When we covered Pool Corp in Q3’25, we called it the quarter of stabilization, with green shoots signaling a potential revenue acceleration. However, heading into Q4’25, Pool missed expectations on both the top and bottom lines, leading to a further decline in the stock. It is now down 6% YTD, trading at historic decade lows of 14x NTM EV/EBITDA compared to its 10-year average of 19.5x.

Source: Koyfin

But it wasn’t all bad. The quarter was fundamentally a story of tough comparisons. Pool faced a massive headwind in Q4'25 as it cycled against the hurricane-driven surge in Florida from late 2024. Despite this, the company delivered a 70-basis-point expansion in gross margins and introduced a 2026 outlook projecting a return to low single-digit top-line growth.

We’ll dive into the specific drivers behind these numbers below.

Support for this research is provided by our sponsor, 9fin.

9fin event with Kobre & Kim: Past the turning point — Enforcing defaulted private credit loans onshore and offshore

9fin and Kobre & Kim invite you for a webinar on March 24 at 9am ET, examining what happens when restructuring is no longer viable, and how creditors can pursue recovery through arbitration and global enforcement strategies.

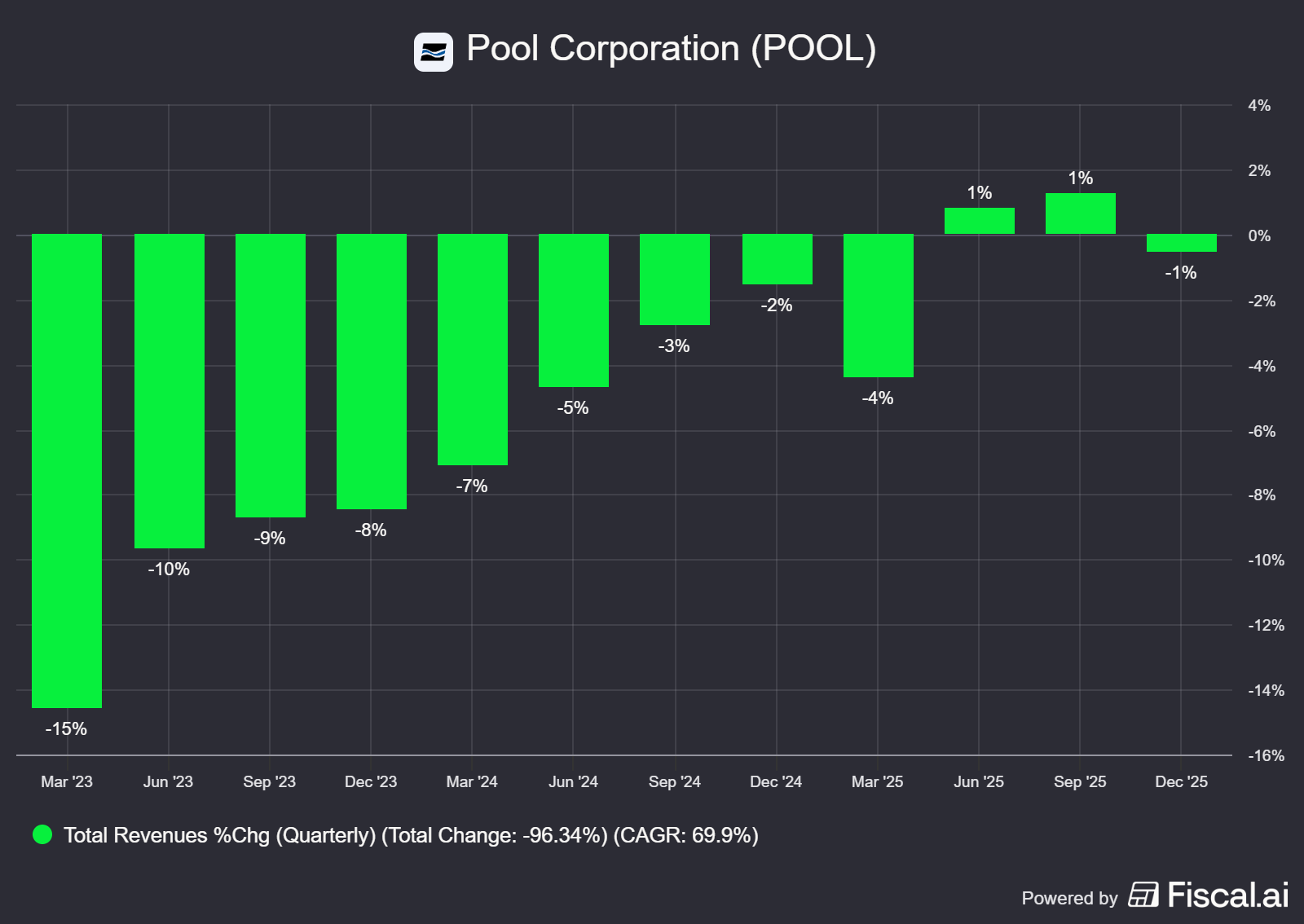

1. Revenue

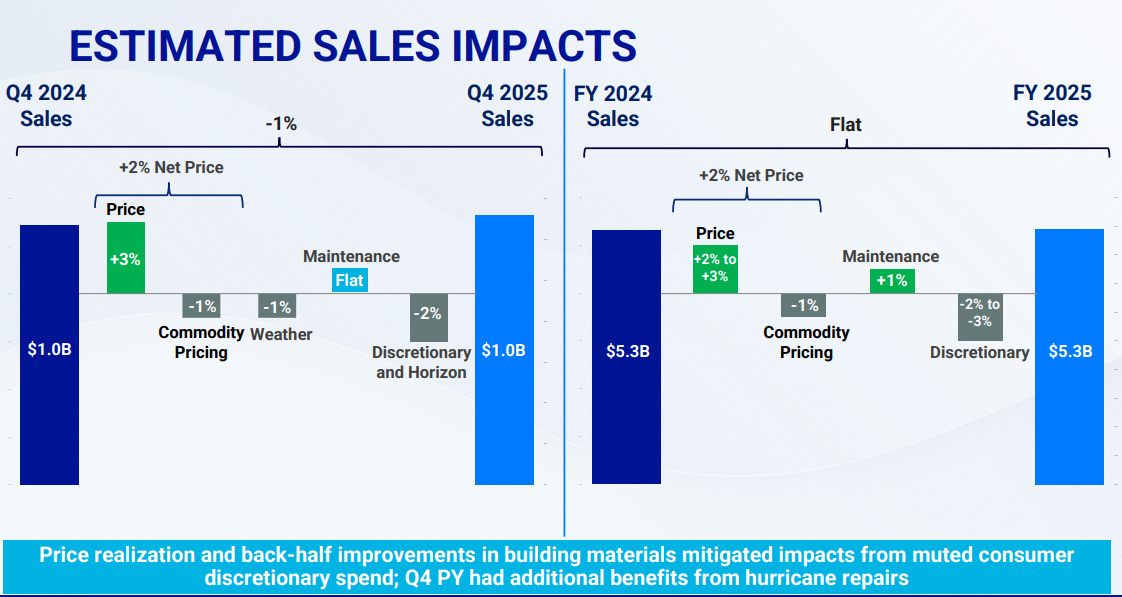

Net sales for the quarter were $982.2 million, a modest 1% decrease year-over-year. This slight decline was largely expected, as Q4’24 included a 2% benefit from hurricane recovery efforts. Excluding the impact of that tough repair comparison in Florida, the positive growth trends we saw over the last two quarters would have continued.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

This quarter’s revenue dynamics were driven by a +2% benefit from net pricing, which helped offset a -2% drag from lower discretionary spending.

