Vertex Pharmaceuticals - Snapshot

PROFILE

Vertex Pharmaceuticals is a biotechnology company which develops drugs for the treatment of serious diseases with focus on specialty markets. Vertex has been specialising in the treatment of cystic fibrosis (“CF”), obtaining its first drug approval in 2012 and is a dominant leader in the space with its commercial CF drugs generating $7.6 billion in revenue during fiscal 2021.

MOAT

Vertex’s moat is built around its dominance in the CF space. Its blockbuster drug TRIKAFTA/KAFTRIO can address 90% of all mutations, has high efficacy rates, and its patent expires in 2037. TRIKAFTA/KAFTRIO is approved and reimbursed/accessible in more than 25 countries. The high profitability and cash generation allow the company to further invest in drug development outside CF.

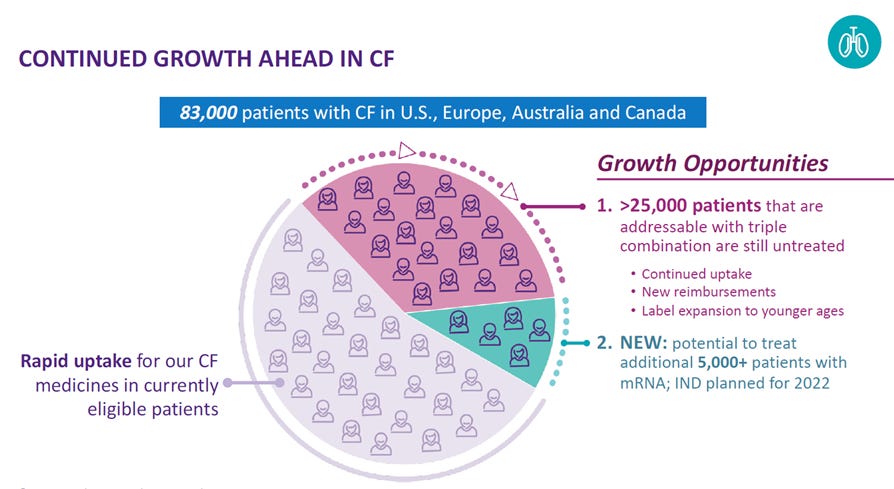

MARKET SIZE OF CYSTIC FIBROSIS

Cystic Fibrosis therapeutics global market size is expected to reach $14.2 billion by 2027 (8.2% CAGR) and Vertex’s medicines (CFTR modulators) are dominating the market. Vertex expects further growth to come from drug approvals for lower age groups as well as from the approval of reimbursement programs in foreign countries.

The Company markets its products in North America, Europe and Australia where it estimates that there are approximately 83,000 people with CF. The Company estimates that 25,000 of those patients can be treated by the Company’s CFTR modulators but they remain untreated with the Company expecting the specific population to be a major growth driver in the future. Finally, 5,000 of those patients cannot be treated by CFTR modulators, however, the Company is in a collaboration with Moderna to develop an mRNA therapy that could treat those patients as well.

Source: Vertex fourth quarter and full year 2021 Financial results presentation

PIPELINE

Vertex has several ongoing clinical and research programs to advance and extend the treatment of CF. Beyond CF, the Company’s pipeline extends to other serious diseases including sickle cell disease, beta thalassemia, APOL1- mediated kidney disease, type 1 diabetes, pain, alpha-1 antitrypsin deficiency, and muscular dystrophies.

