Sunbelt Rentals: The Business Delivers, But the Numbers Tell a More Complicated Story

Record Cash Flow and the near-term headwinds

In the most recent quarter Q3 FY26, Sunbelt Rentals delivered a quarter that was broadly in line with management expectations. Rental revenue grew 2.6% year-over-year, free cash flow hit a record $1.4 billion year-to-date and the company successfully completed its primary listing on the NYSE (now officially trading on the NYSE under the ticker SUNB).

But if we look past the headline figures, the picture gets a bit more complex. Adjusted EBITDA margins contracted 259 basis points, EPS missed consensus by 7.1% and top line revenue was essentially flat at $2.64 billion which was a negligible $5.5 million miss against expectations.

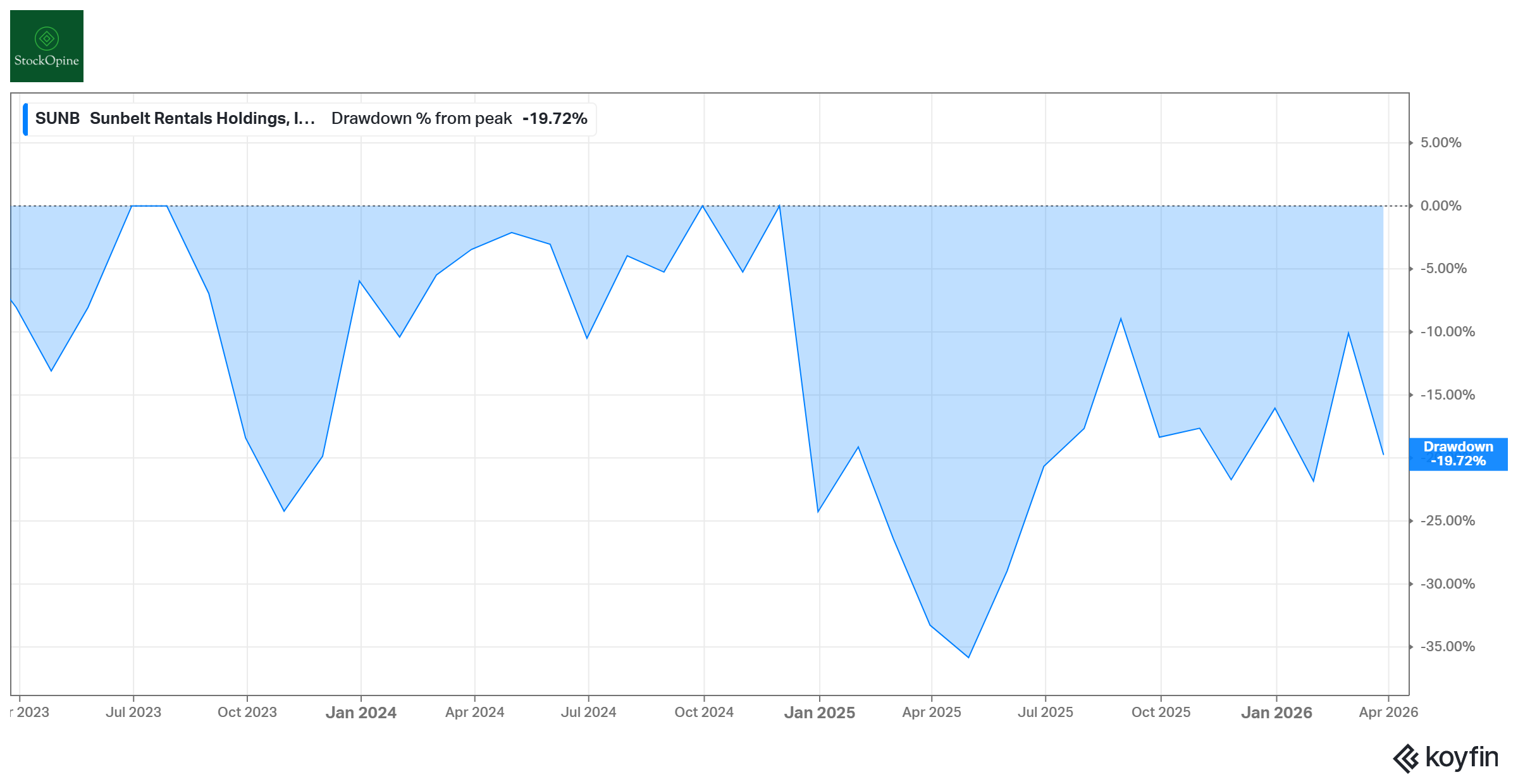

With the stock hovering about 21% below its peak, it’s worth asking: is the market missing the long-term story, or is this miss on expectations and margin pressure a sign to stay on the sidelines?