Source: Pool Corporation Q4’25 Earnings Presentation

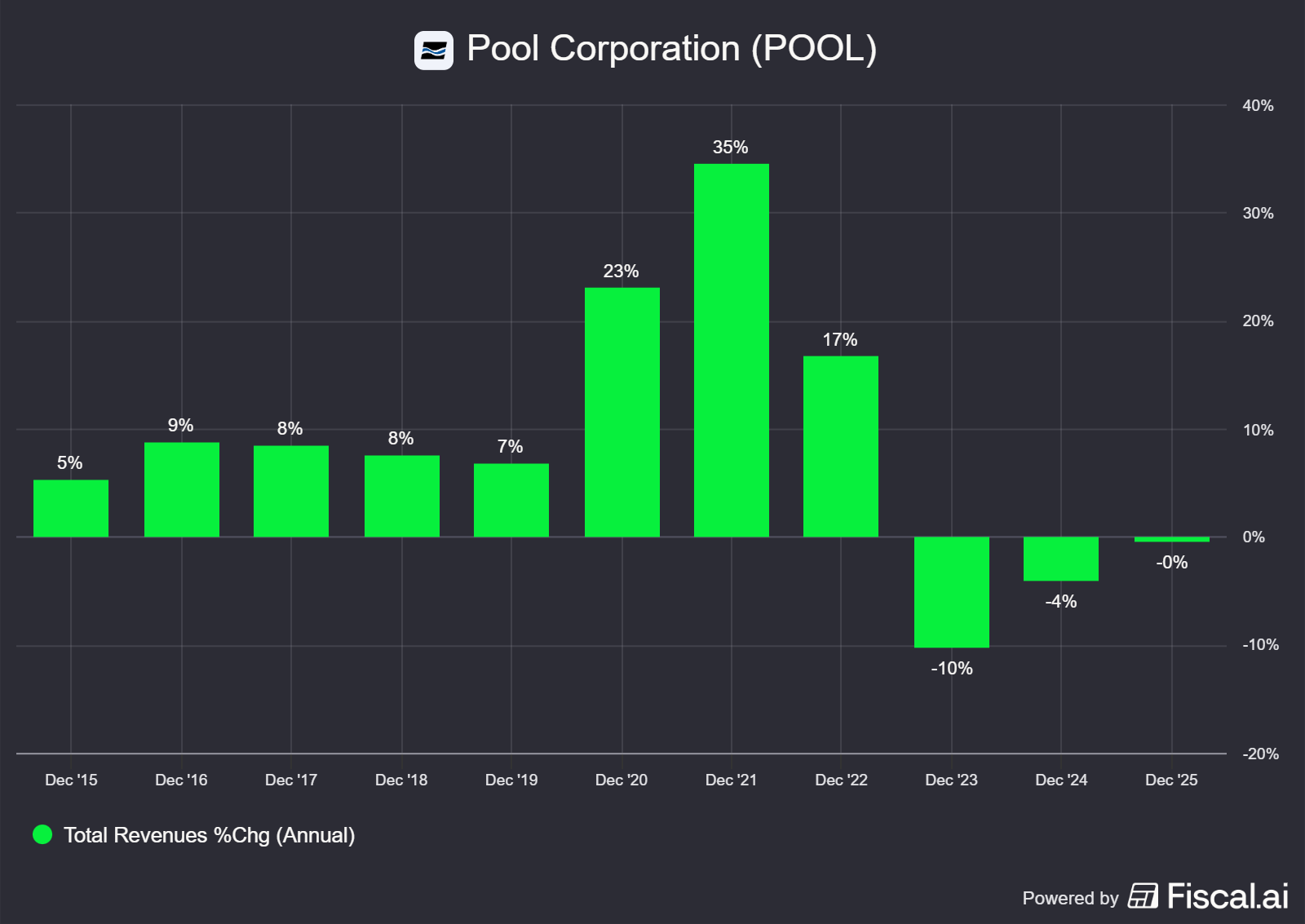

For the full year, Pool achieved $5.3 billion in net sales, finishing flat compared to FY24 and reflecting a true year of stabilization. The industry has been in a broader decline for three consecutive years, fighting the hangover from the pandemic demand surge as well as a restrictive interest rate environment.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

