The recent addition to our portfolio, Pool Corporation (“POOL”), reported Q3’2022 results on 20 October 2022 beating expectations on both revenue and EPS.

Results

Actual Vs Consensus

Revenue $1.62B Vs consensus of $1.6B

Diluted EPS $4.78 Vs consensus $4.58

Key Financials

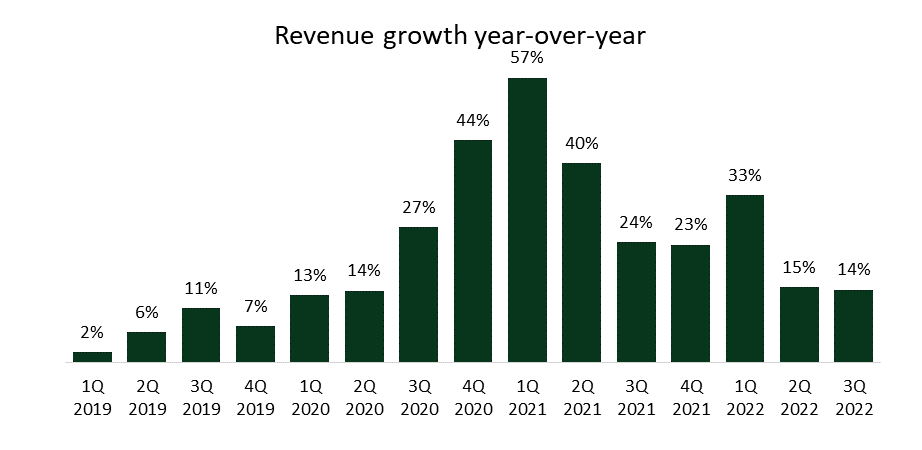

Revenue grew 14% year-over-year, with base business up 10% (base business excludes sales centers that are acquired, closed or opened in new markets for a period of 15 months). Inflation driven growth was in the range of 9-10%.

Operating expenses grew more than revenue at 17% due to recent acquisitions and new locations. Base business expenses were up 8% demonstrating operating leverage gains.

Operating income was $264 million, up 11% and operating margin was 16.3% compared to 16.8% last year. Acquisitions added $20 million in expenses during the third quarter compared to last year.

Adjusted Diluted EPS (excludes ASU 2016-09 tax benefit) of $4.76, up 7.2%.

Pool Business and Industry Outlook

“The industry has transformed as well and is now larger driven by, one, a higher installed base, which is approximately 6% larger when compared to the 2019 installed base of in-ground swimming pools; and two, structural inflation that has increased the size of the industry by approximately 30%.” Peter Arvan, CEO

However, management expects that new pool construction activity this year will be down 10%- 15% compared to 2021.

Source: Pool’s 10K filings, StockOpine analysis

Although new construction might be down as much as 15% in 2022, management still expects revenue growth of 17%-19% (5% from acquisitions), benefiting from structural inflation along with increasing installed base and strong demand for maintenance and repairs.

Volumes are also holding up, “And that's partially because the installed base is growing, partially because we believe that there was some pent-up demand in renovation, and it's offsetting a decline in new pool construction.” Peter Arvan, CEO.

EU sales which constituted 5% of total sales in 2021, face significant headwinds with sales down 24% (11% on constant currency). The strong prior year comparables along with weather, war and macroeconomic headwinds impacted EU results.

Outlook

Earnings per Share

Earnings guidance for FY22 remains within range of previous guidance (narrowed to $18.50 - $19.05 per diluted share). Excluding the ASU adjustment, the range is $18.26 to $18.81 per share, implying adjusted EPS growth for the year of 22%.

Revenue

Growth of 17%-19% is expected for 2022, implying a growth of approximately 12.5% in Q4’2022.

Source: StockOpine analysis, Koyfin

Growth rates are normalizing and move closer to management’s long term outlook of 6%-9%.

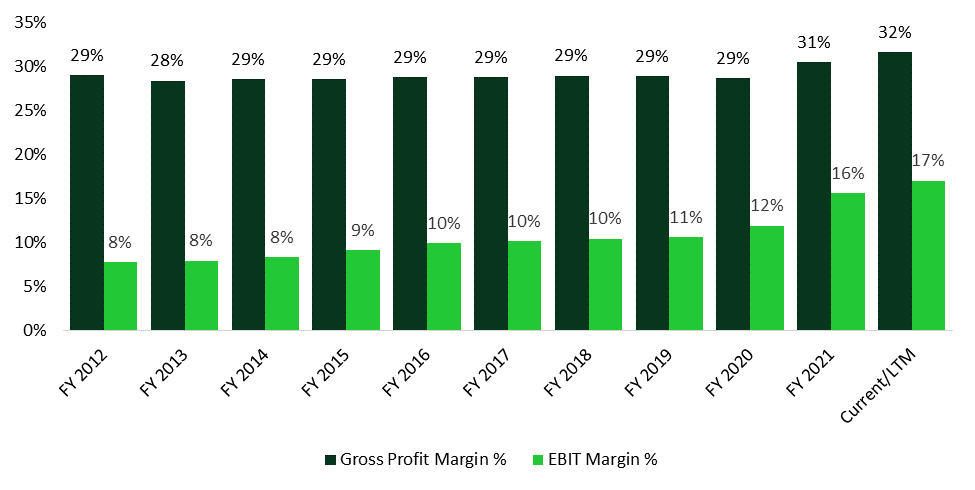

Gross Profit Margin

Management expects to close the year at a higher gross profit margin than in 2021, however, Q4’2022 gross profit margin is expected to decline by 150-200 basis points due to lower inflation from vendor price increases and lower incentives earned under volume-based vendor program.

Melanie Hart, CFO, reiterated the long term outlook of gross profit margin profile at 30%. Profitability margins is something to look for in 2023, as they can impact POOL valuation if they revert to pre-pandemic levels.

Source: StockOpine analysis, Koyfin

Inventory

“Our inventory balance at year-end could range from plus 10% to plus 25%, depending on the timing of vendor early-buy shipments. This is slightly ahead of the plus 5% we were expecting earlier in the year before we had the opportunity to evaluate the early buys.” Melanie Hart, CFO.

Management might be taking advantage of early buys, although, increasing inventory in the current macro environment might be increasing the risk of future profitability deterioration (write-offs/discounts).

Concluding Remarks

The inflationary environment and tighten monetary policy is affecting new pool construction and could also impact remodeling activity (currently remodeling demand remains strong). However, the increased installed base, the non-discretionary maintenance (60% of the business) and the increase in inflation would most likely partially offset the impact of those headwinds.

No matter the economic environment we expect that $POOL will take advantage of its scale and will continue gaining market share over the long term.

If you are interested to learn more about the Company you can always read our latest write up on Pool Corporation.

You can also find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.