We have been closely following Zoom (“Company”) and the recent pullback in price motivated us to dig more into its valuation.

ZM 0.00%↑ reached as high as $589 during the pandemic and fell as low as $78 in September 2022 which represents an 87% decline from its all-time high. This is even lower than its pre-pandemic prices but one can argue that tech stocks were highly overvalued before the pandemic (for example Zoom EV/Sales was 50.6 in fiscal year 2020). However, it is worth noting that Zoom increased its revenue by 7-fold since the start of the pandemic, i.e. from $622M in FY’2020 to $4.3B for the trailing twelve months (“TTM”).

Before moving into the valuation, we will give a brief overview of Zoom’s business, profitability and outlook to provide more insights on the assumptions used in the valuation.

Zoom Offering

Zoom’s core product is Zoom Meetings (video conferencing solution) which played a pivotal role during the pandemic and sent Zoom’s brand awareness to the roof.

Despite this, Zoom is not just a single product company as it has been continuously adding products to its suite advancing itself into a unified communications platform. Outside Zoom Meetings, the Company’s most prominent offerings include Zoom Rooms, Phone, Contact center and Events & Webinars.

The Company does not report revenue per product, however we presume that Zoom Meetings should be in the range of 80-90% of total revenue. In Q1’23 management noted that no other product outside of core video is more than 10% of revenue, although, they exceed the 10% threshold when combined. Management expects that some of those products will exceed 10% of revenue somewhere in FY24, FY25 with Zoom Phone being first in the line.

Source: Zoom website

Revenue

While revenue growth from Zoom Meetings is on the decline, Zoom Phone (launched three and a half years ago) and Zoom Contact center (launched six months ago) show signs that they can drive future revenue growth. Management is going after a “land and expand” strategy to sell those new products to its existing enterprise customers which have been originally acquired through Zoom Meetings.

In regards to Zoom Phone and based on information provided in previous earning calls, the number of seats for Zoom Phone increased by 100% Y/Y as of August 2022. We estimate that Zoom Phone could be over $450 million in annual revenue run rate (i.e. higher than 10% of revenue) based on the 4 million seats reported by management and the lower tier pricing of $120 per seat.

The Contact center launch added $18B to Zoom’s total addressable market. Based on Gartner forecast analysis published in 2021, revenue for CCaaS (Contact Center as a Service) will reach $17.9 billion by 2024, 29% CAGR. According to management, the Contact center offering is seeing early traction with deals in Q2’23 exceeding management’s expectations.

In terms of geographical mix, Americas, EMEA, and APAC consist of 69.4%, 17% and 13.6% of revenue, respectively as per the latest quarter Q2’23.

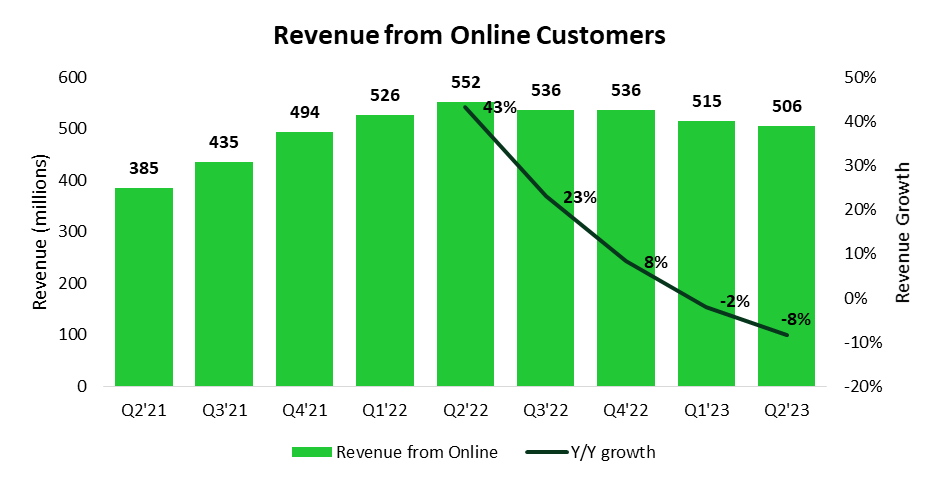

Zoom reports its revenue into enterprise and online business. Enterprise business consists of customers which are engaged by either direct sales team, resellers, or strategic partners whereas online business consists of customers self-serviced through the online channel. We presume that the online channel is mainly small businesses and individuals.

