PayPal Q4'24 Earnings

"Transaction margin percent increased by more than 100 basis points for the second consecutive quarter, reflecting our focus on price-to-value and profitable growth."

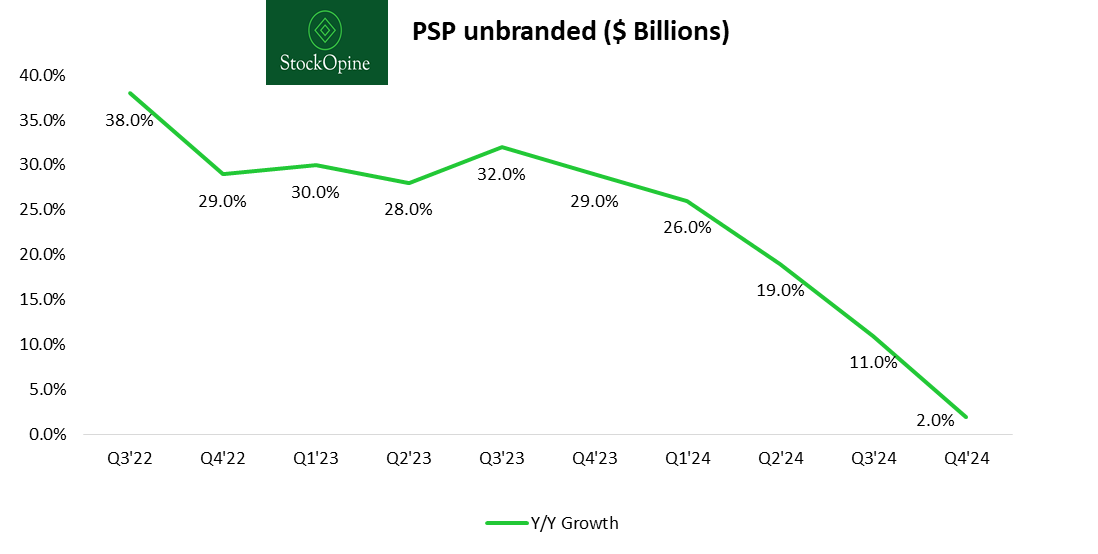

On Tuesday, February 4th, PayPal released its Q4 2024 results, triggering a share price drop of over 13%. The main reason? Unbranded card processing (primarily Braintree) saw its volume growth slow to 2%, down from 11% in the previous quarter and 29% a year ago. This was driven by PayPal’s price-to-value strategy, which aims to expand transaction margins in Braintree by shifting away from unprofitable growth.

Branded checkout grew by 6%, falling short of analysts’ expectations, while the projected transaction margin growth of 4-5% for FY25 is too low to offset these concerns.

Let’s break down the results to see if the sell-off was justified.

