PayPal Q4’25 Review: Sacking the Coach While the Scoreboard Bleeds

A leadership change can’t hide a stalling core business.

If you follow a football team that is struggling financially and underperforming on the field, the logical fix is finding better players or a new strategy to motivate the squad. Instead, PayPal’s Board just decided to sack the coach.

The shocker of the Q4 print wasn’t just the earnings miss, it was the abrupt, “effective immediately” appointment of Enrique Lores (former HP CEO) as the new President and CEO. This feels wrong. It feels reactive. While Alex Chriss may have missed on the core checkout button, he improved Braintree profitability, finally started monetizing Venmo, and stabilized the ship.

To replace him so suddenly raises questions. The official statement from Jamie Miller (Interim CEO) was standard corporate speak:

“The Board’s appointment of Enrique reflects a clear commitment to strengthening performance... At the same time, we recognize as a company that our execution has not been what it needs to be.”

But let’s look at the incentives. A simple comparison of the compensation packages is telling. Alex Chriss signed for equity awards around $43.75 million, while Enrique Lores is landing a package closer to $72.5 million. This raises further questions about the Board’s decision-making process.

Were the poor results merely a pretext to surface a conflict of interest? How does paying nearly double for a new CEO serve shareholders when the business is guiding for margin compression?

Let’s get into the numbers, because the guidance and the “execution issues” are where the real pain lies.

1. The Numbers: A Quarter of Misses

The Q4 print was weak, and no amount of adjusted metrics can hide the stalling growth engine.

Revenue: Came in at $8.68B, missing estimates of $8.79B. Growth of 4% is negligible for a “growth” fintech.

Non-GAAP Operating Income: $1.55B, missing estimates of $1.58B.

