Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analysed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

At the end of each write-up, we will state whether we decided to buy the stock or not. If not, keep an eye to our Quarterly Portfolio Update releases in which we will update you for all the transactions that took place during the latest quarter.

After covering the equipment rental industry through our write-up on Ashtead Group, we are fascinated with the durability of this business and the potential for industry consolidation. Therefore, for our final research report of 2022, we decided to examine United Rentals (Ticker: $URI), the leading equipment rental company in North America and compare and contrast the market leaders to gain a broader understanding of the industry as a whole.

It is important to note that Ashtead and United Rentals have different fiscal years, with Ashtead's fiscal year ending in April and United Rentals' fiscal year ending in December, therefore, the comparison will not be 100% apples-to-apples.

Ashtead Group Write up – Renting is Flexible and Affordable

1. Key Facts

Description: United Rentals (“URI”, “Company”) is the largest equipment rental company in the world with an estimated market share of 16%. The Company operates a network of more than 1,400 locations across the United States, Canada, as well as locations in Europe, Australia, and New Zealand.

Key Financials: Over the period 2012 to Q3’2022, the Company depicted a Revenue Compound Annual Growth Rate (“CAGR”) of 10.7% reaching a Trailing Twelve Month (“TTM”) revenue of c. $11.1 billion. URI has a balance sheet with Cash and Short-term investments of $76 million compared to a debt and lease liabilities amounting to $10.5 billion.

Price & Market Cap (as of 28th December 2022): Its market cap is $24.5 billion with a 52-week high of $374 and a 52-week low of $231, whereas it currently trades at $352.

Valuation: URI trades at a TTM EV/EBITDA of 6.8 (10 Year average of 6.6) and at a TTM P/E of 13.1 (10 Year average of 14.6).

2. The rise of United Rentals

United Rentals was founded in 1997 by Bradley Jacobs and was listed in the New York Stock Exchange in the same year. The Company was formed to consolidate the equipment rental industry through an acquisition strategy.

In 1998, it became the largest equipment rental company in the US through the acquisition of U.S. Rentals, Inc. for $1.3 billion.

The equipment rental industry is highly fragmented, and was a good candidate for consolidation according to Bradley Jacobs, who followed a similar strategy in garbage-collection industry with United Waste Systems, Inc. in the nineties. United Waste Systems, Inc. was created by Jacobs in 1989, went public in 1992 and was sold to Waste Management Inc for $2.5 billion in 1997.

Jacobs served as CEO of United Rentals until 2003, when he stepped down to pursue a new venture. He continued as chairman of the board until 2007.

Since its IPO (price data available on Yahoo Finance), United Rentals has generated a compound average annual shareholders' return of around 14%. In the years following its formation, the company focused on expanding its operations through acquisitions of other equipment rental and specialty rental companies. More details on the Capital Allocation section.

3. Business overview

Equipment Rentals

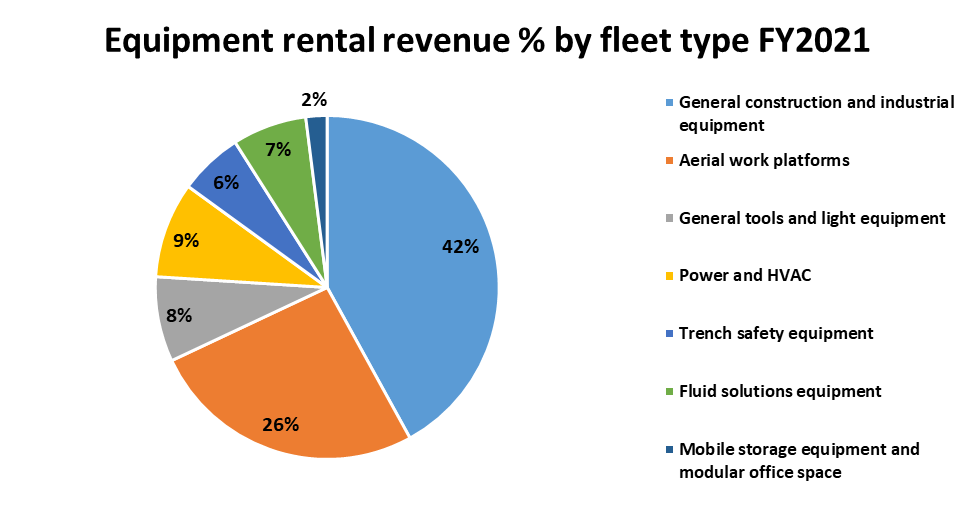

United Rentals is offering equipment on an hourly, daily, weekly and monthly basis. The Company’s equipment include general construction and industrial equipment; aerial work platforms; general tools and light equipment and specialty equipment such as trench safety equipment; power and HVAC equipment; fluid solutions equipment; mobile storage equipment and modular office space.

