Valuation update: Ashtead Group plc ($AHT.L)

Positive Signs Emerge After a Slowdown

It's been a while since our last update on Ashtead Group (LSE: AHT) in February 2024, “Ashtead: Building Success Brick by Brick”, and its time to revisit our valuation.

In case you are unfamiliar to the company, Ashtead is the second-largest equipment rental company in U.S., holding an 11% market share (up from 4% in 2010), in a highly fragmented, $80.9 billion industry. The company operates under the Sunbelt Rentals brand.

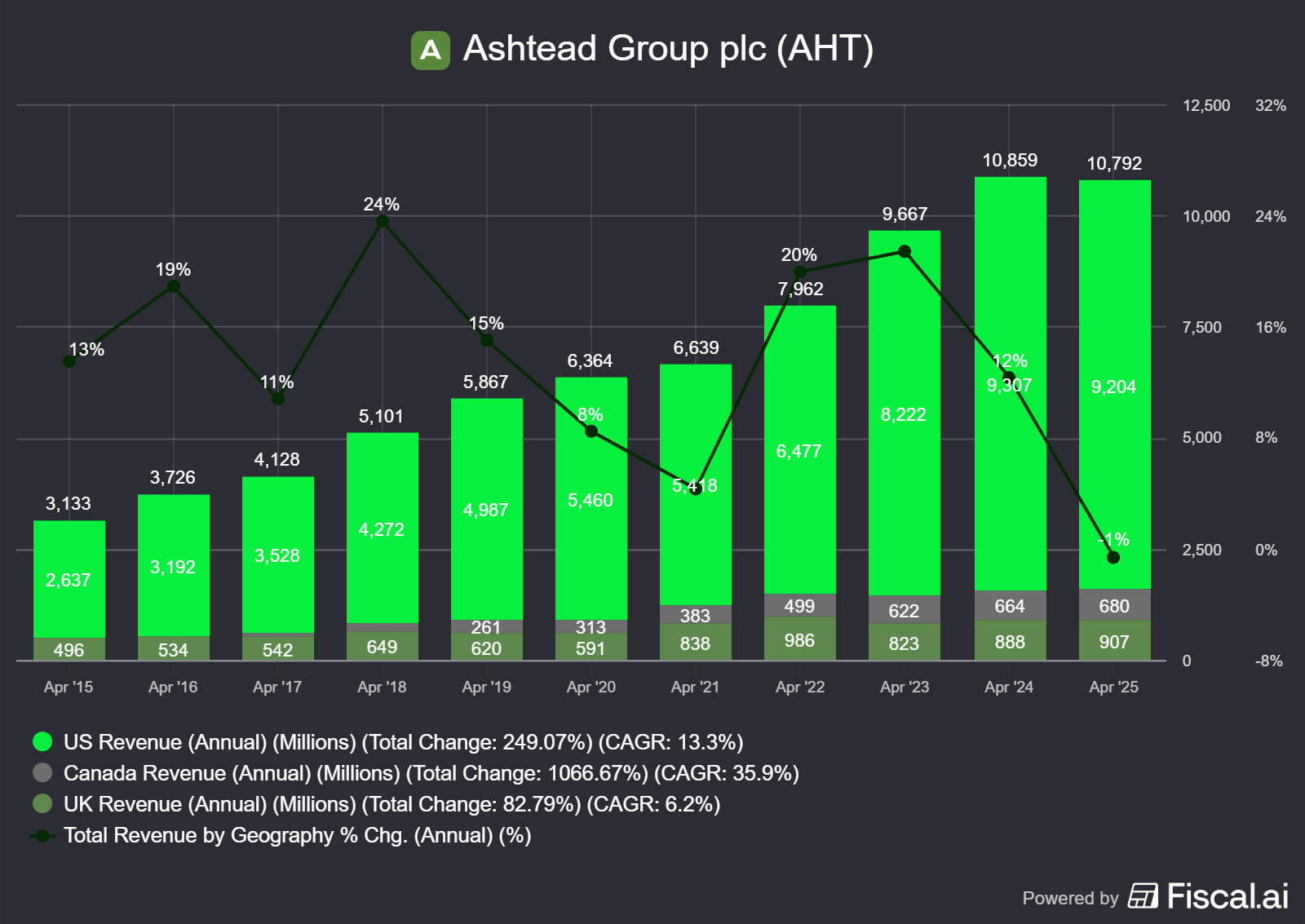

Over the past decade, Ashtead has grown its revenue at a 13% CAGR, reaching $10.8 billion in its most recent fiscal year (FY25), with 92% of that revenue coming from North America. This growth has been fueled by a successful strategy of acquiring smaller competitors and opening new "greenfield" locations.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Looking ahead, Ashtead forecasts the North American rental market will grow from $84 billion in FY24 to $100 billion by FY29, a 3.3% CAGR. Ashtead’s target is to grow 2x the industry and capture more market share.