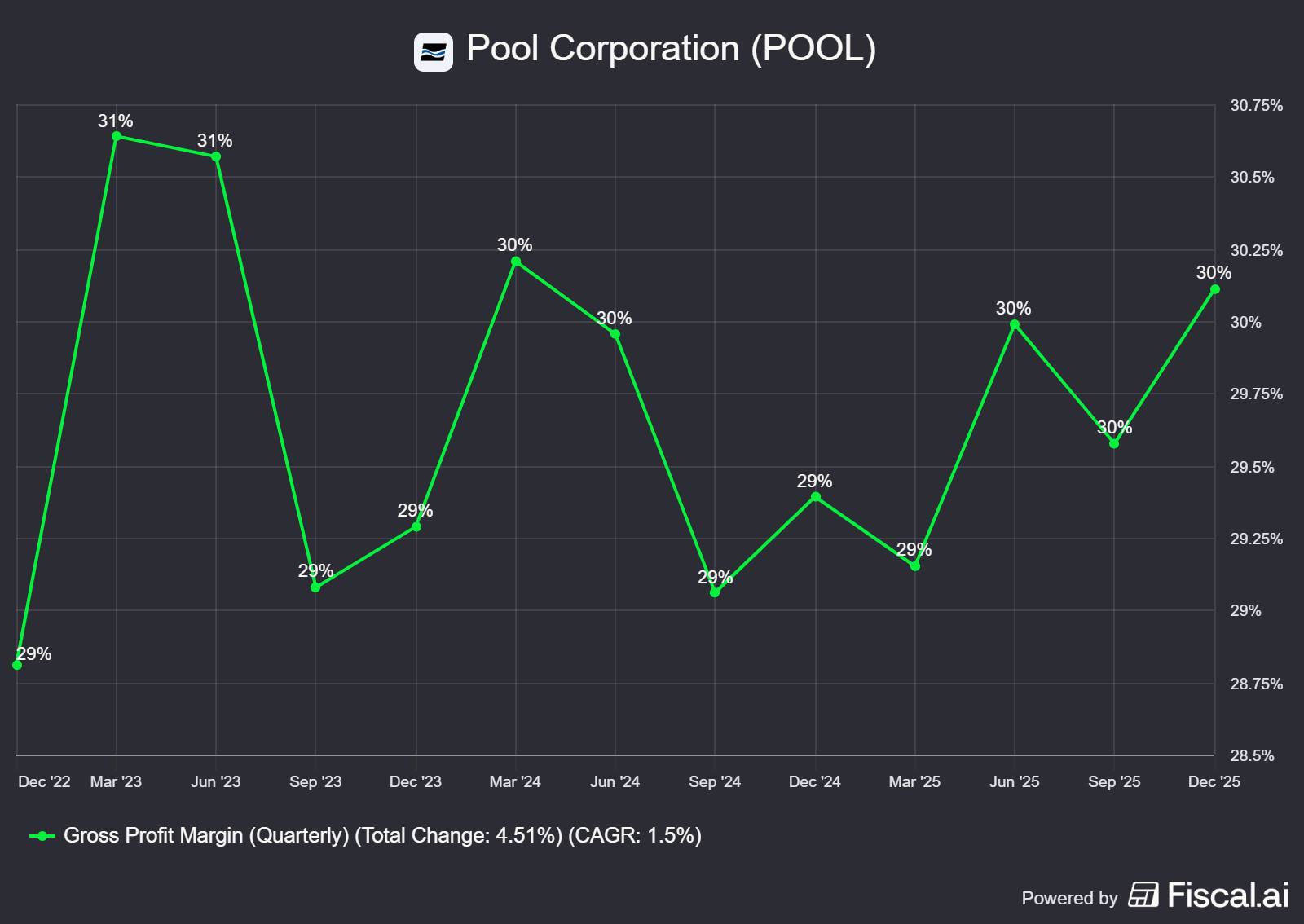

2. Gross Profit Margin

Gross margin for the quarter was a major bright spot, coming in at 30.1%. This represents a robust 70-basis-point expansion compared to Q4’24.

This margin expansion was fueled by disciplined pricing, supply chain benefits, and an increase in private label sales. The company also benefited from a favorable product mix compared to last year, as Q4’24 saw an unusual spike in lower-margin equipment sales related to post-storm replacements. For the full year, gross margin landed at 29.7%.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

3. Operating Margin

Operating margin for the quarter contracted by 80 basis points to 5.3%. Operating income came in at $52.0 million.

Operating expenses increased by 6% to $243.7 million. This expense growth was primarily driven by incremental investments in the POOL360 Unlocked technology rollout, costs associated with new greenfield sales centers, and rising self-insured medical costs.

