Thesis in Brief

The Dislocation: PYPL trades at ~10x Forward P/E (near 52-week lows) despite accelerating Transaction Margin growth (+7%) and Venmo monetization (+20%).

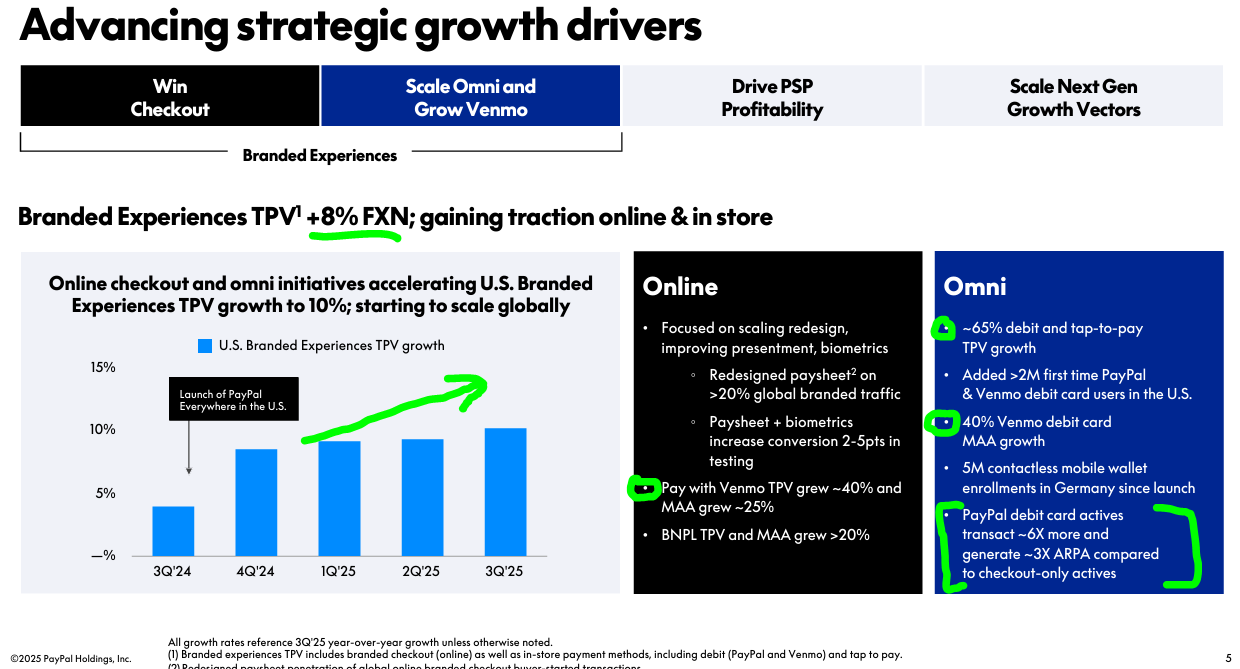

The Pivot: The “Checkout is dying” narrative ignores the 10% acceleration in U.S. Branded Experiences driven by debit/offline usage.

The Catalyst: 2026 is a transition year of investment (1-2% margin reinvestment), setting the stage for high-margin Ads and Agentic revenue in 2027.

The Verdict: We view this as a ‘Profitable Utility’ mispriced as a ‘Terminal Value Trap.’