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

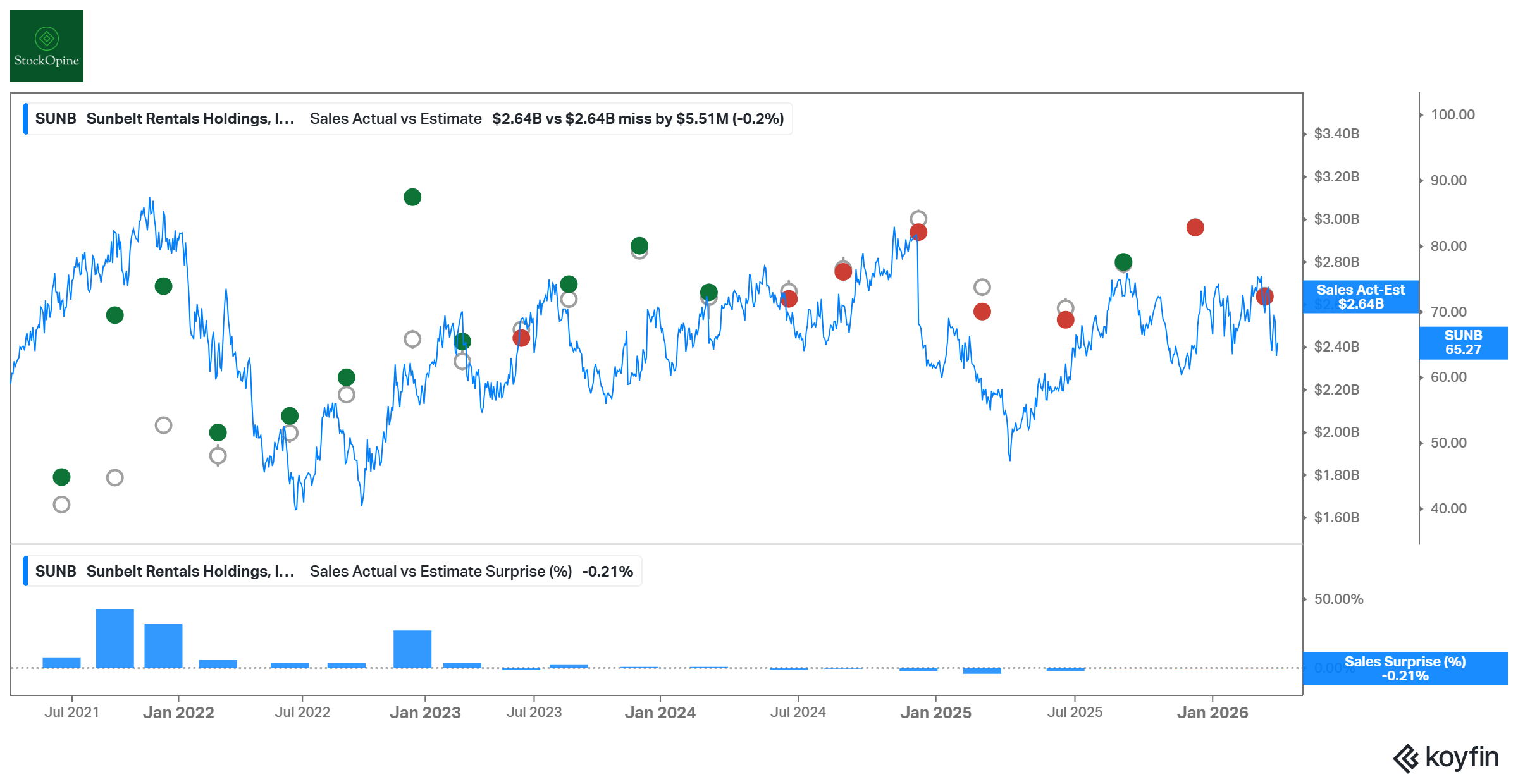

1. The Top-Line Trend: Persistent Small Misses

That $5.5 million revenue doesn’t mean much in isolation. However, it fits into a broader pattern we have been tracking. Sunbelt has missed revenue consensus in the majority of quarters over the past two years. While these negative surprises are small in magnitude, their frequency indicates a recurring struggle to capture the top-line growth anticipated by the market.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