Source: United Rentals Annual Report 2021, StockOpine Analysis

United Rentals owns the largest rental fleet in the world with a cost (Original Equipment Cost or “OEC”) of approximately $17.4 billion as of 30 September 2022 compared to Ashtead Group’s OEC of $14.5 billion as of 31 October 2022.

Equipment rentals make 87% of URI’s total revenue for the trailing twelve months ended 30 September 2022. Other sources of revenue include sales of rental equipment, sales of new equipment, contractor supplies sales and service and other revenues. We think of those revenue streams as by-products of the rental equipment revenue.

General and Specialty segments

The Company operates through two segments, General Rentals and Specialty. The General segment includes the rental of construction, aerial and industrial equipment, general tools and light equipment whereas the Specialty segment includes Trench Safety, Power & HVAC, Fluid Solutions, Tool Solutions, Onsite services and Portable storage and Modular Space.

Source: United Rentals Third-Quarter-2022-Investor-Presentation

The General Rentals segment operates across the United States and Canada whereas the Specialty segment primarily operates in the United States and Canada, with presence in Europe, Australia, and New Zealand.

Specialty is growing faster than General Rentals and accounted for approximately 26% of equipment rental revenue for FY 2021 compared to 16% in FY 2016.

Comparing the above to Ashtead, we note that the Specialty segment of Ashtead also grows at a faster rate than its General segment representing 30% of rental revenues for the year ended 30 April 2022. For the last five fiscal years Ashtead grew Specialty revenue at a CAGR of 30% generating c.$2B in FY 2022 while URI grew Specialty rental revenue at 22% CAGR generating $2.1B for fiscal year 2021. We should note that the above growth rates include the impact of acquisitions and relate to fiscal years ending at different dates.

Concluding on the above, Specialty is the most lucrative segment for both entities as it grows at a faster rate, has lower rental penetration and can be accretive to profitability margins. According to URI’s segmental reporting, Specialty had a gross profit margin of 46.8% for FY 2021 compared to 37.4% of the General Rentals segment.

Markets

In terms of geographic mix, 90% of URI’s FY21 revenue ($8.8 billion) was from the US. United Rentals is also the market leader in Canada with an estimated market share of 18% based on Ashtead’s strategic report for the FY22.

Until 2018 URI was operating only in Canada and US though it entered the EU market with the acquisition of BakerCorp (provider of tank, pump, filtration and trench shoring rental solutions) in July 2018and Australia and New Zealand in 2021 through the acquisition of General Finance (provider of mobile storage and modular office space).

As of 30 September 2022, URI operated through a network 1,402 locations (1,198 in US, 145 in Canada, 13 in EU and 46 in Australia and New Zealand). This compares to Ashtead’s 1,307 locations as of October 2022 (1,025 in US, 98 in Canada and 184 in UK).

Customers

The company serves a diverse customer base, including construction companies, industrial companies, utilities, municipalities, and homeowners. In 2021, the Company's top ten customers accounted for only 4% of total revenue.

As part of its strategy, United Rentals has made national accounts a priority. These are generally defined as customers with potential annual equipment rental spend of at least $500,000. In 2021, national accounts contributed 43% of the Company's revenue. To cultivate these relationships, United Rentals provides these clients with a single point of contact to handle all their equipment needs.

United Rentals serves primarily three end markets, a) Industrial and other non-construction rentals, c. 50% of rental revenue, b) Commercial construction rentals, c. 46% of rental revenue and c) Residential construction rentals, c. 4% of rental revenue.

4. Culture and Compensation

Key Management

Both URI’s and Ashtead’s CEOs, namely Matthew J. Flannery and Brendan Horgan, respectively, were appointed in May 2019, while both joined their companies before 2000, demonstrating a ‘grow within’ culture.