While the high-interest-rate environment has been a headwind for commercial construction, a surge in mega-projects like data centers and manufacturing facilities is expected to be a major growth driver. In fact, Ashtead highlights that the pipeline for these large-scale projects in North America is projected to swell from ~$840 billion (FY23-FY25) to over $1.3 trillion (FY26-FY28).

1. Business Segments: General Tools & Specialty

Ashtead splits its North American revenue into two main segments:

General Tools (65% of revenue): This includes mostly construction equipment like mobile elevating work platforms (40%), forklifts (26%), and earth-moving equipment (18%).

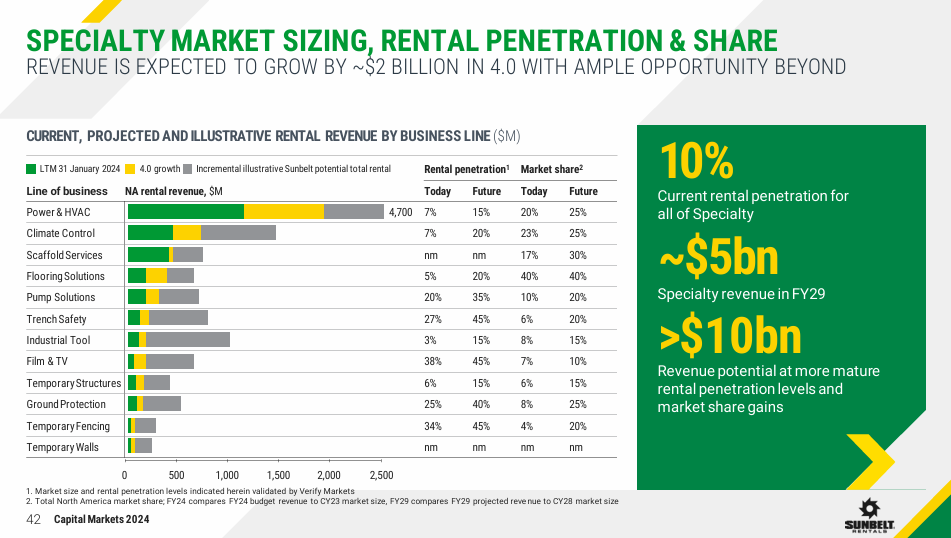

Specialty (35% of revenue): This segment focuses on products for non-construction markets with lower rental penetration, such as Power, HVAC, and Climate Control.

Notably, the Specialty business has been the primary growth engine, expanding at an average annual rate of 21% from FY18-FY25, compared to 11% for the General Tools segment.