1. Financial Results

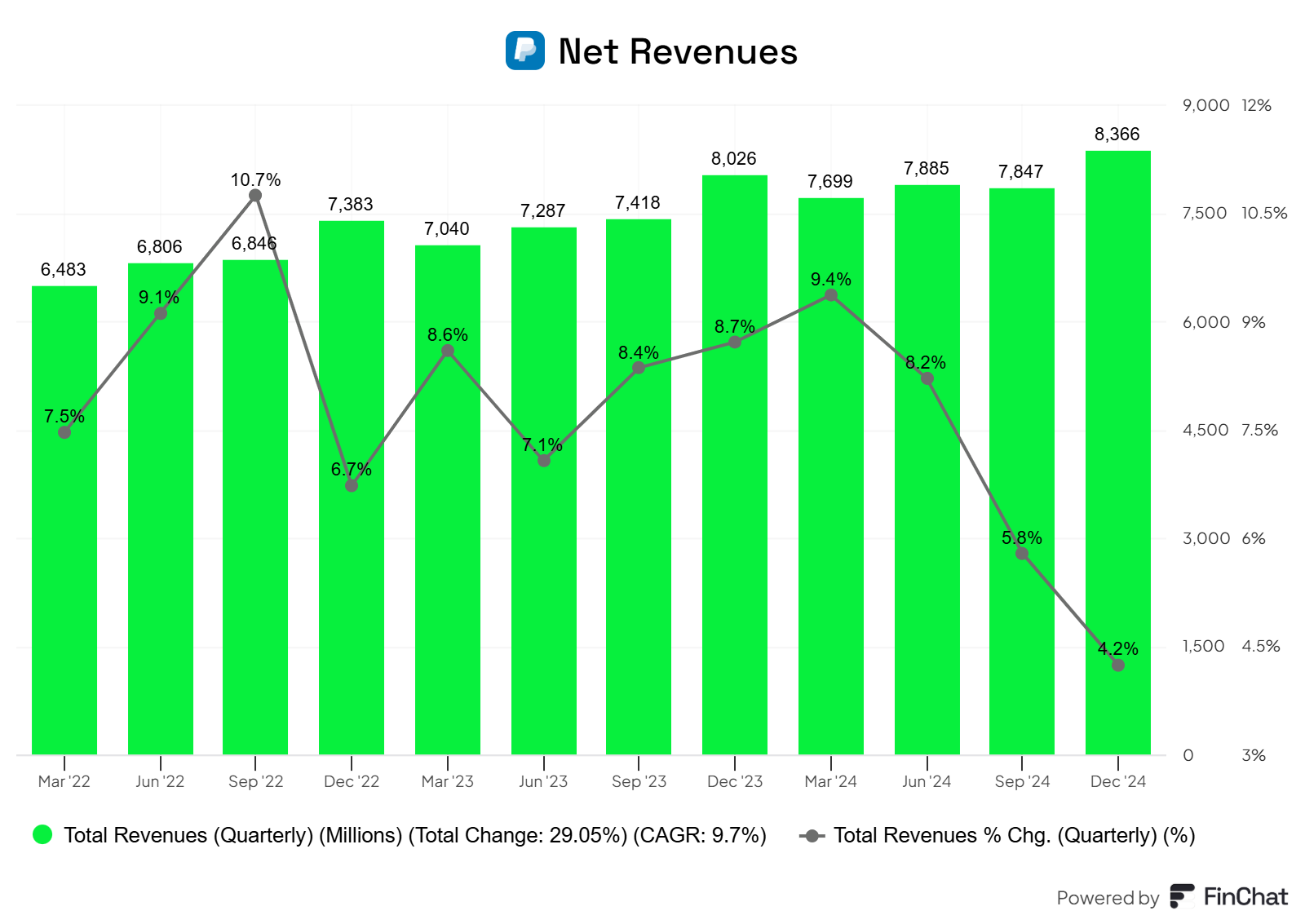

Revenue of $8.4 billion (up by 4.2% YoY) slightly above the consensus of $8.3 billion and in line with low single digit growth guidance.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

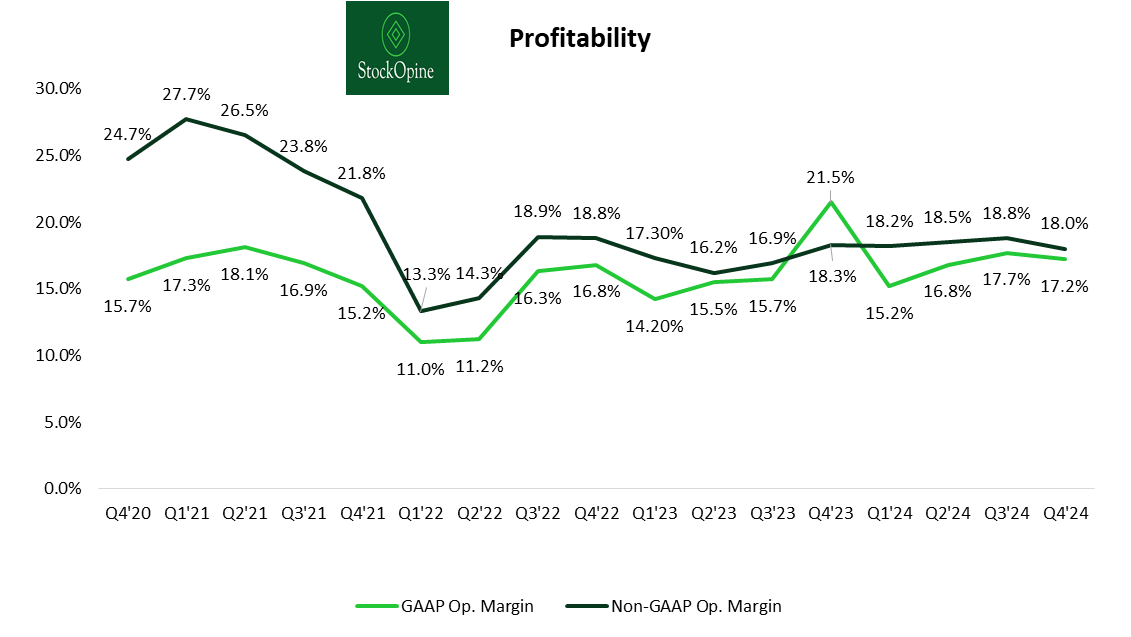

Non-GAAP operating income was $1.5 billion (up 2% YoY), surpassing the consensus estimate of $1.41 billion. This brought the operating margin down from 18.3% to 18.0%.

