Q1’24 Peter Arvan CEO remarks:

“Overall, we saw permits down 15% to 20% for the quarter, which is more than we anticipated for the year. We believe that easier comps and signs of the bottom of the trough that we are seeing in some markets will allow the full year construction level to be more in line with our previously stated full year expectation of flat to down 10%.”

Two months later, the CEO’s remarks changed as follows:

“The most recent pool permit data suggests persistently weak demand for new pool construction, and with the peak selling season almost complete, we now believe that new pool construction activity could be down 15% to 20% for the year with remodel activity down as much as 15%.”

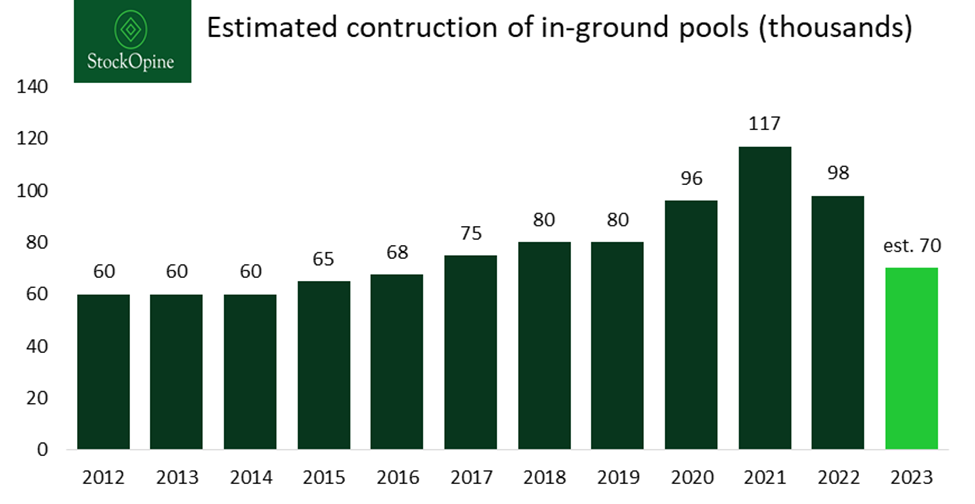

In our previous article titled: Evaluating the Strengths and Challenges of POOL Corporation, released in November 2023, we shared the below chart. According to the latest filings, 2023 closed at the lower range of 70k to 75k new pools built, recording a decline of 28.6% in 2023. The revised estimate of another 17.5% mid-point drop suggests new pool units around 58k for 2024, which is lower than any year since 2012. This figure is comparable to 2011 levels of 57k but higher than the 2009 levels of 45k units. This is a cause for concern not only for investors but possibly for the overall trajectory of the economy in 2024.

Source: Pool’s 10K filings, Q3’2023 Earnings call, StockOpine Analysis

Consequently, management revised the 2024 net sales guidance from flat to slightly up to a drop of about 6.5%, in line with year-to-date performance. The only positive comment from the 8K pool season update released on June 24, 2024, was that non-discretionary maintenance and repair demand, accounting for 62% of 2023 net sales, remains solid, somehow protecting revenues from falling to the -10% levels seen in 2023. Meanwhile, the diluted EPS guidance for 2024 was revised from $13.19 - $14.19 to $11.04 - $11.44, representing a mid-point drop of approximately 18%, implying a wider drop in gross margin and operating margins, initially anticipated at ~30% and ~13%, respectively.

Source: Finchat.io → 15% discount for StockOpine readers | Gross margin in 2022 was 31.3%, but this is not clearly shown on the chart.

In this short update, we will share information about leading indicators to better assess Pool Corporation's ("POOL," "Company") management assessment for 2024 and update our valuation based on new information.

Is the price drop justified? Does it provide a compelling entry point? Let’s find out.

Contents:

Industry Update (leading indicators)

Valuation (DCF along with a sensitivity analysis)

Conclusion (final thoughts and portfolio changes)

1. Industry Update

Leading economic indicators

With maintenance and repairs expected to perform well we will examine the remaining 38% of POOL's business, which includes renovation, remodeling, upgrades, and new construction.

