POOL Corp Q2’25: Eyes on recovery

Revenue growth turns positive for the first time in two years

POOL reported second quarter 2025 results that were largely in line with expectations, signaling a potential end to a challenging downcycle. While the discretionary side of the business (new pool construction and remodeling) remains under pressure from the high-interest-rate environment and the post-Covid-19 recovery, the non-discretionary maintenance segment showed its resilience.

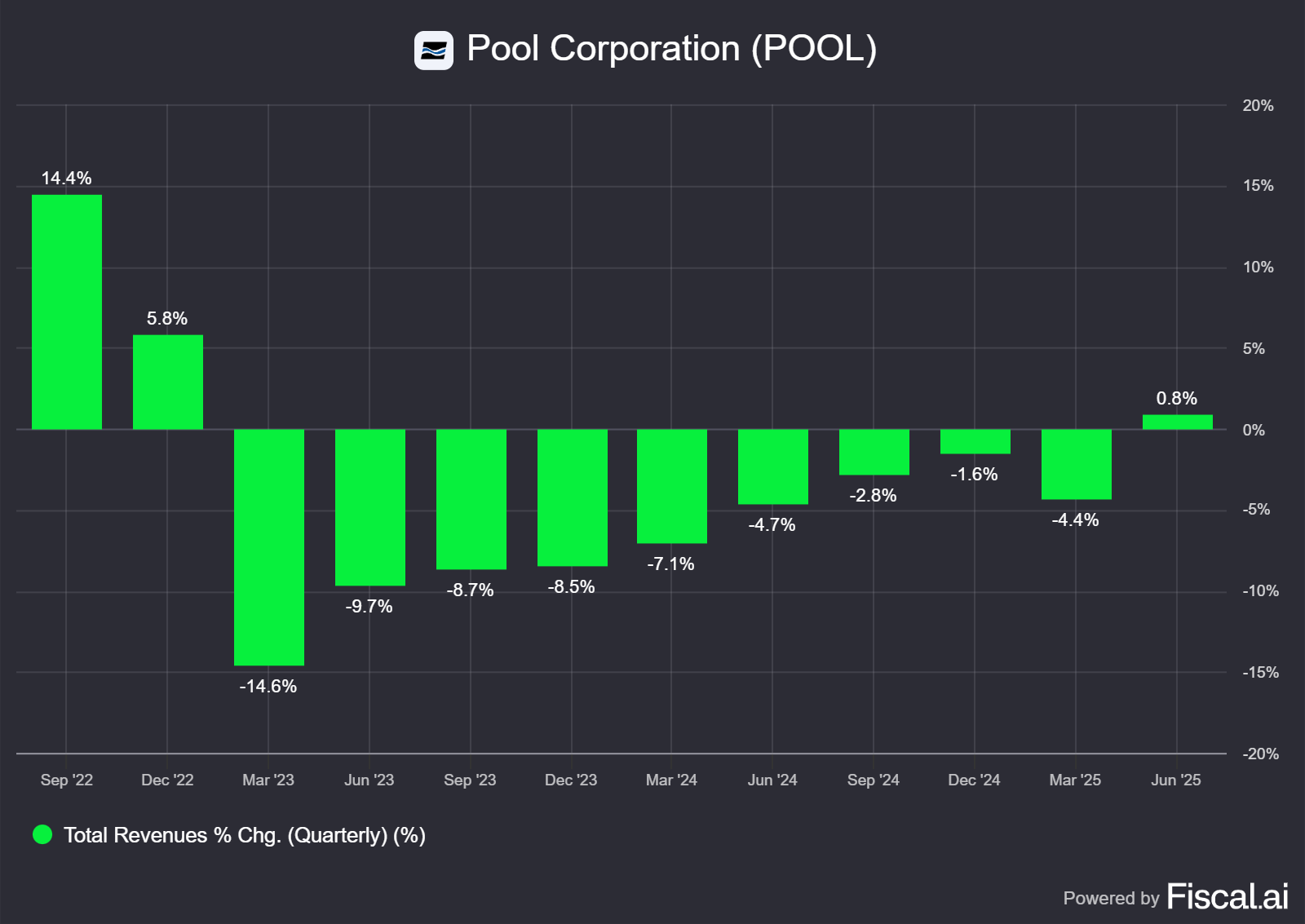

The key takeaway from the quarter is a story of stabilization. After nine consecutive quarters of decline, revenue growth has finally turned positive. However, management tempered enthusiasm by lowering its full-year sales and EPS guidance, acknowledging that the anticipated recovery in new pool construction and remodeling has yet to materialize.