Evaluating the executive management of URI we noted two changes in Named Executive Officers (“NEOs”) in 2022 compared to what it was reported in the latest proxy statement but nothing seems absurd.

CFO change -> Jessica T. Graziano joined United States Steel Corporation (a smaller company in terms of Market Cap but larger in terms of revenues) and was replaced by William ‘Ted’ Grace in Nov 2022, who has been with the company since 2016 and served as VP of Investor Relations. Nothing appears shady here as per her LinkedIn profile she does change jobs every few years. Additionally, the compensation package offered by United Steel (estimated at $3.8M per annum plus c. $7M in new hire, one-time awards vesting at various time intervals) seems attractive compared to her $4M total compensation in 2021 ($2.1M in 2020).

Jeffrey J. Fenton was Senior VP of Business Development and retired on June 30 of 2022 and was succeeded by Alfredo Barquin (VP of Business Development, joined in Jan 2022 but not yet a NEO) to lead the M&A growth strategy.

The remaining two NEOs joined in 1998 and in 2003 further justifying the ‘grow within’ culture.

Compensation

Total compensation of Matthew J. Flannery grew from $6.5M in 2020 to $12.7M in 2021 driven mainly by higher stock awards ($9.1M Vs $4.9M). Per Simply Wall St, CEO’s payroll is about average for similar size companies in the US ($12.85M).

The compensation of URI’s NEOs has 3 components a) Base Salary (cash and fixed), b) Annual Incentive Compensation Plan “AICP” (cash and vested shares of Company stock) and c) Long-Term Incentive Plan “LTIP” (equity).

AICP is based on financial metrics, being 50% Adjusted EBITDA and 50% EPI (Economic Profit Improvement, spread of Return on Invested Capital “ROIC” over a constant 10% WACC) and other qualitative strategic factors (human capital, customer experience, digital technology, ESG). LTIP performance restricted units (“PRSUs) are based on 50% Revenue and 50% ROIC and time RSUs are based on continuous employment (vest over 3 years). Both AICP and LTIP plans show that URI is focused on profitable growth, yet value adding growth as ROIC should reach desired levels.

Ashtead has the following compensation components for its key management: a) base salary and benefits, b) Deferred Bonus Plan (“DBP”) based on achievement of annual performance targets relating to adjusted pre-tax profit and free cash flow -> 2/3 received and 1/3 is deferred to a new share award of share equivalents, c) LTIP for which performance is measured over a 3-year horizon and takes into account Total Shareholder Return (40%) relative to FTSE 100, Earnings per share annual growth (25%), Return on Investment (25%) and Leverage – Net Debt to EBITDA (10%) and d) Strategic Plan Award that relates to the Sunbelt 3.0 and includes among others increase in EBITDA and improvement in ‘cap factor’ (rental revenue / average original equipment cost) in North America.

Both compensation packages seem attractive and comprehensive and contain among others stock ownership guidelines, aligning management with shareholders. None of the two stands out but we have a slight preference for Ashtead’s one given that it also covers free cash flow.

The below provides a quick head to head comparison of URI and Ashtead CEOs compensation. Total compensation of URI’s CEO was way higher than Ashtead, as URI’s 2021 compensation was affected by the 200% achievement of their compensation targets. In prior fiscal year they had similar compensation.

Source: Proxy statements, Annual filings, StockOpine analysis

Culture

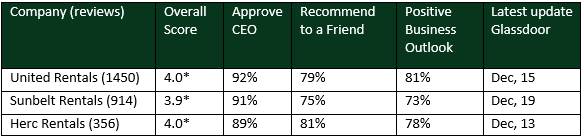

Using Glassdoor score which can be used as a proxy for culture it can be concluded that no single company stands out to its peers. URI has completed the largest acquisitions in the industry thus having similar scores with its peers shows that cultural integration risk is minimized. In addition, URI employee turnover ratio was 15.4% in 2021 (11.9% in 2020) which is well below Ashtead’s turnover ratios of 22% in North America in FY22 (18% in FY21) and 25% in UK (17% in FY21) with the majority being people with less than 2 years’ experience (as expected). Ashtead’s abnormally high voluntary turnover ratio reported for Canada of 28% (21% in FY21) is a bit strange given its expansion plans in the region. This does not seem to be a health & safety issue as incident rates improved across all regions.

