Today we are breaking down Grab’s game-changing announcement: the $600 million cash acquisition of foodpanda Taiwan. This transaction proves that Grab’s “Super App” playbook has legs beyond the Southeast Asia.

1. Breaking the SEA Border: Why Taiwan?

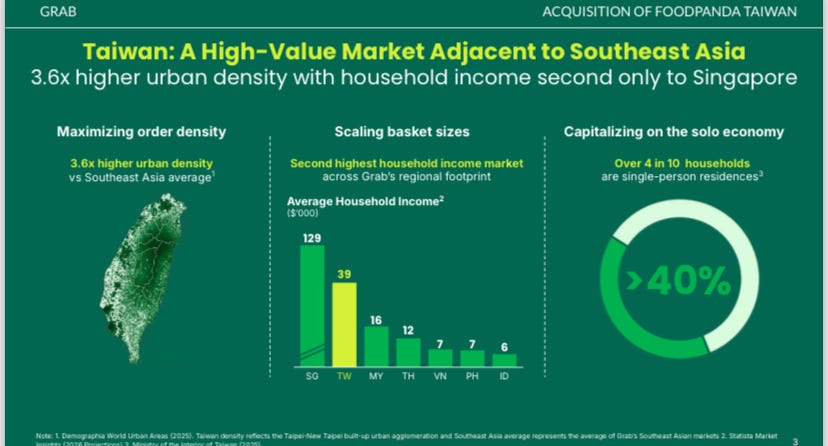

For the first time in its history, Grab is stepping outside Southeast Asia into its 9th market. CEO Anthony Tan described this as a natural next step, and the data supports this move as Taiwan it’s a logistics dream given its population density.

Taiwan’s urban density is 3.6x higher than Grab’s Southeast Asian average. High density means shorter delivery routes (so better efficiency) and higher “drops-per-hour,” meaning that margins are generally higher.

Additionally over 4 in 10 households are single-person residences. These households don’t usually cook, making them the highest-frequency users of delivery apps. What a gift for Grab!!

But they are not just solo. They have money to spend, as Taiwan has the second highest household income in Grab’s footprint, trailing only Singapore.

Source: Grab M&A presentation

As Grab’s CEO, Anthony Tan, puts it:

“Taiwan’s population of approximately 23 million also has a high demand for mobile-first services, similar to the Southeast Asian consumers who Grab serves every day.”

2. The Valuation: Did Grab Get a “Steal”?

Grab is paying $600 million for a business that generated $1.8 billion in GMV in 2025. This implies a 0.33x EV/GMV multiple, that stands at a 51% discount to its own trading multiple of approximately 0.68x GMV (including mobility GMV).

To add on this, Uber was willing to pay $950 million for the same asset just 22 months ago before regulators blocked it. However you slice it, Grab has done a good deal.

3. Uber - The Elephant in the Room

The main ‘concern’ relates to the relationship with Uber which remains a major strategic partner and a shareholder in Grab (a remnant of the 2018 SEA exit). Grab will now go head-to-head with Uber Eats in Taiwan creating a potential conflict. When asked about this, Anthony Tan gave the response needed from someone focused on shareholder value:

“Our primary fiduciary duty is to all our shareholders, and driving long-term value creation for our ecosystem in all the countries that we serve.”

Grab is here to win for their investors. Addressing concerns over regulatory hurdles, management clarified that they are entering Taiwan as a new competitor rather than a market consolidator like Uber. This distinction provides a significantly smoother path with the Taiwan Fair Trade Commission.

4. Financial Impact

Grab is buying a business that is already profitable on an adjusted EBITDA basis (before group cost allocations). As such they expect the following:

The deal to be accretive to Grab’s 2026 Revenue guidance of $4.04B - $4.10B.

The transaction to contribute at least $60 million in incremental Adjusted EBITDA by 2028. That stands at 3.3% of current GMV; above Grab’s average of 2% in FY25 and slightly below its long-term target of 4%. Effectively, it’s buying a profitable asset with room for growth.

5. Final Thoughts

This deal is a masterclass in capital allocation. For the past year, the market has been obsessed with rumors of a Grab-GoTo merger, a deal that many expected to be significantly more expensive (at ~$7b) and complex.

Instead of chasing this multi-billion dollar merger in a lower-income market like Indonesia, Grab pivoted to a cleaner, higher quality asset by grabbing the #1 player in a high-density market at just 0.33x EV/GMV multiple.