1. Separating Signal from Noise

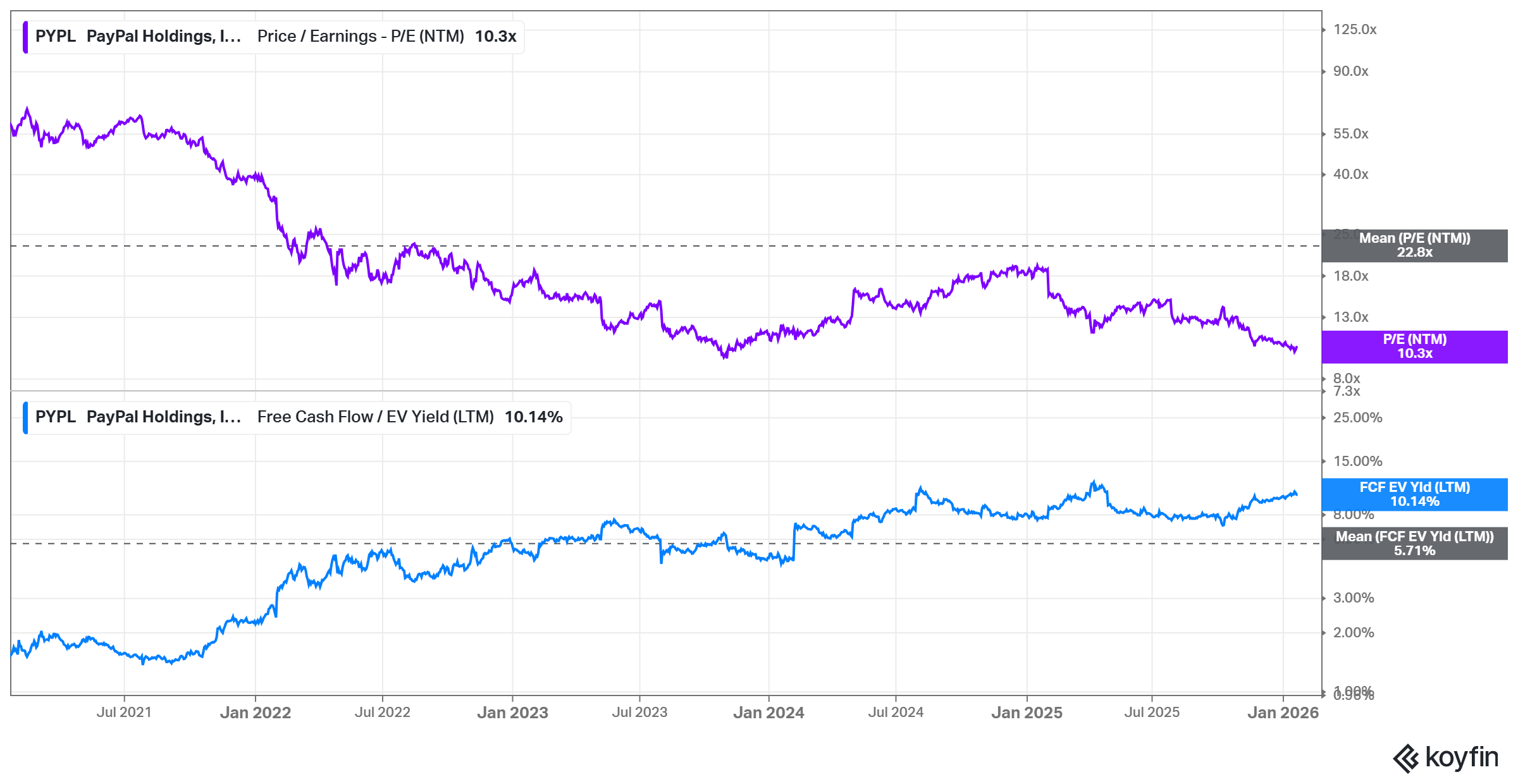

As we enter 2026, PayPal ( PYPL 0.00%↑ ) presents one of the most interesting setups in large-cap tech. The stock is trading near 52-week lows (~$57), pressured by a fresh wave of analyst downgrades in mid-January. Goldman Sachs slashed their target to $64 (from $72), citing market share erosion to Apple Pay. TD Cowen was even more severe, cutting their target to $65 (from $80), while Compass Point reiterated a sell rating with a target of just $55. The consensus is clear: PayPal is priced as a terminal utility with zero growth, facing regulatory overhangs and competitive moats it cannot cross.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

However, looking under the hood of the Q3 ‘25 results and recent strategic announcements, a different reality is emerging. The “growth at all costs” era is dead; the “profitable utility” era has arrived.