Source: Glassdoor, StockOpine analysis

Based on the above findings it appears that URI’s culture is better despite the ongoing acquisitions and this is further justified by its awards of Forbes America’s Best Employers (Rank 40 of 500 Large employers) and Rank 37 in 2022 Top Workplaces USA by Energage.

5. Equipment Rental Industry

This section is brief so as to avoid repeating what was stated in section 4 of our Ashtead write-up. For additional information you can refer to that write-up.

Industry’s key driver is construction activity (say 50%) yet other sectors are also important (manufacturing, entertainment, downstream, power / utilities etc.).

Key benefits to customers are capital conservation, right equipment for the right job, outsourced maintenance, storage savings, access to advance equipment etc.

Industry is fragmented (local, state, regional, global players) yet consolidating with Ashtead (12%) and URI (16%) accounting for 28% of US market in 2022 compared to 9% in 2010.

Source: Ashtead Group First Quarter Results FY23 presentation

URI is also the largest player in Canada with 18% share compared to 8% of Ashtead, whereas Ashtead dominates the UK market (10%) in which URI has insignificant presence (just 2 specialty locations).

Market size and forecasts

As per American Rental Association (“ARA”), US market, which accounts for >90% of URI sales, is estimated to reach $55.9B in 2022 (11.2% growth) and exceed $65.1B by 2026 (CAGR of 3.9% for 2022-2026).

As per ARA, Canada market is estimated to reach $4.7B in 2022 (14.4% growth) and exceed $5.4B by 2026 (CAGR of 3.5% for 2022-2026).

6. Financial Analysis

Over the period from 2012 to Q3 2022, United Rentals achieved a revenue CAGR of 10.7%. During this time, profits and free cash flow grew at a faster rate, reaching an operating margin of 27% and a free cash flow margin of 13%. In the trailing twelve months ending in Q3 2022, revenue reached $11.1 billion, while operating income and free cash flow reached $2.95 billion and $1.4 billion, respectively.

Source: United Rentals Annual Reports, Koyfin, StockOpine Analysis

Revenue growth was driven by rental rate increases, which were mainly due to increases in OEC, increase in fleet productivity, acquisitions, and branch openings. The Company's growing revenues and market share over the years required significant amounts of CAPEX and funds spent on acquisitions. In the last ten fiscal years, United Rentals spent $11.0 billion in net rental CAPEX and $9.1 billion in business combinations, with those investments ramping up in fiscal 2022 in anticipation for higher demand.

The recent drop in free cash flow margin in 2021 and 2022 compared to 2020 can be attributed to increased CAPEX in order to fund future growth opportunities and due to pausing of investments in fleet equipment for 2020 as a response to COVID-19. Adjusting for cash acquisitions would result to an average FCF for the period of 1%.

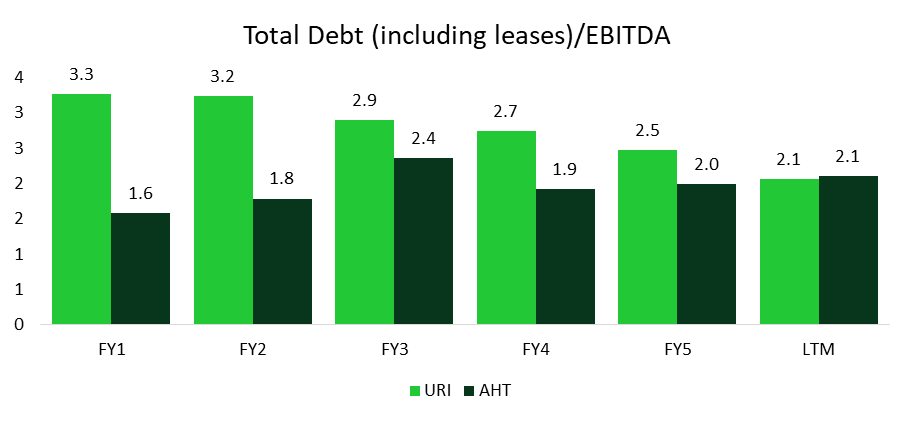

United Rentals' net debt is $10.5 billion, representing around 43% of its market capitalization and around 165% of the book value of its total equity. The resulting ratio of total debt (including leases) to EBITDA is 2.1x, while its leverage ratio as measured by management (net debt divided by LTM adjusted EBITDA) is 1.9x, the lowest level in the last 10 years.