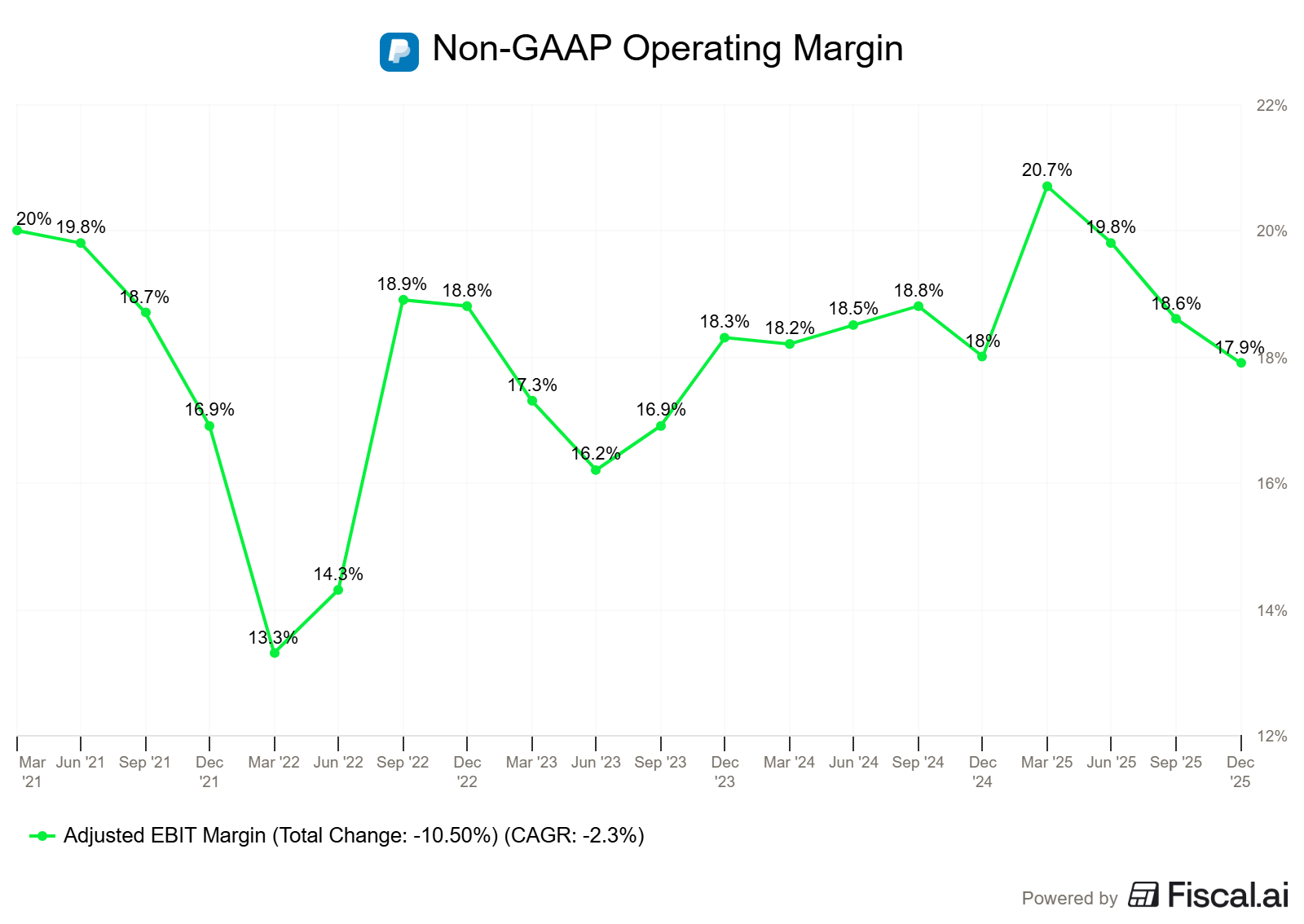

Operating Margin: Contracted 9 basis points to 17.9%. This is the lowest Non-GAAP operating margin we have seen in the past six quarters.

EPS: $1.23, missing the guidance of roughly $1.29. Management blamed a higher than expected tax rate, but relying on tax nuances to explain a miss is usually a sign of weak operational leverage.

Transaction Margin ($TM): The lifeblood of the company grew just 3% (or 4% ex-interest). This is well below previous implied estimates of 5-6%.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