Source: Capital Markets Day 2024

2. Sunbelt 4.0 Financial targets

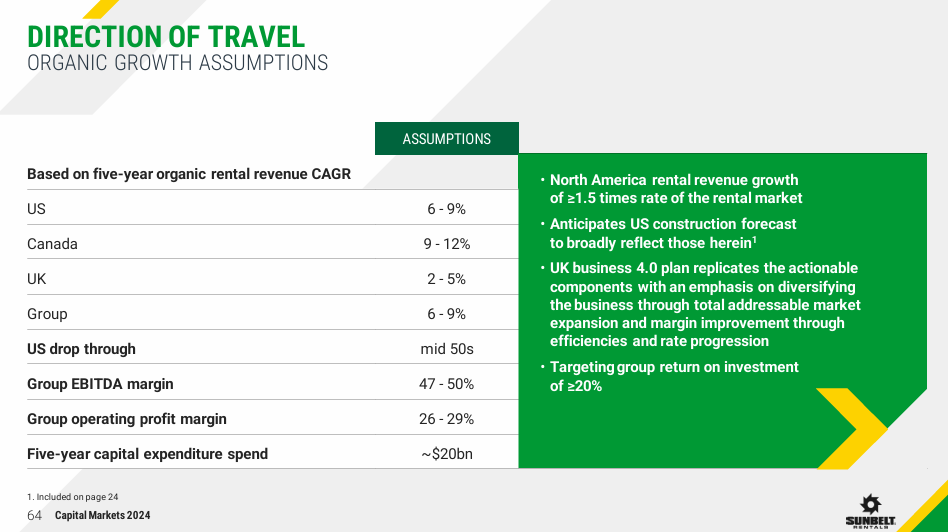

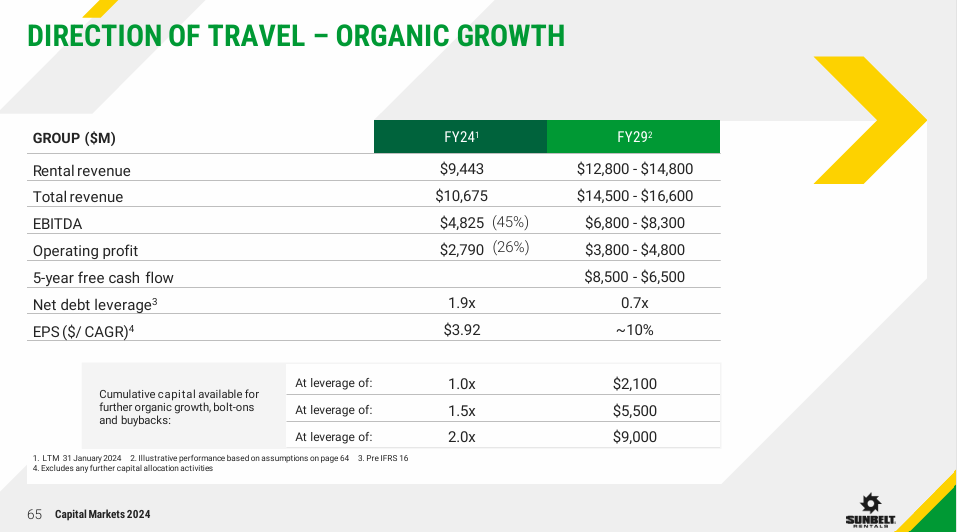

In April 2024, the company unveiled its "Sunbelt 4.0" strategic plan, setting financial targets through FY29. The plan aims for annual revenue of approximately $15.5 billion, driven by targeted annual growth of 6-9% in the US, 9-12% in Canada, and 2-5% in the UK. Based on FY24 revenue of $10.8 billion, the projected CAGR is 7.5%

Source: Capital Markets Day 2024

Source: Capital Markets Day 2024

A major contributor will be the Specialty business, which is expected to scale from $3.5 billion in FY25 to $5 billion by the end of FY29.

To achieve this, management plans to invest $20 billion in capital expenditures (CAPEX) over the five-year period while expanding its EBITDA margin to a target range of 47-50% (up from 46.4% in FY25). This margin improvement is expected to come from leveraging SG&A costs, optimizing pricing, increasing equipment utilization, and the maturation of newer locations. As an example, the 401 locations added during the previous "Sunbelt 3.0" plan have already demonstrated a 200 basis point (2%) margin improvement over the past year.

3. Recent Performance & FY26 Outlook

FY25 results (Year ending April 2025)