1. Revenue

Net sales for the quarter were up 1% year-over-year reaching $1.78 billion, a modest but significant improvement as it marks the first year-over-year increase in over two years.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

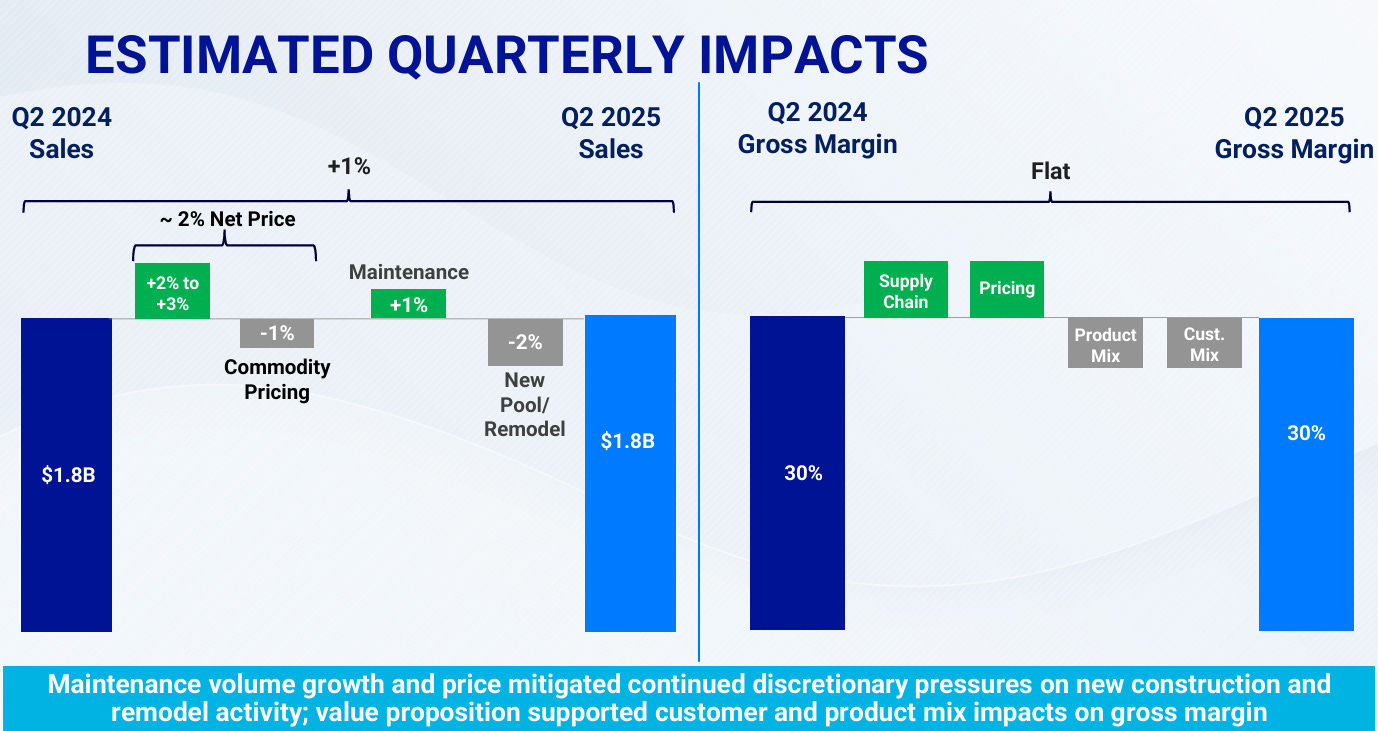

This growth was primarily fueled by the the maintenance business, which contributed 1% to overall revenue growth, and a 2%-3% benefit from price realization. These gains were partially offset by a 1% headwind from deflation in chemical prices and a 2% drag from the continued softness in new construction and remodel activities.

Source: Pool Corporation Q2’25 Earnings Presentation

Maintenance Vs New Construction

The core Maintenance business performed well, with growth in both volume and price. Considering the 2% headwind on growth from overall New Construction/Remodel, we estimate that maintenance revenue grew in the range of 4% year-over-year.