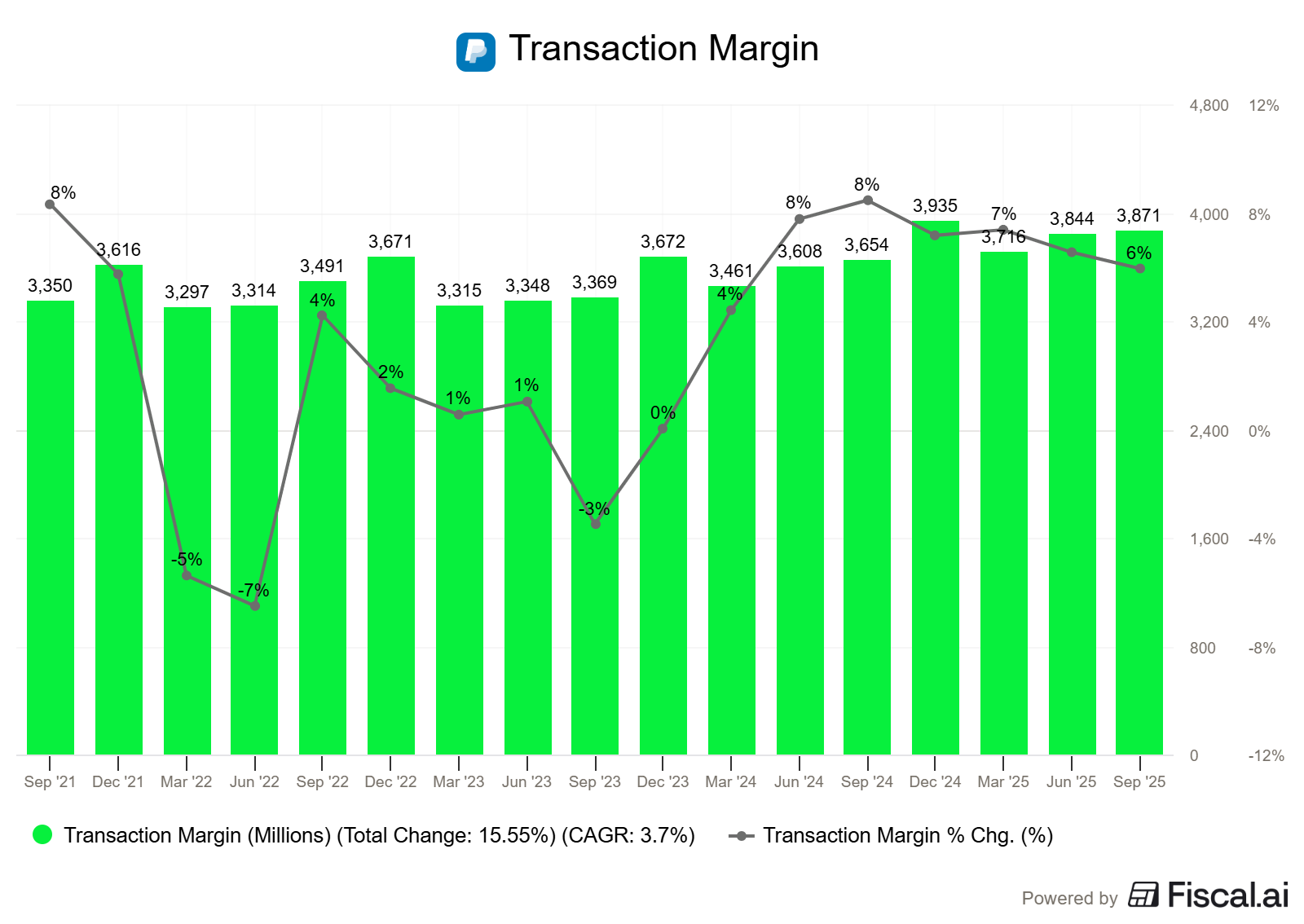

Transaction Margin Recovery: We are seeing a confirmed 6-7% growth in Transaction Margin dollars (ex-interest), proving the “price-to-value” strategy in Braintree is working.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Source: PayPal Q3’25 Earnings Presentation