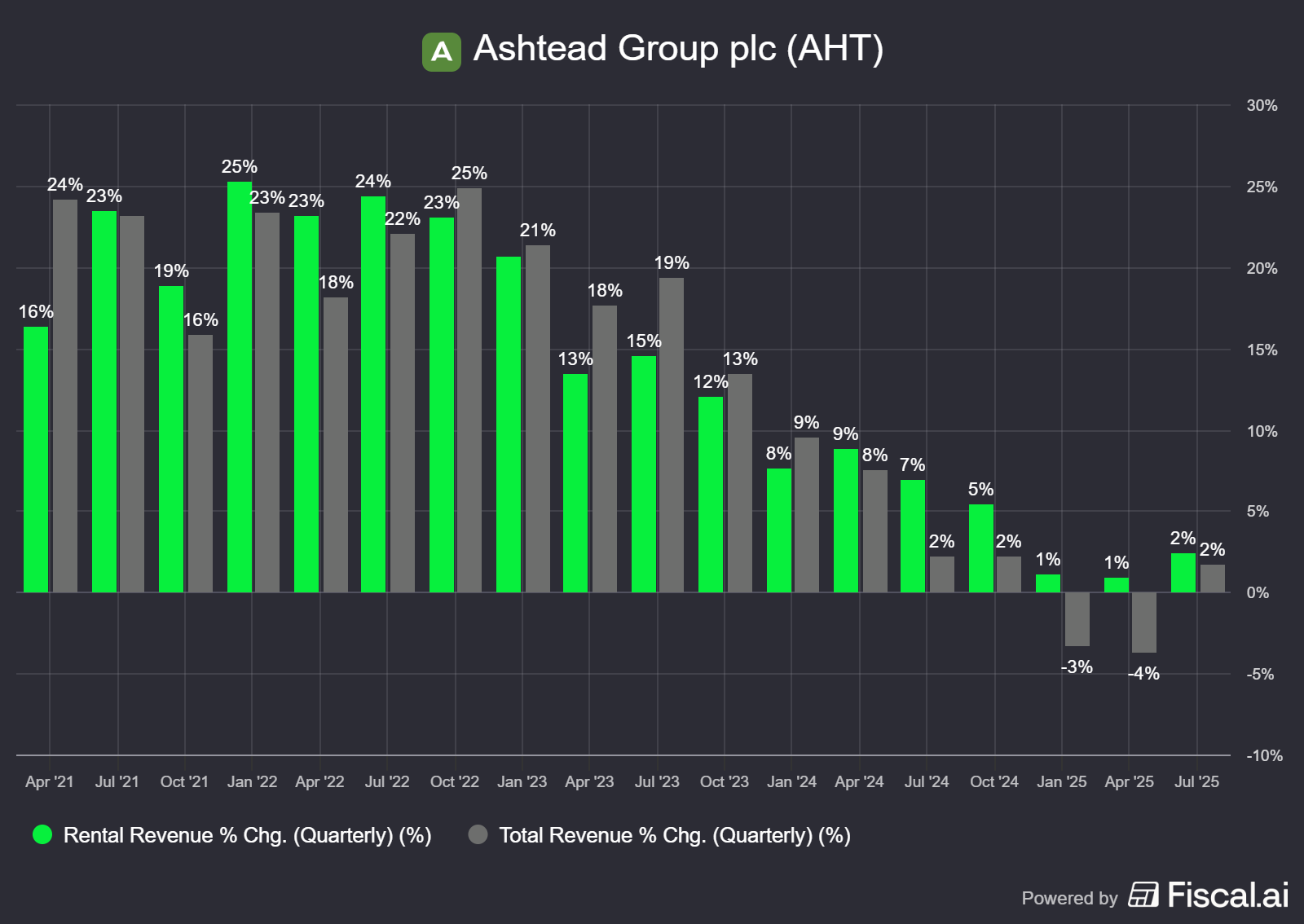

For the full fiscal year 2025, the company saw decelerating growth due to the impact of high interest rates on commercial construction and lower used equipment sales. Total revenue was $10.8 billion (-0.6% YoY), though rental revenue grew a modest 3.6% YoY to $9.98 billion. Despite the top-line slowdown, the company improved its EBITDA margin to 46.4% from 45.1% in the prior year, thanks to a higher mix of rental revenue.