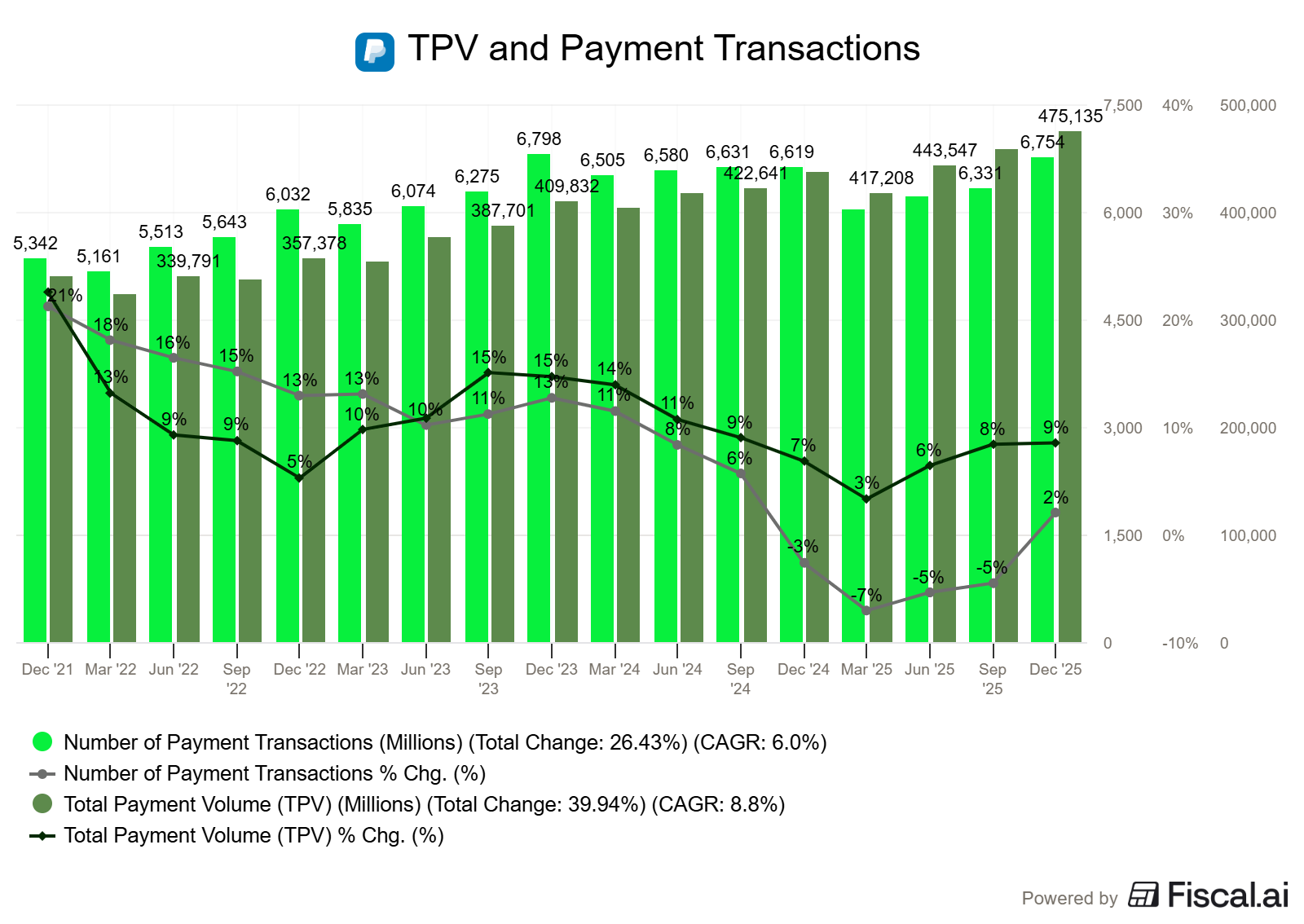

The volume picture is also discouraging. TPV grew 9%, while payment transactions increased just 2%. Excluding PSP (Braintree) volume, transactions rose 6%. That implies PSP transactions declined by roughly 13% during the quarter. It’s a clear hit to the volume narrative, though it does mark an improvement from the ~20% YoY decline seen in the prior quarter.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

a. The Core Problem: Branded Checkout is Stalling

The narrative has been turnaround for a long time, but the core cash engine Branded Checkout is slowing down. Branded Checkout TPV grew just 1% on a currency-neutral basis down from 5% in Q3’25.

Management blamed a list of external factors: US retail weakness, international headwinds in Germany, and normalization in travel/gaming. They always seem to blame external factors. To us, when you blame the “macro” while competitors are growing, it just implies market share loss.

Here is Jamie Miller, Interim CEO admitting the failure:

“The 4-point deceleration was more than we expected... First, U.S. retail weakness. We saw pressure across our retail merchant portfolio, particularly among lower and middle income consumers. While part of this can be attributed to macro factors... it’s also clear that we need to do more to win with key merchants.”

To reverse the trend, management announced a “change in approach” to focus on strategic merchants, who represent nearly 25% of branded checkout volume. They formed dedicated teams in January to serve them.

“To date, we’ve been optimizing for every merchant, and that approach has slowed our ability to move quickly on what matters most…We're changing our approach to focus on strategic merchants, representing nearly 25% of our branded checkout volume today but could be much larger.” Jamie Miller - Interim CEO

Focusing on large merchants sounds good on paper, but these players have immense bargaining power. If you are desperate to ‘win’ larger share of their wallet with dedicated teams and custom integrations, you are likely going to concede on pricing. This pivot further justifies the expectation of a drop in Transaction Margin dollars in 2026.