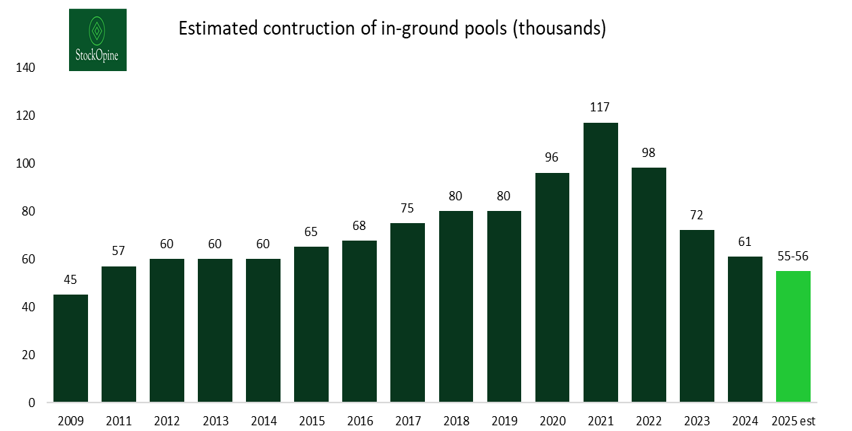

On the other hand, New Construction & Remodel was a 2% headwind to overall growth, an improvement from the 3% drag in Q1. This implies an underlying year-over-year revenue decline of 5–6%, which is better than our Q1 estimate of an 8–9% drop and the high single-digit decline indicated by new pool permit data. The permit data suggests that new pool construction is down high single digit, which implies that the construction of in-ground pools could hit a 15-year low in 2025, falling below 2011 levels.

Source: Pool’s 10K filings, StockOpine analysis

Maintenance constituted approximately 64% of sales in FY24, up from 62% in FY23 and 58% during the construction peak in 2021. This shift highlights the company's reduced reliance on the more cyclical parts of its business. This trend shares similarities with the financial crisis when the maintenance mix grew from an estimated 55% of sales at the housing bubble peak to 70% after the collapse, cushioning the overall revenue decline. During the current cycle, Pool's revenue has declined 14% from its 2022 peak, a less severe drop than the 20% decline seen between 2006 and 2009.

