Zoom Q2'25 Earnings

Zoom ZM 0.00%↑ reported Q2’25 Earnings on Wednesday, beating guidance on both revenue and profitability. Here is a brief recap:

1. Financial results

Revenue $1.16 billion Vs $1.15 billion expected. Revenue was up 2.1% year over year and 2.4% on constant currency basis.

Non-GAAP EPS $1.39 Vs $1.21 expected.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

2. Profitability

Non-GAAP operating income at $456 million, beating guidance of $420 million.

GAAP operating margin of 17.4% compared to 15.6% in prior year. Non-GAAP operating margin of 39.2% compared to 40.5% prior year.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

3. Outlook

Zoom raised guidance for the year.

Revenue for the year expected to be in the range of $4.63 billion to $4.64 billion, up approximately 2.4% year-over-year. This is up from $4.62 billion expected in Q1’25.

And when you have a chance to really look at the guidance, right, you'll see that we are forecasting, as we said that Q2 would be the low point this year in terms of year-over-year growth, and we would start to reaccelerate in Q3. Kelly Steckelberg, CFO

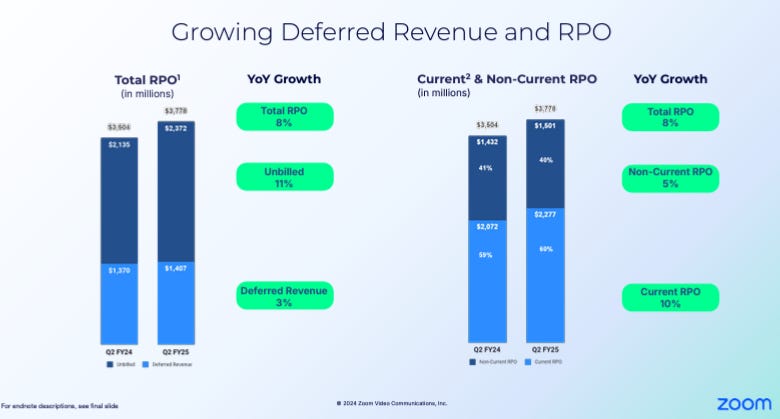

4. Remaining Performance Obligations (RPO)

Total RPO grew at 8% year over year compared to 5% growth in Q1’25, indicating that progress towards re-acceleration of revenue growth is on track.

Source: Zoom Q2’25 Earnings Presentation

5. Enterprise

Enterprise revenue grew 4% year over year, decelerating from 5.3% growth in Q1’25. Customers with over 100,000 TTM revenue grew 7% and now represents 31% of revenue, up from 29% in prior year.

Source: Zoom Q2’25 Earnings Presentation

6. Retention

Net Dollar retention rate at 98% compared to 99% in prior quarter and 109% prior year.

We've had a lot of stability in terms of our retention rates and this is going to show up eventually in our net dollar expansion that we expect to start to reaccelerate as we come to like the middle of next year. Kelly Steckelberg, CFO

7. Online Average Monthly Churn

Online average monthly churn reached all time low at 2.9%, compared to 3.2% in prior year and 3.2% in Q1’25.

8. Contact Center

During the quarter Zoom had its largest Contact Center deal. The Company surpassed 1,100 Zoom Contact Center customers representing more than 100% year over year growth.

Of our top 10 Contact Center wins, all represented displacements of major Contact Center vendors and 40% were migrations of our first-generation cloud-based solutions. Eric Yuan, CEO

9. Zoom AI Companion and Workvivo

Zoom AI Companion is now enabled on over 1.2 million Zoom accounts. This up from 700,000 in Q1’25. Workvivo reached 69 customers with over $100K in ARR, roughly doubling year over year.

10. Resignation of CFO

Kelly (CFO) is leaving the company after a seven year tenure. The Company is on the look for a new CFO.

Conclusion

Overall, Zoom delivered a strong quarter, beating expectations across the board. The company’s guidance suggests that Q2’25 marks the low point for the year in terms of growth, with re-acceleration expected in the coming quarters. This is further supported by the growth in remaining performance obligations. Zoom continues to be a leader in innovation, demonstrated not only by its success during the COVID-19 era but also by the success of its internally developed products like Zoom Phone and Contact Center, which are key contributors to its growth.

If you enjoyed this post, you can get a taste of StockOpine's offerings by claiming a 2-day free trial through the link below.