Moving to the redesigned checkout, we heard the biometric excuse. Management blamed operational deployment issues, noting that new checkout experiences were rolled out without biometric enablement.

“In too many cases, we were deploying our redesigned checkout without biometric enablement... That’s changing.” Jamie Miller - Interim CEO

Apple Pay has had biometric authentication figured out for years. It’s hard to understand why this wasn’t enabled by default in the redesigned checkout from Day 1.

As for progress, it remains slow. Management says only 36% of consumers are currently checkout-ready (biometrics/passkeys enabled), with a target of 50% by the end of 2026. Adding just 15% over a full year is underwhelming. By the time this rollout is complete, the technology risks being outdated.

b. Give Credit Where Due

It wasn’t all a disaster though. Ironically, the parts of the business that Alex Chriss focused on are the only ones working.

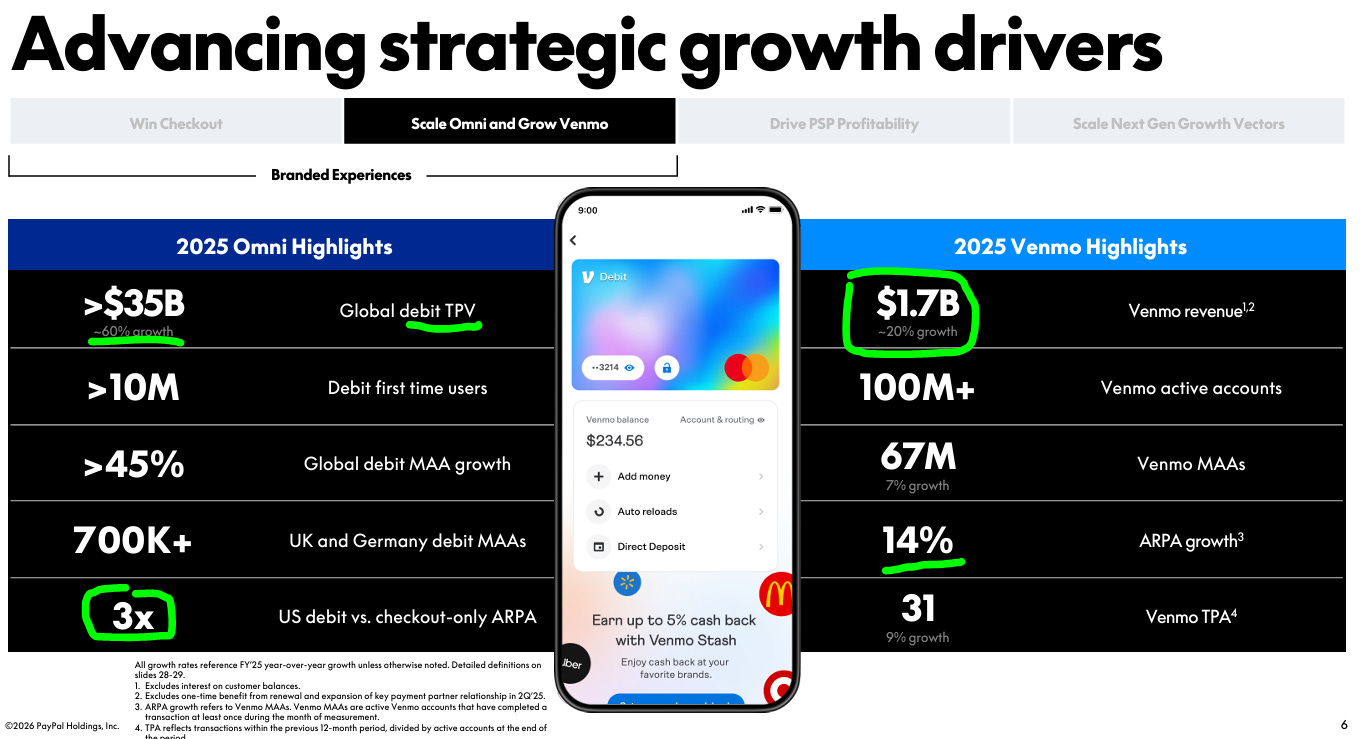

Venmo is finally making money: Venmo revenue grew ~20% to $1.7B (excluding interest income). Active accounts surpassed 100 million.