2. Gross Profit Margin

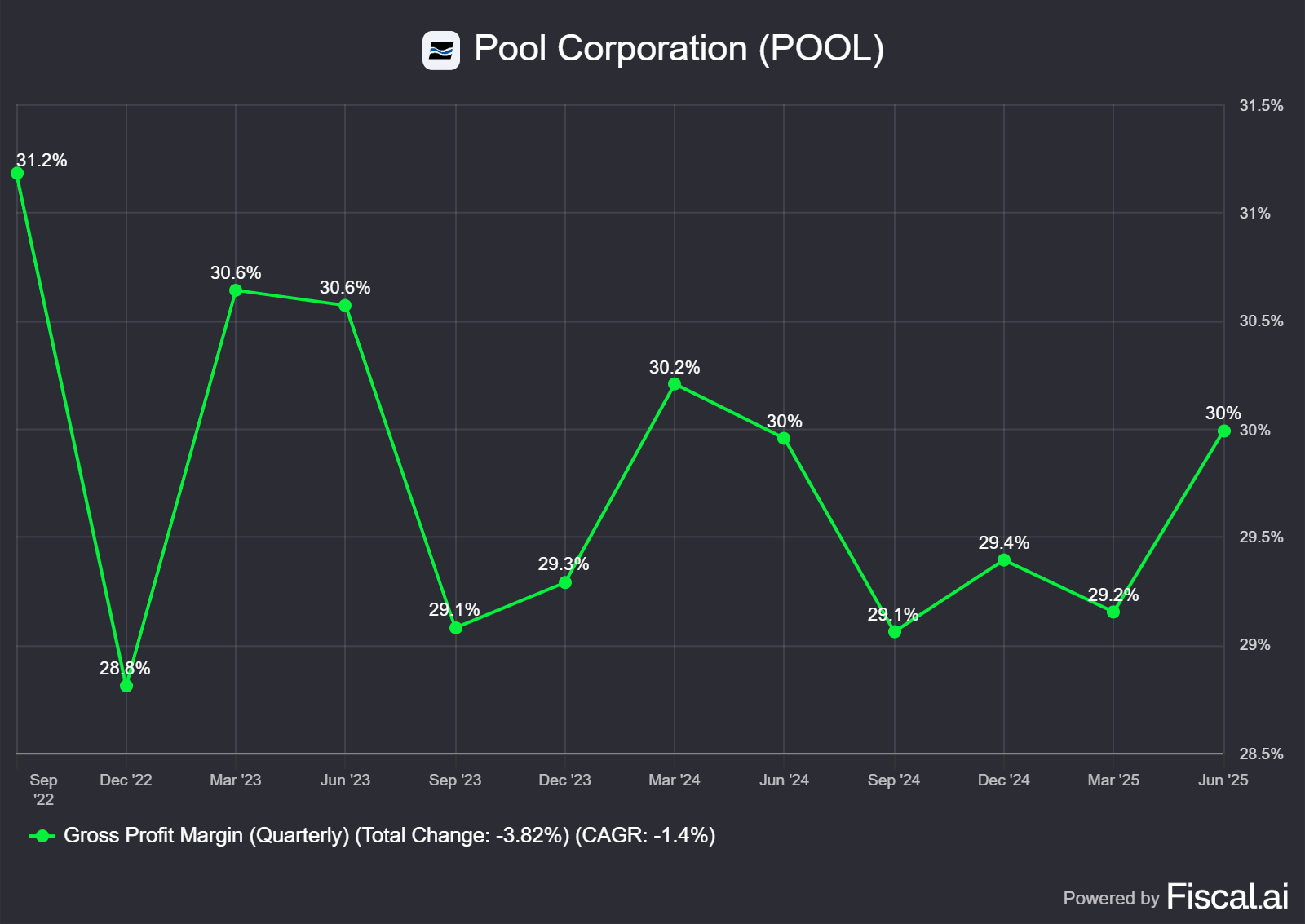

Gross margin for the quarter came in at 30%, flat year-over-year and a sequential improvement from 29% in Q1. The 30% level is in line with management's long-term target.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Incremental gross profit margin improvement was driven by strong performance in higher-margin private label chemicals and moderating headwinds from building material (building materials carry higher margin) as well as by price increases implemented late in the quarter.

In late April and early May, following the announcement of new tariffs, vendors raised prices on certain products. POOL was able to pass these increases on to its customers late in the quarter, which contributed to the overall price realization and is expected to provide more benefit to margins in the second half of the year.

“So as we look out for the balance of the year, we'll see a little bit of margin benefit from some of those incremental prices in the third and fourth quarter. And then we'll also see a little bit of improvement from the year-over-year change in the building materials as that started to moderate when you compare it to prior years.”

3. Operating Margin

Operating margin was 15.3%, consistent with the prior year, as operating expenses grew in line with revenue. This reflects solid cost discipline, especially considering wage inflation and the expenses associated with opening new locations. During the quarter they opened 8 new locations contributing around 1% to the expense increase.

4. Performance by Product Category

Chemicals: Sales grew 1% despite a 1% price deflation, driven by strong volume growth in private label products which helped offset lower prices for chlorine commodities like trichlor. Cooler weather in May and early June in certain markets was also a headwind for chemical sales.

Equipment: Sales were up 1%, reflecting stable volumes and modest price increases.

Building Materials: Sales declined by 1%, but this was a sequential improvement from the 5% decline seen in the first quarter, suggesting stabilization.

5. Other End Markets

Independent Retail: Sales to independent retailers declined by 3%, impacted by weather headwinds in northern markets during May and early June that dampened DIY maintenance activity. Trends reportedly improved in the latter part of June.

Pinch A Penny: The franchise network saw a 1% sales increase, outperforming the broader retail segment due to its concentration in Florida, which experienced favorable weather. The network added 5 new stores, in line with its annual target of 10-12 new stores, bringing the total to 302.

Commercial: The commercial business was a bright spot, with sales up 5% year-over-year, supported by ongoing investments in the commercial team. Commercials continue to gain share in the mix (increased from 4% of sales in FY23 to 5% in FY24).

Regional Performance: Florida and Arizona saw 2% sales growth, outperforming the national average. In contrast, Texas and California were down 2% and 3% respectively, impacted more heavily by the new construction slowdown, though maintenance remained resilient in these markets.

6. Updated 2025 Outlook

Reflecting the persistent weakness in discretionary spending, management updated its full-year guidance.

Sales: Now expected to be flat compared to the prior year (previously: flat to low-single-digit increase).

Gross Margin: Expected to be in line with the prior year.

SG&A: Expected to increase by 2% to 3% for the full year.

Diluted EPS: Lowered to a range of $10.80 to $11.30 (previously: $11.10 to $11.60).

Management attributed the lowered EPS guidance to the fact that anticipated interest rate cuts (to which discretionary spending is sensitive) in the first half of the year did not occur.