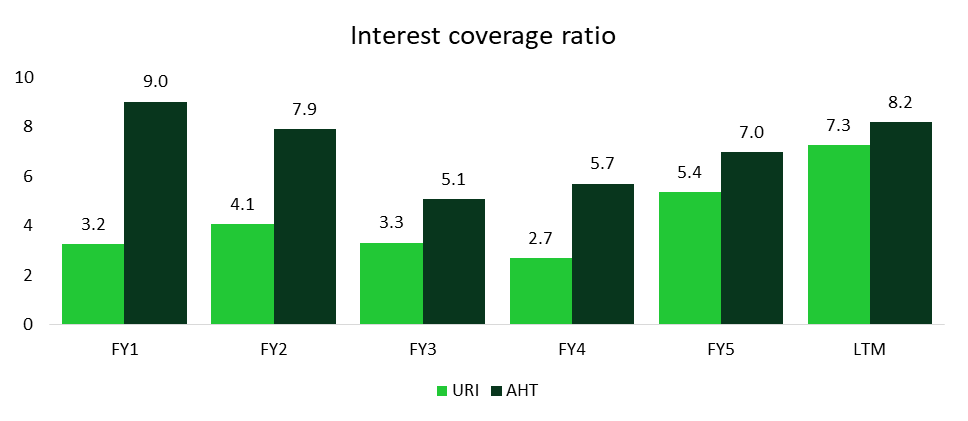

Operating profits sufficiently cover interest expenses, with a TTM interest coverage of 7.3x (the average interest coverage over FY17-FY21 was 3.7x) indicating low default risk.

United Rentals Vs Ashtead Group Head-to-head analysis

In this section we will compare United Rentals to Ashtead Group through financial metrics over a span of a five year period. Since we have different fiscal years, FY5 represents fiscal year ending 31 December 2021 for United Rentals and fiscal year ending 30 April 2022 for Ashtead.

Profitability

Source: United Rentals Annual reports, Ashtead Group Annual reports, Koyfin, StockOpine Analysis

Ashtead's profitability appears to be slightly better, although the differences are marginal, indicating that there are no clear cost advantages. It is possible that Ashtead’s better EBITDA margins in FY1-FY5 is due to higher sales mix in Specialty which was approximately 30% of rental revenue in FY 2022 (23% in fiscal year 2019) compared to United Rentals' Specialty mix of 26% of rental revenue in FY2021 (20% of rental revenue in FY 2018).

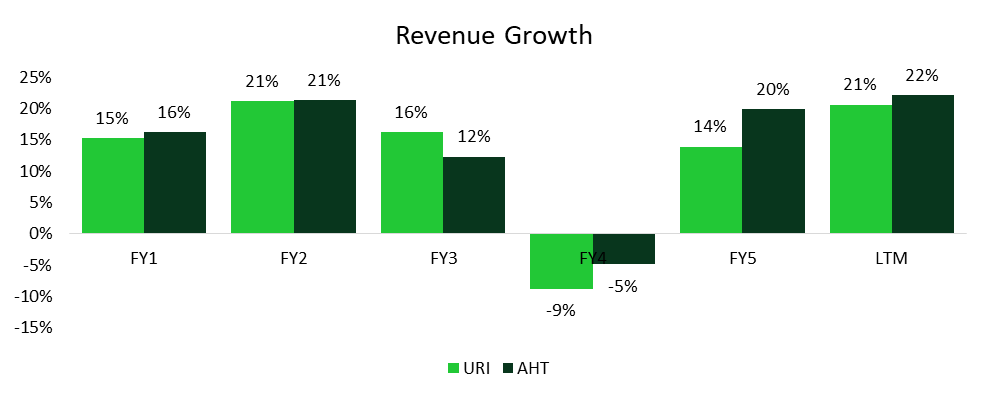

Revenue growth

Source: Koyfin

Both companies depict similar growth rates and we expect this trend to continue.

Investments in CAPEX and Acquisitions

Source: United Rentals Annual reports, Ashtead Group Investor Presentations, StockOpine Analysis

URI’s seems to be spending more compared to Ashtead due to its acquisition strategy, however, this does not translate into a faster revenue growth compared to Ashtead, and thus Ashtead appears more efficient.