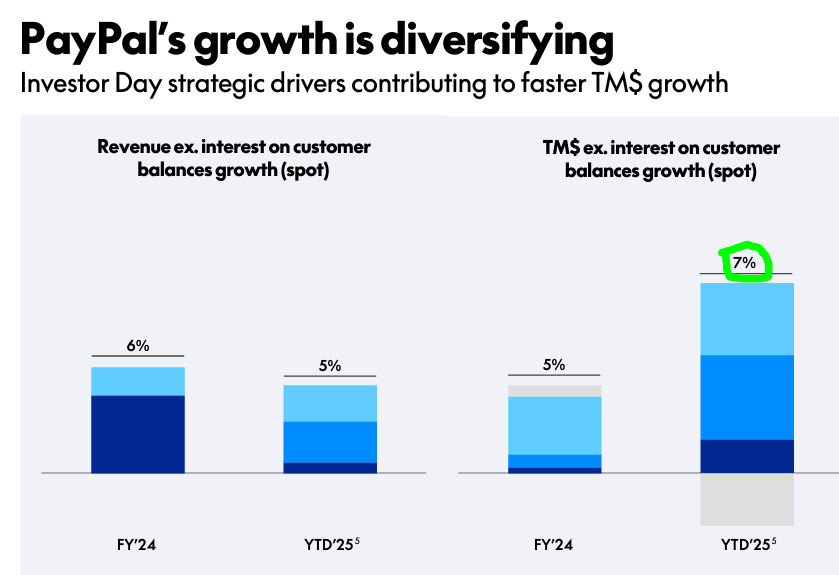

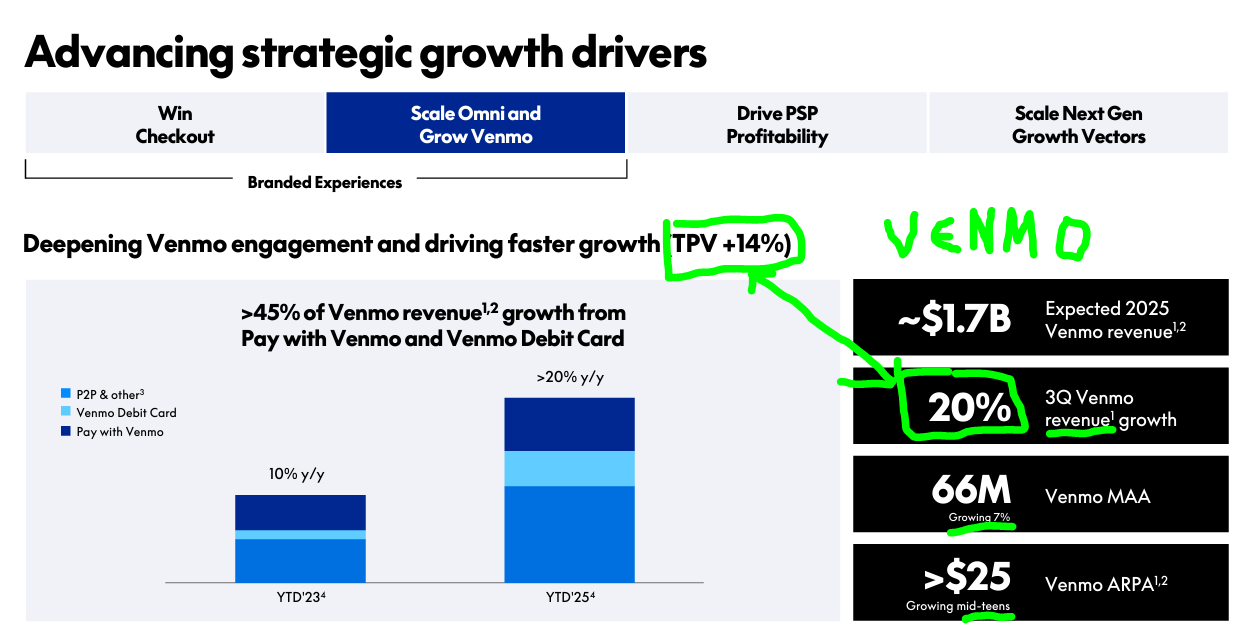

Venmo’s Monetization Inflection: Venmo is no longer just a free P2P app. The platform is pacing toward ~$1.7bn in revenue this year (ex-interest income, +20% YoY), driven by the expanding Pay with Venmo and Venmo Debit Card flywheel. Revenue growth of ~20% versus TPV growth of 14% points to improving monetization efficiency, with Venmo extracting more value per dollar of volume as scale increases.