For the year, operating income reached $580.2 million (11.0% operating margin) compared to $617.2 million in the previous year (11.6% operating margin)

4. Performance by Product Category

The Q4 product mix highlights the impact of the 2024 hurricane comps:

Building Materials: Sales grew +4%. This marks another solid quarter of growth, driven by demand for National Pool Trends products. The trend continues from Q3'25 where we saw another +4% YoY gain.

Equipment: Sales declined -3%. This drop was directly related to cycling against the significant equipment replacement activity following the major hurricanes in Q4’24.

Chemicals: Sales fell -3%. This reflects both a tough comp with post-hurricane cleanup and continued pressure on chemical pricing.

5. Other End Markets

Independent Retail: Sales to independent retailers declined by 4% in the quarter. This reflects softer retail demand compared to the hurricane-driven surge late last year.

Pinch A Penny: The franchise network saw a 9% sales decline. This was heavily impacted by geographic concentration; most stores are in Florida, and Q4’24 saw a 15% jump in sales from hurricane activity. The network itself continues to expand, crossing the 300-location mark.

Commercial: Sales fell -4% for the quarter, but finished the full year up +3%.

Regional Performance: Florida declined 9%, heavily skewed by the tough comp, though it remains up 2% on a two-year stack. Texas provided early signs of recovery, growing +1% in Q4. California and Arizona declined 4% and 3% respectively.

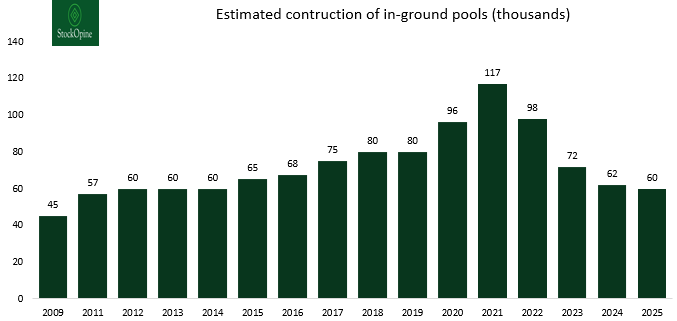

6. New Construction Vs Maintenance

The industry saw just under 60,000 new pools built in the U.S. in 2025, representing a mid-single-digit decline from 2024. This is 25% lower than the pre-pandemic period and closer to the post-financial crisis years.

Source: Pool Corp 10-K Filings, StockOpine Analysis

Looking into 2026, management noted an encouraging level of optimism from dealers following the January show season. Many builders expect to construct at least as many pools as they did in 2025, indicating that the new construction market has likely found its floor.

For FY25, maintenance revenue was 64% of total revenue, while renovation and remodel made up 22% and new pool construction contributed 14%. This compares to maintenance revenue of 62% in FY23 and 58% during the construction peak in 2021. As mentioned in previous posts, this trend shares similarities with the financial crisis when the maintenance mix grew from an estimated 55% of sales at the housing bubble peak to 70% after the collapse.

7. 2026 Outlook

Management is expecting return to growth in 2026.

Sales: Expected to grow in the low-single-digit range.

Pricing: Anticipated to provide a +1% to +2% benefit.

Gross Margin: Forecasted to be consistent with 2025 levels at 29.7%.

Diluted EPS: Guided to a range of $10.85 to $11.15. This excludes any potential ASU tax benefits, implying growth in the low-single-digit range.

8. Quick Take: The POOL360 Digital Advantage

Pool’s continued investment in its B2B digital ecosystem is paying off.

Record Adoption: For the full year, POOL360 sales reached an all-time high of 15% of total revenue.

Q4 Momentum: Digital sales remained strong at 13.5% of total revenue in the fourth quarter, up from 12.5% in the prior year.

Strategic Benefit: The company successfully launched POOL360 Unlocked in Q4, introducing new artificial intelligence features and expanded customer access.

9. Concluding Remarks

We believe Pool’s Q4 results validate that the company has successfully navigated the bottom of this cycle. With the discretionary business showing signs of firming up, a resilient maintenance segment, and the stock price trading at decade-low valuations, the long-term thesis remains firmly intact.