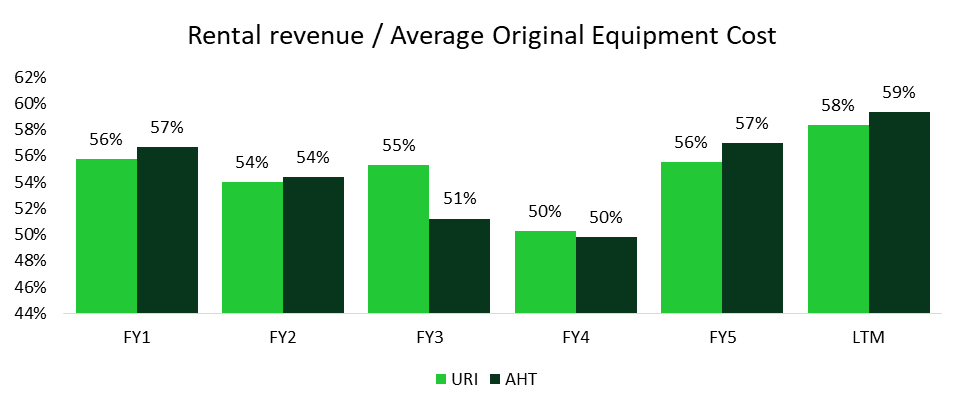

Rental Equipment yield

Source: United Rentals Annual reports, Ashtead Group Quarterly Press releases, StockOpine Analysis

Neither company demonstrates materially better utilization of its fleet.

Liquidity

Source: United Rentals Annual reports, Ashtead Group Annual reports, Koyfin, StockOpine Analysis

Both companies follow a disciplined capital strategy keeping their leverage at sustainable levels. URI managed to partly repay its debt following the peak levels achieved in 2018 (FY2) while Ashtead embeds Net Debt to EBITDA ratio in its executive compensation structure keeping management debt conscious. For comparison, ratios of Herc Holdings (the 3rd largest player in US) exceed 5x.

Source: United Rentals Annual 10K and 10Q Filings, Ashtead Group Annual reports and press releases, StockOpine Analysis, Note: Ratios slightly differ from our previous write-up as we decided to recalculate these ratios rather than use Koyfin figures directly.

While Ashtead depicted a better interest coverage ratio, URI managed to improve its ratio in recent years due to improvement in operating income. Both are expected to be affected by the rising interest rate environment, yet we believe that they can sustain such pressures as only 36% of URIs indebtedness bears interest at variable rates (per Q3’22) and 41% of Ashtead (latest annual report) minimizing the risk of breaching covenants.

Outlook

During Q3 2022, United Rentals increased its guidance for the fiscal year 2022 and now expects revenue in the range of $11.5-$11.7 billion, representing full year revenue growth of 19%. This growth is primarily driven by increases in average OEC, as well as increases in rental rates and fleet productivity (a function of rental rates and time on rent). Adjusted EBITDA for the year is expected in the range of $5.5-$5.6 billion, implying an Adjusted EBITDA margin of 47.8% based on the midpoint of the guidance, suggesting further improvement in profitability compared to last year's Adjusted EBITDA margin of 45.4%.

Gross Rental Capex (excluding sale proceeds from rental equipment) for FY 2022 is expected to be in the range of $3.25-$3.45 billion, representing 28.9% of total estimated revenue, compared to 30.9% in fiscal 2021. These factors are expected to result in free cash flow in the range of $1.6-$1.8 billion, implying a FCF margin of 14.7%, compared to 15.6% in the previous fiscal year.

Comparing United Rentals to Ashtead, Ashtead increased its guidance as well and now expects to grow Group rental revenue in the range of 18% to 21% for the year ending 30 April 2023. Ashtead expects gross rental CAPEX in the range of $2.7B-3B, representing 29.9% of total estimated revenue based on analysts’ expectation, compared to 22% spent FY 2022. The estimated free cash flow is expected to be approximately $300M.

7. Capital Allocation

URI’s growth is driven both organically and through acquisitions whereas excess cash are returned to shareholders in the form of share buybacks. Since 2012, URI returned approximately $5.3 billion to shareholders through share repurchases whereas the number of Ordinary shares is down by 25.5% since then, with Diluted Earnings per Share from continuing operations growing from $0.79 in 2012 to $20.56 as of today.

