POOL Corporation (“POOL”) released its Q4 and full year fiscal 2022 results on February 16th, reporting a miss on consensus revenue estimates and on its own guidance. Despite this, the company achieved a revenue growth of 16.7% for the year, falling slightly short of its guidance of 17%-19%. However, POOL's diluted EPS for the year came in at $18.7 per share, up 17.1%, which met the mid-range of the company's own guidance of $18.50 - $19.05.

This alone does not change the long-term thesis for POOL. It is clear that the Company was over-earning during the period 2020-2022, due to inflation price increases, low interest rate environment and increased spending on outdoor living as a result of the COVID-19 pandemic.

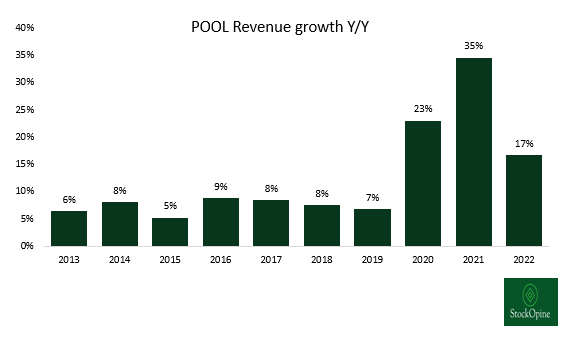

For context, since 2019, POOL increased its revenue by 1.9x. Going forward, we expect that management can still achieve its long-term revenue growth target of 6%-9%, driven by increasing installed base, a modest inflationary environment, new pool construction and organic growth.

Source: Koyfin, StockOpine analysis

An outstanding year for POOL

2022 was a remarkable year for POOL, reporting record revenue and profitability. Revenue for the year grew by 16.7%, reaching $6.2B, while the company achieved record levels of profitability margins.

Source: Koyfin, StockOpine analysis

“Revenue growth has expanded since 2019 by 93% driven by approximately 30% to 35% from inflation, 17% from acquisitions, 9% from new pool construction, 7% from the growth in the installed base of pools and 25% to 30% from market share and new product growth.” Melanie Hart, CFO

In previous write-ups on POOL, we expressed concern over the reversion of Gross Margin to historic average levels. While we don't expect gross margin to remain at the elevated level of 2022, we believe that improvement from pre-pandemic levels is achievable. Fortunately, Melanie Hart (CFO) provided reassurance on this point.

“Gross profit margin in 2023 is expected to be in line with our longer-term guidance of around 30% compared to the 31.3% gross margin we reported in 2022.” Melanie Hart, CFO.

30% is above the 29% pre-pandemic levels.

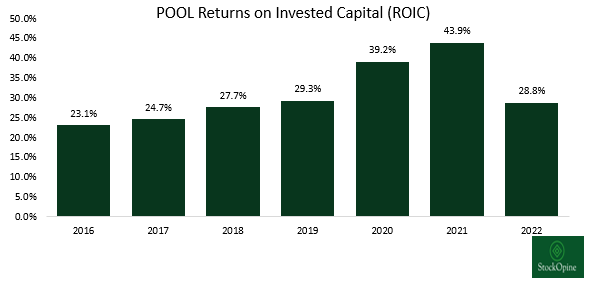

Furthermore, POOL continues to demonstrate high capital efficiency with returns on invested capital (as reported by management) reaching 28.8% for the year 2022. This indicates that the company is utilizing its capital effectively and generating significant value for its shareholders.

Source: Pool’s earnings presentations, StockOpine analysis

Pool Business and Industry Outlook

During the year, new pool construction declined by approximately 16% to 98,000 new pools, following the accelerated growth we observed in 2020 and 2021. For 2023, new pool construction is expected to fall back to the levels seen in 2018-2019, declining by approximately 15% to 20%.

Source: Pool’s 10K filings, Q4’2022 Earnings call, StockOpine analysis

Despite the decline in new pool construction, the installed base remains larger than it was in 2019 (estimated to be 6% larger as per Q3’2022 earnings call), and management anticipates a 4% year-over-year increase in the wholesale value per pool from the existing installed base based on inflation expectations.

New construction now accounts for 17% to 18% of POOL’s business, compared to 20% in 2021.

“We also saw a decrease in the portion of our business related to new pool construction, the more historical levels of 17% to 18%. And for remodel, we estimate this comprise 21% to 23% of our 2022 sales.” Melanie Hart, CFO