Non-GAAP EPS was $1.19, up 5%, exceeding the consensus estimate of $1.12 and the midpoint guidance of $1.09.

Source: PayPal filings, StockOpine analysis

In the latest quarter, transaction margins improved for the third consecutive period, rising from 46.6% in Q3 to 47% in Q4, also marking a 120bps improvement compared to Q4’23. However, non-transaction costs increased by 10%, up from 3% last quarter (management has previously communicated the expected increase in growth). For the full 2024, the main driver was marketing expenses, which added $250 million for the year (or 0.78% of sales), with a larger portion in the second half. For FY25, management anticipates a low single-digit increase in non-transaction expenses.

2. Payment Volume

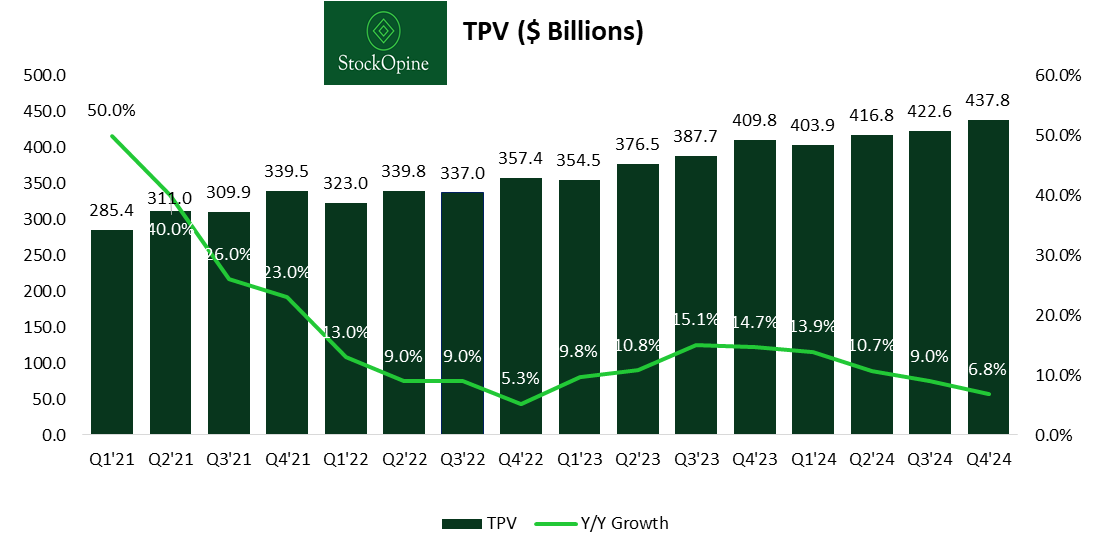

a. Total Payment Volume

Total Payment Volume (TPV) reached $437.8 billion, a 6.8% increase from Q4 2023, while yearly TPV totaled $1.68 trillion, reflecting a 10% increase. The growth in the quarter was driven by strong performance across all categories, except for unbranded processing, which continued its downward trajectory due to the price-to-value strategy.

Source: Company filings, StockOpine Analysis

Source: Company filings, StockOpine Analysis

The slowdown is concerning, even considering the price-to-value strategy. Management has delivered on transaction margin growth due to the shift in Braintree’s strategy, but as they’ve stated in both the previous and current quarter, they are prioritizing ‘healthy, profitable growth’. In our view, a 2% growth is far from healthy. However, as they lose market share (from around 95% of processing for a client to 75%) due to renegotiations, this slowdown seems inevitable.

So, what’s ahead? Deceleration will likely continue with major negotiations on the horizon, but transaction margins could keep improving. We would only see reacceleration once the renegotiation cycle is complete.

“Our conversations with merchants have become more holistic, moving beyond price and share of card processing to a deeper appreciation of our customers' needs and how we can add value through our full suite of solutions. We expect a handful of large Braintree merchant renegotiations to result in a headwind to revenue growth of about 5 points in 2025.

Shifting away from this volume pressures gross revenue but is accretive to transaction margin dollars and will result in more than 1-point benefit this year. We expect this benefit to build over time as we drive more value-added services. Over the next few quarters, we will continue to work through renegotiations, at which point we should reach a new baseline to drive faster volume and revenue growth.” Jamie Miller CFO

Ultimately, the question is whether we trust Alex Chriss to execute this plan. As of now, he’s performing well, so we’re giving him the time needed to deliver results. In this regard, we have to accept the revenue slowdown for a couple of quarters while we wait for the long-term benefits.

“For the first quarter, we expect flat to low single-digit revenue growth on a currency-neutral basis, which is heavily impacted by the Braintree renegotiation efforts I discussed earlier. This also includes about a 1-point headwind from lapping last year's leap day.” Jamie Miller CFO