Source: Koyfin, StockOpine analysis

Organic growth is driven by average CAPEX investments of c. 20% of sales for 2012 until today (well below the 33% of Ashtead) and through acquisitions. As noted in our Ashtead write-up, URI is more actively engaged in acquisitions (c. 300 acquisitions), accounting for an average 22.5% of sales for its latest 5 fiscal years (excl. 2020) compared to Ashtead’s ratio of 11.9%. This is also justified by the higher goodwill percentage of total assets of 26% for URI compared to 15% for Ashtead.

The most notable transactions since 2012 are the following:

2012: Acquisition of RSC Holdings for $4.2 billion (Equipment Rentals). Largest merger in the industry where the rental industry’s largest company acquired RSC, the industry’s second-largest firm.

2014: Acquisition of National Pump for $780 million (Specialty)

2017: Acquisition of NES Rentals for $965 million (Equipment Rentals) – Purchase EBITDA multiple of 4.9x

2017: Acquisition of Neff Corporation for $1.3 billion (Equipment Rentals) – Purchase EBITDA multiple of 5.4x

2018: Acquisition of BakerCorp International Holdings, Inc. for $715 million (Specialty) -> to provide a full suite of fluid transfer, storage and treatment solutions, leading position in Pumps and entry point into Europe - Purchase EBITDA multiple of 9.0x

2018: Acquisition of BlueLine for $2.1 billion (Equipment Rentals) – Purchase EBITDA multiple of 6.7x

2021: Acquisition of General Finance for $1 billion (Specialty) –> Expanding portfolio to the commercial mobile storage and modular space market of c. $5B and entrance to Australia and New Zealand - Purchase EBITDA multiple of 10.6x

2022: Acquisition of Ahern Rentals for $2 billion (Equipment Rentals), the 8th largest equipment rental company in North America providing opportunity for cross-selling URIs Specialty offering and to improve the profitability of acquired assets. Ahern’s EBITDA ranges within 35%-38.5% whereas last 5 year average of URI is 44% – Purchase EBITDA multiple of 6.5x

The multiples paid by URI appear higher than the ones paid by Ashtead, though, Ashtead does not disclose these multiples per transaction as acquisitions are significantly smaller with only 7 deals above $100M and an average multiple of 6.1x. As expected, Specialty deals carry higher multiples due to their higher margins.

By comparing Ashtead to URI Returns on Invested Capital (“ROIC”), Ashtead appears to generate higher returns which can be attributed to the different growth strategy (e.g. URI has an aggressive acquisition strategy whereas Ashtead mainly invests organically and with smaller acquisitions). Peer to peer or year on year comparisons for earlier years do not make sense without further adjustments for operating leases capitalization (more appropriate as in substance this is a debt).

Source: Koyfin, StockOpine analysis, Note: [1] FY9 for URI ends on 31st of December 2021 and for Ashtead on 30th April 2022, [2] ROIC = Operating profit after tax (25%) / (Average Shareholder’s Equity + Debt (incl. leases), deferred taxes less Cash), [3] Number in the text box represents URI’s large acquisitions for each period.

Historically, it can be observed that URI manages to smoothly integrate acquisitions, as the impact on ROIC is immaterial despite the fact that it takes 18-36 months for acquired companies’ ROIC to exceed cost of capital (disclosed by management). Nonetheless, acquisitions do carry risks of overpayment and can be value destructive. URI is no exception with $1.56B accumulated impairment charges (or 22% of goodwill initially recognized) as of 31 December 2021 with the latest recognized impairment charge of $1.1B dating back to Q4 2008 as a result of the challenges to the construction cycle and economic conditions. It shall be noted that this charge was related to acquisitions made between 1997 and 2000. The results of the annual testing taking place in October would be interesting given the current economic environment.

8. Competitive advantages, Opportunities and Risks

This section is brief so as to avoid repeating what was stated in section 6 of our Ashtead write-up. For additional information you can refer to that write-up.

Competitive advantages

Scale providing better pricing power on purchases from OEMs (Original Equipment Manufacturers) and cost efficiencies resulting to better unit economics.

Due to their size they have better access to debt financing, a critical strength under the current environment.

High barriers of entry due to high CAPEX requirements repelling new entrants.