BNPL is scaling: TPV exceeded $40B (up >20%).

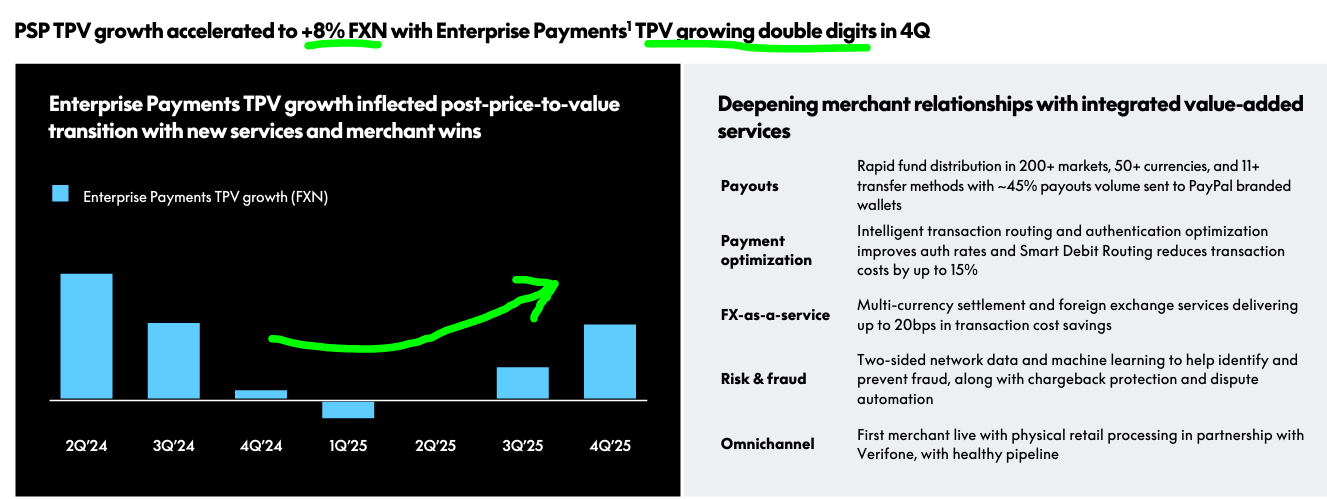

Enterprise Payments (Braintree): Returned to double-digit volume growth (+12%) and significantly improved profitability by doubling their net processing yield.

As Jamie Miller noted on the call:

“These 2 businesses [Venmo and Enterprise] were once small contributors to profitability. In 2025, they drove nearly half of our 6% transaction margin dollar growth.”

Source: PayPal Earnings Presentation Q4’25

Additionally, the PayPal Debit Card is showing clear signs of traction. In the US, TPV growth accelerated to over 50%, with MAAs (monthly active accounts) up 35%. Interestingly, US debit ARPA is roughly 3x that of a checkout-only user, reinforcing the importance of the omni-channel strategy.

Venmo’s debit card momentum is similarly strong, with TPV up more than 50% and MAAs growing 50%. While debit cards and Tap to Pay still represent a relatively small share of branded experiences volume today, their combined spend continues to scale rapidly, rising 60% YoY.

Source: PayPal Earnings Presentation Q4’25

c. The Innovation Distraction: Agentic & Visibility

Management spent time discussing “Agentic Commerce” and partnerships with AI platforms like Perplexity and Microsoft Copilot. While they admit this won’t materially impact 2026 growth, it feels like a buzzword distraction from the core fire in Branded Checkout.