2. Q3 FY26 - the Numbers

Overall, the results were solid on the top line but missed analyst consensus across every profitability metric:

Total Revenue: $2.64B (+2.7% YoY)

Rental Revenue: $2.44B (+2.6% YoY, or ~4% excluding hurricane impacts)

Adj. EBITDA: $1.08B (-3.1% YoY), with margin 41.0% (-259bps YoY)

Adj. EPS: $0.78 (-3.7% YoY, missing the $0.84 consensus)

YTD Free Cash Flow: $1.43B (+83% YoY)

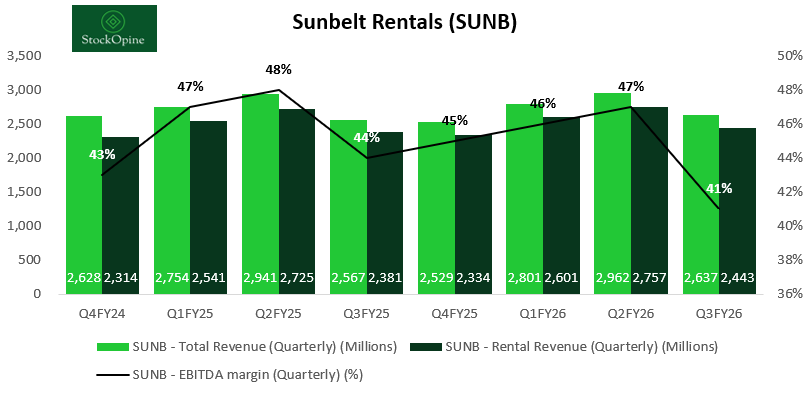

The Story of the Quarter: Margin Compression

The top line was resilient with rental revenue growth accelerating quarter-over-quarter (4% Vs 3% in Q2’26 excluding the prior year hurricane impact), but margin compression is the story of the quarter. Two distinct drivers are weighting on profitability right now:

Revenue mix: The Specialty segment is growing faster than General Tool. Specialty naturally carries a lower EBITDA margin, though it boasts higher return on investment because it is less capital-intensive. We’re also seeing a boom in ancillary revenues (like cable installation for major events such as the Super Bowl or step-up and step-down transformers re-rented to support data centre projects), which carry lower margins than pure rental revenue. These services are currently growing at twice the pace of pure rental revenue. These dilute the margin percentage due to higher labor and logistics costs, but as CEO Brendan Horgan emphasized, this is still “highly profitable revenue” that increases the total dollar pool of earnings.

Internal Costs: Elevated internal repair and fleet repositioning costs which have been a significant headwind throughout the year. The good news? CEO Brendan Horgan signaled a pivotal turning point in Q3, indicating that these pressures are finally starting to tail off.

Source: StockOpine Analysis, Company filings

Segment Performance

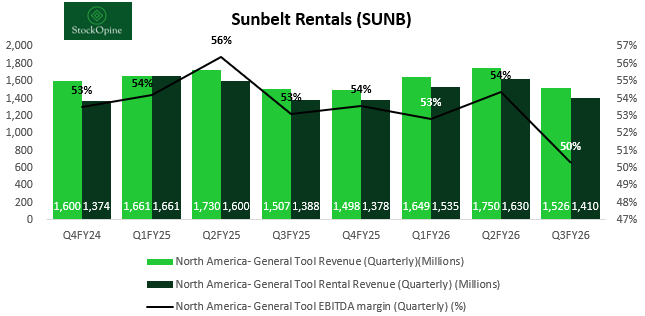

North America General Tool - Sunbelt’s largest segment reported total revenue of $1,526 million, growing 1.3% year-over-year, with rental revenue up 1.6% or approximately 2% excluding hurricane impacts. Growth was led by volume improvement, with strength in mega projects and large strategic accounts offsetting moderating conditions in the local non-residential construction market. However, adjusted EBITDA margin contracted sharply by 282 basis points to 50.3%, primarily reflecting the mix effects of higher ancillary revenues and fleet repositioning costs discussed above.