Opportunities

$1 trillion US Infrastructure bill, Transformation of automotive manufacturing plants to support EV, CHIPS Act and Inflation Reduction Act.

Matthew Flannery, CEO:

“One is a $550 billion of funding in the U.S. infrastructure bill, which will finally put shells in the ground starting in '23. This should trigger at least 5 years of opportunity.”

“There's another $440 billion of federal tax incentives in the Inflation Reduction Act for clean energy and plant upgrades. And we think these will have a 5- to 10-year impact.”

“This year alone, hundreds of billions of dollars of new investment in manufacturing have been announced. Investments are already underway in automotive electrification, microchip factories and the broader trend towards onshoring.”

High economic uncertainty making rental option appealing in the attempt to conserve capital.

Risks

Slowdown in the construction cycle (50% of 2021 URI’s Customer mix is in construction).

Diminishing returns on capital or impairment charges due to acquisitions.

9. Valuation

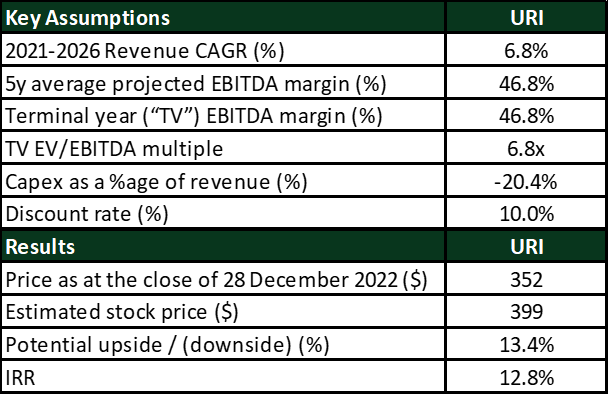

The stock price as of 28th of December 2022 stands at $352 and is up by 6% YTD. The Company's market capitalization is $24.5B and it trades at an EV/EBITDA TTM multiple of 6.8x, compared to Ashtead's EV/EBITDA TTM multiple of 8.5x. Based on our DCF valuation, the estimated price of United Rentals is $399, which is 13.4% higher than the current price, with an IRR over a 5-year period of 12.8%.

Source: StockOpine analysis

To estimate the fair value of United Rentals, we assumed a revenue CAGR of 6.8%. For FY 2022, we used a revenue growth rate of 19%, in line with management's guidance in Q3 2022. Beyond FY2022, we estimated revenue growth rates based on industry expectations without assuming any market share gains as any market share gains are likely to be achieved through acquisitions.

In terms of profitability, we used an average and terminal projected EBITDA margin of 46.8%. Both the average and terminal EBITDA margins are higher than the average 5-year EBITDA margin of 44.4% for 2017-2021. We did not assume further improvement in profitability as it is possible that the recent spike is due to tailwinds benefiting the industry in fiscal year 2022 that may not recur in future years.

To derive the free cash flow to the firm, we deducted projected capex requirements of $2.5 billion, or 21.9% of revenue for FY22. This is based on the net rental capex guidance provided by management of 20.3% plus non-rental capex of 1.7% for the last twelve months. Beyond FY23, we reduced capex requirements to 20%, in line with the company's 10-year average (excluding FY20, when capex was impacted by COVID-19).

In terms of the terminal EV/EBITDA multiple, we assumed to be around 6.8x which equals its 5-year average excluding FY20.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on these calculations and assumptions (which may not materialize), we estimate a value per share of $399, which is higher than the current price of $352, resulting to an IRR over a 5-year period of 12.8%.

Sensitivity analysis

The below table gives an indication of the potential upside/(downside) %age compared to the current price ($352 as of 28th December 2022) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

10. Concluding Remarks

In line with our conclusion about Ashtead, we believe that URI has similar advantages such as durable business model, economies of scale and it benefits from high barriers of entry.

After concluding the head to head analysis, Ashtead appears marginally better in terms of profitability, rental yield and liquidity/solvency, though, URI appears to have a marginally better culture justified by Glassdoor score and lower employee turnover ratios. Based on our analysis, both companies are trading close to their fair values, with United Rentals having some upside potential. However, we have decided not to initiate any positions in either company at this time. We will continue to monitor their progress, evaluate their outlook for 2023, and re-assess both companies. Stay tuned for updates!

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

Excellent analysis, especially the head to head comparison of the two key players in the equipment rental industry.