Zoom Video Communications - Earnings Review Q1'23

Zoom Video Communications Inc., $ZM reported its fiscal Q1’2023 results on 23 May 2022. The below commentary is a preview of Q1’2023 earnings. Overall, it was a good quarter for Zoom given the market expectations and compared to the results of other pandemic-era darlings.

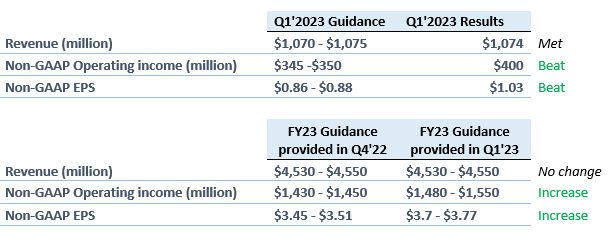

RESULTS Vs GUIDANCE

REVENUE

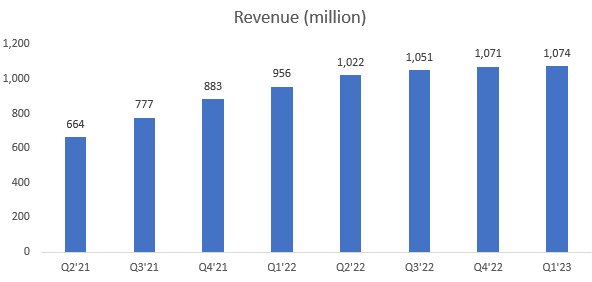

Revenue up 12% year-over-year to $1,074 million.

Growth was driven by the increase in enterprise customers as well as the increased spending from existing customers. The significant sequential deceleration of revenue growth from Q4’22 to Q1’23 was somewhat expected due to the churn of small business and individuals after the easing of COVID-19 restrictions. Effectively, this explains the decline in the number of customers with >10 employees as observed in the below table.

ENTERPRISE CUSTOMERS

Revenue from Enterprise customers grew 31% year-over-year and represented 52% of total revenue, up from 45% in Q1‘22. Enterprise customers are the bread and butter for Zoom; therefore, it would be vital for the Company to continue growing total revenue from those customers.

The number of Enterprise customers grew 24% year-over-year to approximately 198,900 and management expects revenue from Enterprise customers to become an increasingly higher percentage of total revenue over time.

We believe that such trend is important for the sustainability of growth as enterprise customers tend to have higher switching cost.

Trailing 12-month net dollar expansion rate for Enterprise customers in Q1 came in at 123%, down from Q4’22 of 129%. This is not a bad signal as it lies above 100%.

Source: Zoom Q1’23 Earnings presentation

The land and expand strategy seem to be working well for the enterprise customers who spent more with the Company, despite the Covid-19 restrictions easing. We believe that the main reasons for this, is the new hybrid work environment practice as well as the success of the Company in launching new products (i.e., Zoom Phone, Contact centre). In our opinion, continuing to offer additional solutions to existing customers could make Zoom a vital part of workflow streams within those organisations and thus increase switching costs.

PROFITABILITY

Non-GAAP operating income of $400 million compared to $401 million prior year, and non-GAAP operating income margin of 37.2% compared to 41.9% prior year.

GAAP operating income of $187 million compared to $226 million prior year, GAAP operating income margin of 17.4% in Q1’23 compared to 23.7% in Q1’22.

Even though gross profit margin increased from 72.3% to 75.6% year-over-year, operating margin declined due to operating expenses outpacing revenue growth. While this is concerning as software businesses tend to have high operating leverage, it was somehow expected since the Company is investing in new products, adding new customers and expanding within the existing ones. Let’s not forget that Zoom developed the contact centre product internally after the Five9 acquisition did not went through.

Our key concern is the stock-based compensation which was $209 million in Q1’23, up 112% year-over-year increasing dilution for shareholders. In addition, SBC as a % of revenue is increasing.

FINANCIAL POSITION, SHARE BUYBACKS AND CASH FLOWS

Cash and marketable securities as at 30 April 2022 are $5.7 billion with zero debt. A clean balance sheet with plenty financial resources to support investments.

Cash flow from operating activities was $526 million (49% of revenue) compared to $533 million in Q1’22 (56% of revenue).

Free cash flow of was $501 million (46.7% of revenue) compared to $454 million in Q1’22 (47.4% of revenue).

After announcing the share buy-back plan last quarter, the company purchased $132 million of stock, representing 1.2 million shares, implying an average cost of $110 per share.

OTHER NOTES FROM THE EARNINGS CALL

Product launches this quarter Zoom Whiteboard and Zoom IQ for sales.

No other product outside of core video is more than 10% of revenue at this point, however, they exceed the 10% threshold when combined. Management expects that some of those products will exceed 10% of revenue somewhere in FY24, FY25.

Kelly Steckelberg, CFO on a question about macro concerns “we really have it, especially in enterprise, we have continued to see strength in renewals as well as additional new customers and expansion into additional products. So, we really haven't seen that in terms of concern. I think we've heard from other people that what they're really focused on might be, if they're limiting spending, it's focused more around potentially hiring or travel. And, of course, Zoom is a great alternative if they're focusing on limiting internal travel. And so, we really haven't seen that impact today.”

OUR TAKE FROM Q1’2023 EARNINGS

Zoom is not just a video communication platform and management is making efforts in expanding its product suite and be a UCaaS platform.

We do not see any sign that management is not executing. On the contrary, Zoom continuously wins enterprise customers and existing enterprise customers spend more.

SMEs and individuals will most likely churn over time since they don’t use the platform to the same extent on the post pandemic era but the key is enterprise customers.

Overall, we believe that Q1 was the first indication that Zoom is not just a ‘covid’ stock. Surely, it was one of the greatest beneficiaries, but it seems that management can drive it a step further compared to other covid 19 darlings.

Disclaimer:

The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.