Source: StockOpine Analysis, Company filings

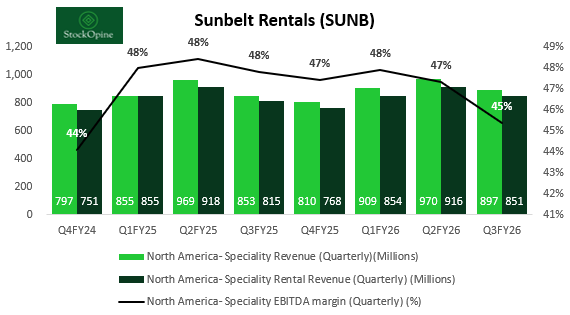

North America Specialty – The star of the quarter. Total revenue hit $897 million, up 5.2% year-over-year. Rental revenue grew 4.4% or approximately 7% excluding hurricane impacts. Demand was driven by broad-based momentum across flooring, temporary fencing, structures and walls, trench safety and power and HVAC. Adjusted EBITDA margin contracted 246 basis points to 45.4%, consistent with the group-wide cost pressures.

Source: StockOpine Analysis, Company filings

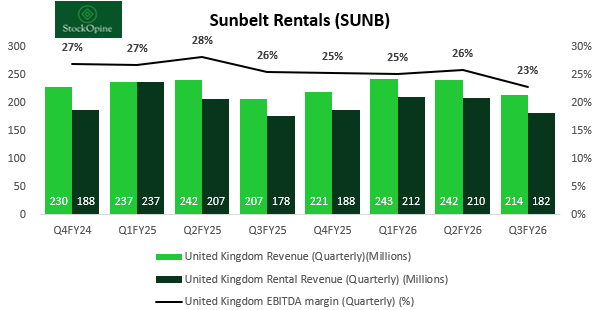

UK- The United Kingdom segment continues to be the weakest in the group. Total revenue of $214 million grew 3.4% as reported, but declined 2% at constant exchange rates. This means that growth is entirely a function of currency movement rather than operational progress. Rental revenue grew 2.2% as reported and adjusted EBITDA margin fell 271 basis points to 22.9%. Management is undertaking restructuring actions to improve profitability and return on investment over the medium term.

Source: StockOpine analysis, Company filings

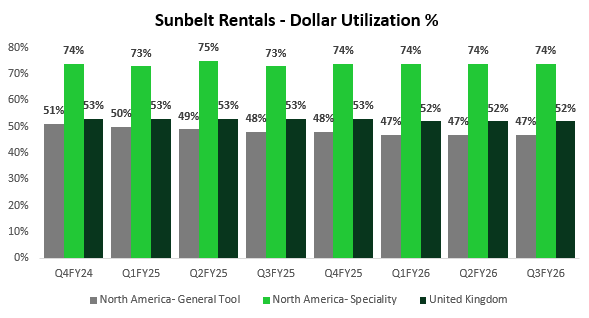

Dollar Utilisation

North America General Tool: Dollar utilisation has declined slightly from 48% in Q3 FY25 to 47% in Q3 FY26. While rental revenue grew by 1.6%, this was offset by a larger 3.1% increase in average OEC (original equipment cost), as well as the impact of the internal repair costs and company repositioning of its fleet to maximize utilization in a mixed construction market.

North America Specialty: Specialty achieved an increase in dollar utilization to 74%, driven by a 4.4% increase in rental revenue that outpaced a 2.8% increase in average OEC.

UK: The slight decline in dollar utilization from 53% in Q3FY25 to 52% in Q3FY26 coincides with a period of operational restructuring in the UK.

Source: StockOpine analysis, Company filings

Capital Allocation & Free Cash Flow

Year-to-date free cash flow reached $1.43 billion (up 83%) from $782 million in the same period last year. This dramatic improvement reflects management’s disciplined capital allocation approach, with year-to-date capex falling 29% to $1.72 billion.

“When markets are experiencing the transitory headwinds, we have experienced over the last few quarters, we remain extremely disciplined in our deployment of capital to support strong utilization and rate discipline. When markets are growing more rapidly, we accelerate capital spending to capture opportunities in market share. In all cases, we generate significant free cash flow in excess of our investments, which we return to shareholders in the form of dividends, debt repayment, and share buybacks.” Alex Pease, CFO

And, they are using free cash flow aggressively to reduce leverage and return cash to shareholders:

$1.35 billion returned to shareholders year-to-date through $1.05 billion of share buybacks and $307 million in dividend payments. Shares outstanding have declined from ~443M in early 2022 to 415M currently.

A new share buyback program of up to $1.5 billion just launched alongside the NYSE listing, signaling management’s confidence at current price levels.

Lowered net borrowings by over $200 million in last year to $7.6 billion. As of January 2026, net debt to adjusted EBITDA leverage is 1.6x, down from 1.7x a year earlier and within the 1.0x–2.0x target.

Now let's turn to the forward-looking metrics. Read on for a breakdown of Sunbelt's updated guidance, our thoughts on valuation, and exactly how we are handling our position.