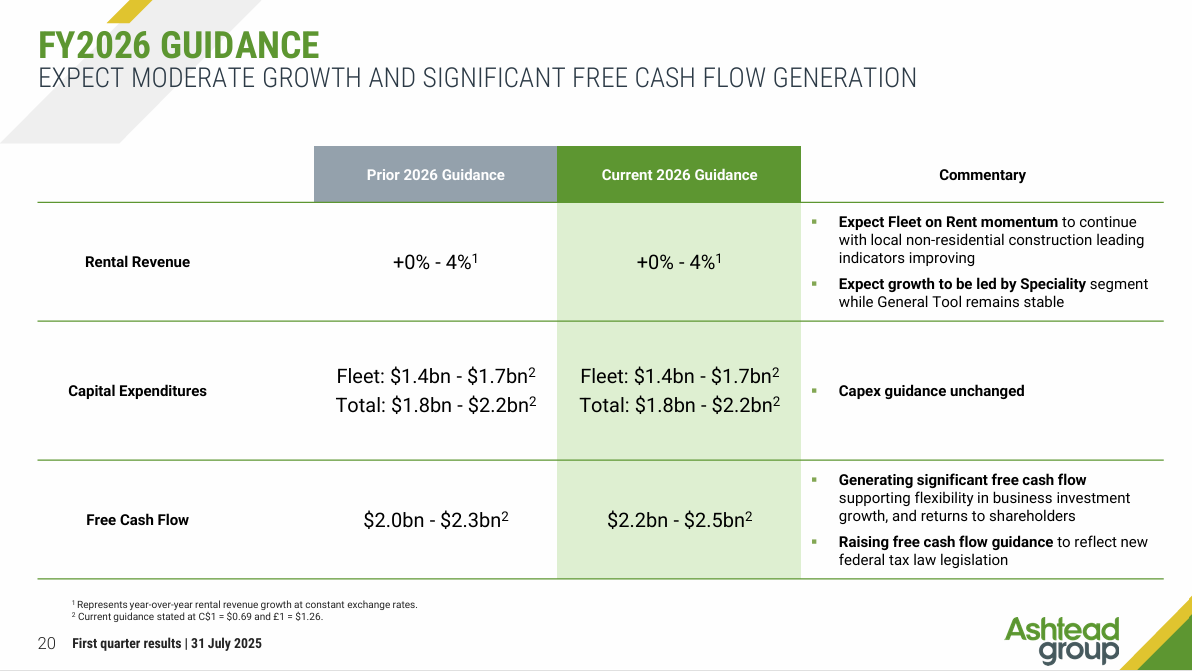

Q1’26 and FY26 Outlook

Last week's Q1 FY26 report showed signs of a potential re-acceleration. Group rental revenue was up 2.4% YoY (Vs 0.9% growth YoY in Q4’25) and total revenue was up 1.7% YoY (Vs -3.8% growth YoY in Q4’25).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Additionally, management noted that internal leading indicators are trending favorably compared to a year ago.

“We actively track leading indicators such as quotes, reservations, daily new contract activity and continuing contracts as a way to measure the health of our pipeline. And all these indicators are trending positively and favorable to what we experienced a year ago this time. Whilst too soon for these leading indicators to form certainty, we're cautiously optimistic that these trends in our business will continue and are early signs of the local nonresidential portion of our end markets recovering.”

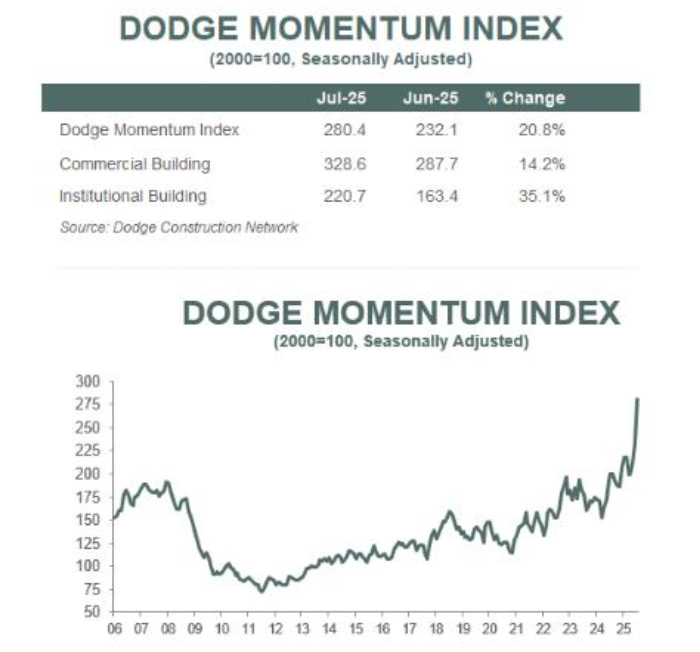

External indicators are also encouraging. The Dodge Momentum Index, a key indicator for future non-residential construction, spiked in July, rising 21% year-over-year. A potential construction boom in the next 12-24 months would be a major tailwind for Ashtead.

Source: Dodge Construction Network

Q1'26 EBITDA margin was 45.6%, down from 46.8% in Q1'25. This was attributed to higher ancillary revenues (which carry lower margins) and increased repair costs as the large fleet purchased in FY23-FY24 comes off warranty. The company reaffirmed its full-year revenue and CAPEX guidance for FY26, while it increased its free cash flow due to tax benefits arising from the One Big Beautiful Bill which allows for immediate depreciation of new equipment for tax purposes.

Source: Ashtead Q1’26 Earnings Presentations

4. Valuation

The following is a summary of our valuation which is behind paywall.