Revenue from enterprise customers in Q2’23 grew by 26% year-over-year (“Y/Y”) and represented 54% of total revenue, up from 46% in Q2‘22. Revenue growth from enterprise remains strong due to the increase in number of customers and due to existing customers spending more (TTM net dollar expansion rate for Enterprise customers was 120%).

Source: Zoom 10Q reports, StockOpine analysis

On the other hand, revenue from online business was down 8% Y/Y in Q2’23 (management was expecting flat Y/Y growth). According to management, retention rates for the online improved in the last quarter, however Zoom strived on new additions.

Source: Zoom 10Q reports, StockOpine analysis

Profitability

Zoom’s profitability exploded during the pandemic with Non-GAAP operating margin reaching as high as 37% and 40.4% in fiscal years 2021 and 2022, respectively. For fiscal 2023, management retained its guidance of Non-GAAP operating margin of approximately 33%.

It shall be noted that Non-GAAP profitability does not include Share Based Compensation (“SBC”) which grew exponentially in the recent quarters and reached 23% of revenue in Q2’23.

Source: Zoom 10Q reports, StockOpine analysis

The exponential increase in SBC is due to retention measures to compensate employees who initially received Restricted Stock Units (“RSUs”) when the stock was in the range of $300-400s. While this seems reasonable in order to retain talent and keep employees happy, it’s still a significant dilution to shareholders and is taken with a ‘grain of salt’.

At least, management expects those RSU top-up programs to be temporary, however, they will continue to impact the P&L in the near term.

Kelly Steckelberg, CFO, So we certainly have seen an elevation in that level of stock-based comp and it's temporary, but it's not temporary for the rest, I mean, you should expect to see those elevated levels, at least for the rest of this year.

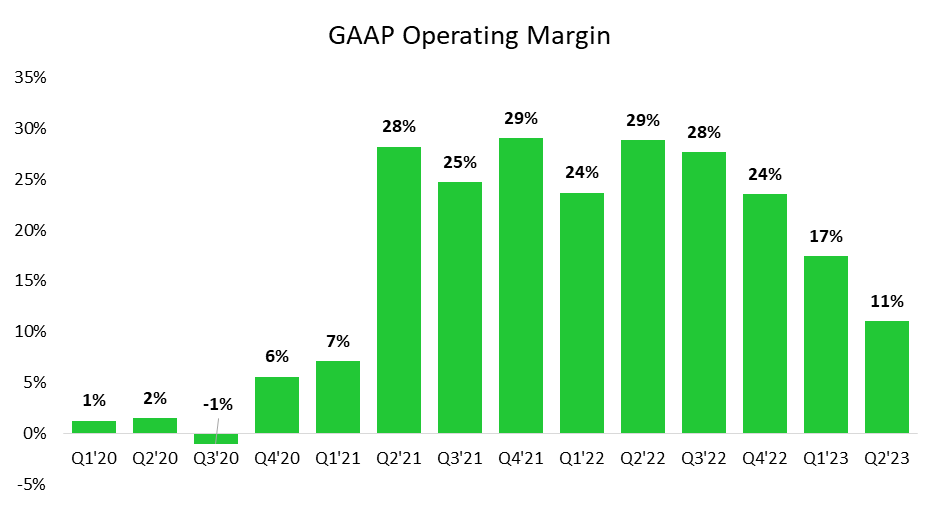

In terms of GAAP profitability, Zoom’s operating margin reached as high as 24.9% and 27.6% for fiscal years 2021 and 2022, respectively, but it has been deteriorating since Q2’22.

Source: Zoom 10Q reports, StockOpine analysis

In addition to the top-up RSU programs, the deterioration in profitability since Q2’22 is a result of the investments in the relatively new products (e.g. Contact center, IQ for sales and Zoom Phone) and the tough prior year comparisons where Zoom was heavily under invested.

