share repurchases reducing the number of shares.

Source: PayPal filings, StockOpine analysis

2. Payment Volume and Operating Metrics

a. Total Payment Volume

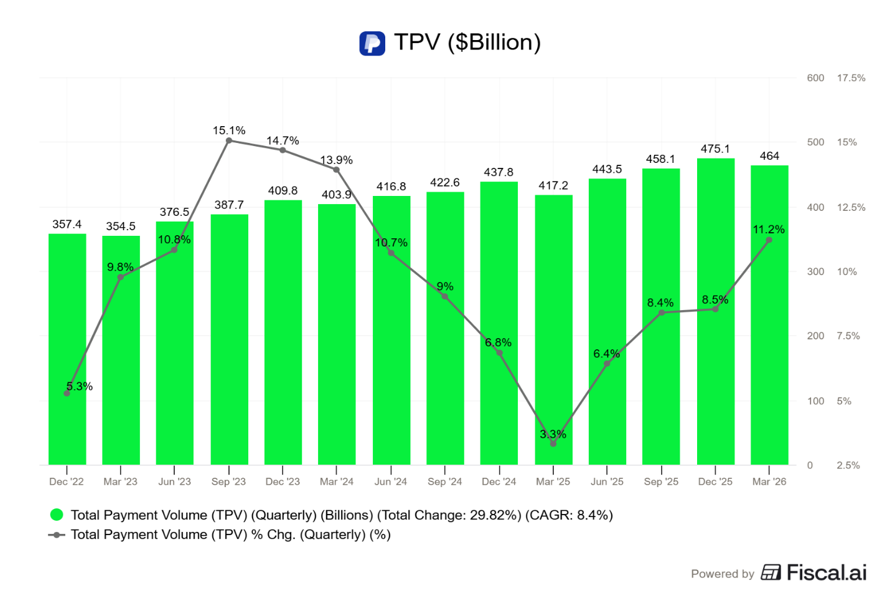

In Q1 FY26, TPV reached $464 billion, reflecting an 11% increase year-over-year (8% FXN), with growth driven mainly by PSP (Unbranded) and Venmo. Branded Checkout TPV grew at just 2% on a currency-neutral basis, a slight sequential improvement of 1%. When compared to Visa and Mastercard, whose payment volumes grew at 9% and 7% respectively, it is clear that PayPal's Branded Checkout continues to lose market share.

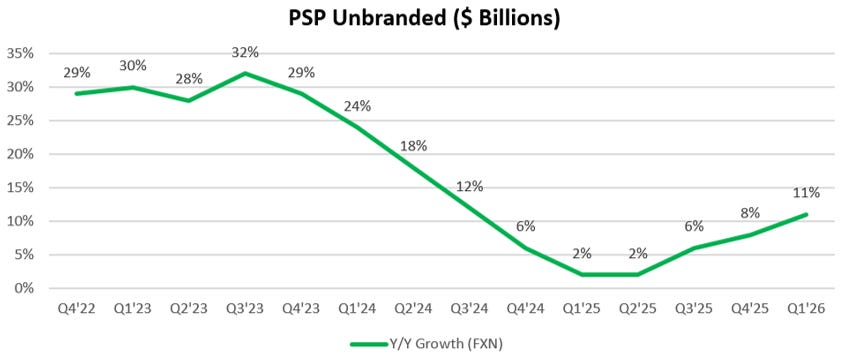

On the other hand, volume growth for PSP (Unbranded) accelerated to 11% (up from 8% in Q4’25). Within this segment, Enterprise Payments showed notable strength in the mid-teens, supported by high retention and growth within the existing merchant base.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Source: PayPal filings, StockOpine analysis

Growth was particularly strong in the US market, where TPV increased 11% year-over-year due to the combined momentum of unbranded processing (PSP), Venmo and core branded experiences. PayPal’s International TPV reached $163.8 billion, accounting for ~35% of the company’s total TPV. This figure represents an 11% increase on a spot basis year-over-year, though growth was a more modest 2% on a currency-neutral (FXN) basis. Management attributed the slowdown to the travel sector, broader macroeconomic softness, intense local competition and market saturation across Europe, particularly with persistent pressure in the U.K. and moderating growth in Germany.

To counter these challenges, management conducted deep-dive reviews and is rebalancing its focus toward the consumer side of the network. Key initiatives to revitalize international growth include the launch of the PayPal+ loyalty program in the U.K. and the aggressive scaling of localized checkout innovations, such as NFC-based solutions in Germany, to capture higher-value transaction verticals.

“There are also specific verticals, high-value verticals where we can have a more differentiated value proposition, especially we combine with financial services. This combined with an improvement in execution that by really understanding what our priorities are and simplifying how we make decisions, we think the combination of all that will have a significant impact in the business going forward” - Enrique Lores, CEO

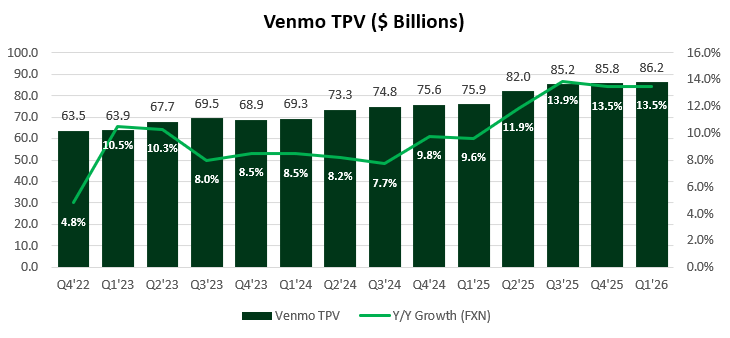

b. Venmo

Venmo continues to serve as a critical high-growth engine for the portfolio, delivering $86.2 billion in TPV for Q1, representing 14% FXN growth. This marks the platform’s sixth consecutive quarter of double-digit expansion that helped overall transaction margin dollar growth despite broader organizational headwinds.

Pay with Venmo surged 34% in the quarter. Though Venmo debit card and tap-to-pay adoption contribute a small share to branded experiences volume, they grew an impressive 60% year-over-year. Paypal’s Monthly Active Accounts (MAA) grew 1% to 225 million, but this growth was largely driven by Venmo, suggesting the core PayPal wallet may be seeing engagement fatigue.

Source: PayPal filings, StockOpine analysis