Source: Vertex fourth quarter and full year 2021 Financial results presentation

COLLABORATION WITH CRISPR THERAPEUTICS AG

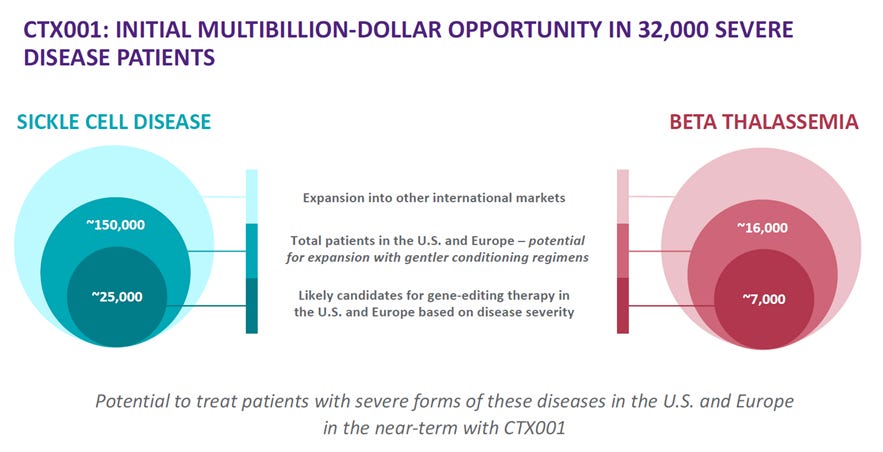

The Company’s most advanced therapy in development is CTX001 which is developed in collaboration with CRISPR Therapeutics AG and the Company expects to file for regulatory approval before the end of the year. CTX001 is a CRISPR/Cas9 gene-edited therapy that is being evaluated for patients suffering from severe sickle cell disease (SCD) and transfusion dependent beta thalassemia (TDT). According to the Company, among gene-editing approaches being evaluated for TDT and SCD, CTX001 is the furthest advanced in clinical development.

In the collaboration agreement with CRISPR, income and expenses are allocated 60% to Vertex and 40% to CRISPR. It should be noted that in the original collaboration agreement, profits and losses were shared equally, though in 2021, Vertex made an upfront payment of $900 million to CRISPR for the additional 10%. CRISPR has the potential to receive an additional one-time $200 million milestone payment upon receipt of the first marketing approval of CTX001 from the U.S. Food and Drug Administration or the European Commission.

The Company claims that this a multibillion-dollar opportunity and estimates that there are more than 150,000 patients in the U.S. and Europe who have beta thalassemia or sickle cell disease, of which approximately 32,000 have severe form disease.

Source: Vertex fourth and full year 2021 Financial results presentation

FINANCIALS

Vertex has consistently grown its revenues, from $1.5 billion in 2012 when its first CF medicine was approved, to $7.6 billion in fiscal 2021, a CAGR of 14.3%. This is explained by the approval of new CF medicines, drug approvals for lower age groups as well as approval of reimbursement programs in different countries. In Q1 2022, its revenue grew by 21.7% to $2.1 billion and per the latest guidance, revenue for FY’22 is expected to increase by 12% to $8.5 billion (using the mid-point of the guidance).

The key revenue drug is TRIKAFTA/KAFTRIO which accounts for 75% of 2021 revenue and 84% for Q1 2022 revenue (compared to 69% in Q1 2021).

Source: 10K reports, StockOpine analysis

Vertex is highly profitable with strong balance sheet and therefore can finance its research and development needs internally. This gives Vertex an advantage over similar biotech companies which seek external financing to develop new products.

Operating margin excluding upfront payments for collaboration agreements and acquisition related costs was 49% and 48% in 2021 and 2020, respectively.

Vertex has a healthy balance sheet position with cash, cash equivalents, and marketable securities of $8.2 billion as of 31 March 2022 and no debt. Furthermore, the Company generated $2.4 billion (31.8% FCF margin) and $3 billion (48.2% FCF margin) in free cash flow in 2021 and 2020, respectively. It should be noted that 2021 includes $900 million upfront payment to CRISPR. When adjusted, the FCF margin increases from 31.8% to 43.7%.

VALUATION

For the valuation of Vertex the revenue growth was based on analysts’ consensus. As a sanity check, we compared this to the industry expectations of the CF market. As it was noted above, the CF market is expected to grow at a CAGR of 8.2% by 2027 reaching $14.2 billion. It can be assumed from the above estimates that the CTX001 upside is negligibly accounted for.

In terms of profitability, we used an average projected EBITDA margin and terminal EBITDA margin of 50% which is in line with the average EBITDA margin of the years 2020 and 2021. In estimating the historic average EBITDA margin, we excluded acquisition related costs and upfront payments for collaboration agreements.

To derive the free cash flows to the firm we adjusted for projected Capex requirements based on the historic average.

In respect to the terminal EV/EBITDA multiple, it is assumed to be around 12x which is in line with the 5-year average of selected comparable companies in the biotechnology industry.

To estimate the value per share we used the minimum required return that we aim to obtain from our investments under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialise at all), it seems that Vertex is overvalued by 16.6% with a resulting IRR over a 5-year period of 5.2%.

FINAL THOUGHTS

Vertex has a strong moat business which arises from its dominance in the CF market, which has room for growth and Vertex is in a perfect position to capitalise on the opportunity. In addition, if CTX001 obtains a regulatory approval it would probably prove to be a multibillion-dollar opportunity given its total addressable market and considering that it is the most advanced treatment in its segment at this stage of development (as indicated by Management).

The key risk for Vertex is the reliance on CF medicines and if a competitor develops a superior medicine for CF, it can lead to a significant loss of revenue/profits. Additionally, failure to gain regulatory approval for medicines outside CF would limit Vertex’s future revenue growth.

We believe that Vertex is not a buy at the current price levels and superior risk/reward opportunities can be found elsewhere in the current market environment.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.