Kelly Steckelberg, CFO during Deutsche Bank 2022 Technology Conference, So our R&D teams have been heavily under invested over the last couple of years. And then our sales and marketing team focusing on sales capacity, especially internationally channel, and then very specifically, opportunities around product marketing. Historically, we've done a lot of brand awareness building that exploded during the pandemic, but there are a lot of people that, again know Zoom Meetings that don't know, Zoom Phone, Contact Center, et cetera. So those are all the areas of investment opportunity.

If you think about it, back in June 2021, Zoom was going to acquire Five9 (Contact Center as a Service company) for $14.7 billion, however the deal was terminated and Zoom decided to develop its own contact center. Therefore, starting a product from zero would require significant investments in R&D (Research and Development) and S&M (Sales and Marketing) which will burden operating margins in the near term.

Outlook

In Q2’23, Zoom missed revenue guidance for the quarter and reduced its guidance for fiscal 2023 by $150 million (revenue guidance decreased from $4,540 to $4,390 million), implying a revenue growth of 7% Y/Y for fiscal 2023.

The reasoning for the reduction was foreign exchange headwinds of $35 million and the pressure on the online business which is expected to be down by 7-8% (previous expectation was flat revenue growth). According to CFO, Kelly Steckelberg, Zoom expects online business to flatten and return to growth during Q2 FY24.

In terms of profitability, Zoom reiterated its Non-GAAP operating margin guidance of approximately 33%.

Valuation

The stock price as of 13th of September 2022 stands at $78.86 and is down by 57% YTD. The market cap of the Company stands at $23.5B and trades at an EV/EBITDA TTM multiple of 19.3x. Based on our DCF valuation the estimated price of $ZM stands at $89, which is 12.7% higher than the current price level, with a resulting IRR over a 5-year period of 13.9%.

Source: StockOpine analysis

To estimate the fair value of Zoom we assumed a revenue CAGR of 10.3% compared to analysts’ consensus of 10.8% CAGR. The 10.3% GAGR, is a result of 18.3% CAGR for the enterprise business and 0.2% for the online business.

We have gradually decreased Enterprise business revenue growth from 24.6% in FY’23 to 15% in FY’27. We consider this assumption to be fair given the estimated UCaaS market CAGR of 13.4% for the period 2022 – 2028.

For the online business, we assumed that revenues will flatten in FY’24 and increase by 3% per year thereafter.

In terms of profitability, we used an average projected EBITDA margin of 13.4% and terminal EBITDA margin of 18%. Both average and terminal EBITDA are lower than the EBITDA margin of FY’21 and FY’22 of 26% and 29%, respectively. We consider this assumption reasonable due to the increased investments in R&D and S&M to support new products and the RSU top-up programs.

The EBITDA margin improvement during FY’23 to FY’27 is based on SBC returning to more normalized levels and the slight leverage that the Company expects to have on its General and Admin (“G&A”) expenses.

To derive the free cash flows to the firm we deducted projected Capex requirements of 2.7% based on the median of selected companies in the software sector.

In respect to the terminal EV/EBITDA multiple, it is assumed to be around 25.5x which is based on the median EV/EBITDA multiple of 41 selected software peer companies.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialise at all), we reach a value per share of $89 and thus Zoom seems to be undervalued by 12.7% with a resulting IRR over a 5-year period of 13.9%.

Sensitivity analysis

The below table gives an indication of the potential upside/downside %age compared to the current price ($78.86 as of 13th of September) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

Concluding Remarks

Despite that the potential IRR meets our hurdle rate, the current risks and uncertainties put us off (for the time being). For example, is work from home here to stay? Is hybrid an acceptable work format? Why not Microsoft Teams given its complete suite in Office 365? Tough questions to answer...

Nevertheless, we are excited about Zoom’s execution so far and we will be closely monitoring for positive signs of continuous execution which will let us revisit our decision. The below are our key focus areas:

Continuous momentum of Zoom Contact Center and Zoom Phone with the latter surpassing 10% threshold in early FY’24.

SBC trend reversing and moving towards more normalised levels in FY’24 and beyond.

Online business revenue growth flattening in Q2’24.

Previous write ups on Zoom Video Communications Inc.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.