As Alex Chriss has highlighted, this inflection is structural. At Investor Day, management guided to more than $2bn in Venmo revenue by 2027, noting that current execution positions the business to deliver well beyond that over time. Crucially, Venmo’s growth is margin-positive, with Chriss stating that it is accretive to transaction margin. TPV growth itself is also accelerating, reaching 14% in Q3, up from 12% in Q2 and 9% in 2024, reinforcing the durability of the monetization trajectory.

Source: PayPal Q3’25 Earnings Presentation

The primary bear case remains the slow rollout of the modern “Fastlane-style” checkout experience. CEO Alex Chriss was candid at the Citi conference, admitting that upgrading 15 years of legacy integrations is “slower than I expected”. Currently, the redesigned paysheet is live on roughly 25% of global traffic, with only about half of that fully optimized.

However, focusing solely on the legacy “Online Button” misses the structural shift to Branded Experiences (Omnichannel):

While global Online Branded Checkout is growing at a stable 5%, the broader Branded Experiences metric (which includes debit & tap-to-pay) is growing faster at 8% globally. In the U.S. Branded Experiences accelerated to 10% growth in Q3 (double the rate of the prior year).

Debit card and tap-to-pay volumes skyrocketed 65% YoY. We are seeing early wins like contactless payments in Germany (5M enrollments) and massive debit card adoption moving PayPal from a ‘guest checkout’ option to a daily spending tool.

The narrative that ‘Checkout is dying’ is incomplete and misleading. The legacy button has stabilized in the mid-single digits, while the new Omnichannel form factors are accelerating growth.

Source: PayPal Q3’25 Earnings Presentation

The ‘Agentic’ Call Option: Through new partnerships with Google, Microsoft, and OpenAI, PayPal is positioning itself as the trusted “vault” for AI Agents, a future revenue stream the market is assigning zero value to today. This also ensures that PayPal isn't disintermediated by AI agents.

This report updates our valuation model to reflect a “Transition Year.” 2026 will see suppressed margin expansion as management reinvests to lock in users. Jamie Miller, CFO, was explicit about this tradeoff at the UBS conference:

“So first, fourth quarter, we said we would invest 1 to 2 points of transaction margin dollars back into the space around product attachment and habituation. And that is really what we’re focused on when we get into ‘26. ‘26 for us around investment in branded checkout is product attach and habituation and it’s about Agentic Commerce and making sure that we can really lean in there and be a first mover to capture that shift.”

We are weighing the near-term pain of these investments (rewards, ads, and offers) against the long-term potential of two potential flywheels:

PayPal Ads: A high-margin ad network built on first-party transaction data.

PayPal World: The cross-border wallet initiative. While adoption is in early stages, Bank of America recently highlighted its potential, estimating that hitting adoption targets could generate approximately $365 million in annual incremental revenue.

Is the market right to panic over Apple Pay, or is it missing the quiet compounding of the most diversified payments platform in the world? Let’s dive into the numbers.

2. Valuation

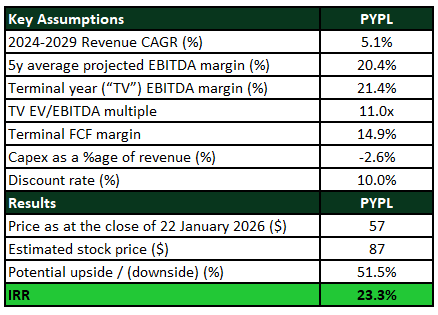

Below we outline our estimated fair value and key assumptions. Paid subscribers get full access to the underlying assumptions, valuation model and sensitivity analysis. Join StockOpine for the complete view.

The stock price as of 22nd of January 2026 stands at $57 with 1 year return of 36.4%. The Company’s market capitalization is $54B and it trades at an EV/EBITDA TTM multiple of 7.7x. Based on our DCF valuation, the estimated price of PayPal is $87, 51.5% higher than its current price, with an expected IRR over the projected period of 23.3%.

Source: StockOpine analysis / This table can be found in tab ‘Key Assumptions’