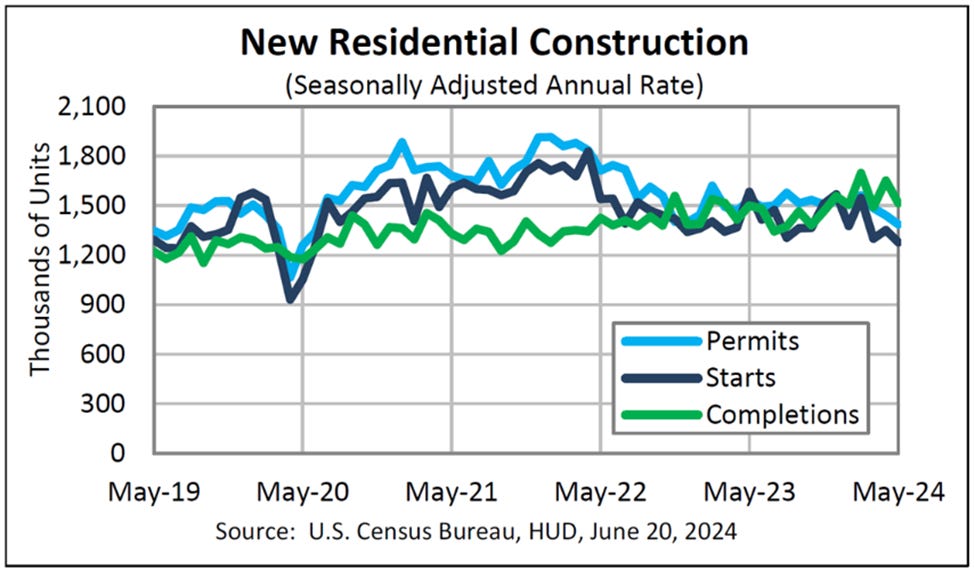

Looking at the permit activity for new residential construction, an indicator that can offer insights into new pool construction, we see a 3.8% decline to 1,386,000 for May 2024 compared to April 2024 and a 9.5% decline compared to May 2023. This justifies management’s assessment and also indicates that this is a wider economy impact rather than being specific to POOL. Examining housing starts, the chart shows that they are reaching the lowest level post-pandemic, and without signs of rate cuts, it’s difficult to project a significant inversion. Housing starts were estimated at 1,277,000, down by 5.5% compared to April 2024 and 19.3% below May 2023.

Source: New Residential Construction Press Release (census.gov)

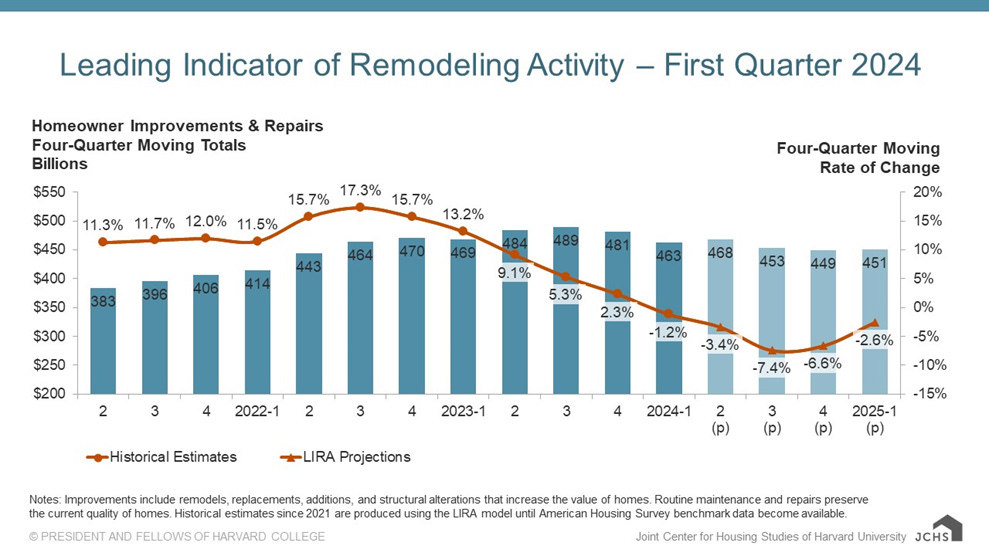

When examining the Leading Indicator of Remodeling Activity (“LIRA”), annual expenditure on improvements and repairs for owner-occupied homes is expected to decrease in 2024 and into Q1 2025, reaching a contraction of 7.4% by the third quarter of 2024 and easing by Q1 2025. Although there are no clear signs of recovery in the home improvement and repair industry, Abbe Will, Associate Director of the Remodeling Futures Program, expects the remodeling downturn to be short-lived. Considering that pool remodeling is more of a discretionary nature, it is reasonable to assume a higher decline (management expects a 15% drop) than the overall remodeling spend drop, which accounts for aging homes that need critical replacements. As such, we still get the sense that this is not a problem specific to POOL.

Source: Joint Center for Housing Studies of Harvard University, Note: The Leading Indicator of Remodeling Activity provides a short-term outlook of national home improvement and repair spending to owner-occupied homes.

Without further ado, let’s dive into the revised valuation.