This annual StockOpine letter reviews our portfolio’s performance, decision-making, and the lessons from both our winners and losers over the past year. Below is what we cover:

What worked, what didn’t, and what we learned at StockOpine

Portfolio performance: returns, benchmark comparison, and key quantitative metrics

Portfolio components, activity and attribution (Q4’25): buys, sells, winners, and losers (paid only)

What we are watching next year (paid only)

(eToro is a multi-asset investment platform. The value of your investments may go up or down. Your capital is at risk.)

1. StockOpine Newsletter

We started the year with around 9,100 subscribers and today stand at roughly 7,800. At first glance, that looks like a step backwards. It wasn’t.

In July, we removed more than 1,600 inactive subscribers to ensure the community remains genuinely engaged with the content we publish. The outcome was better email deliverability and a materially higher open rate. At the same time, Substack followers grew from ~12,500 to ~17,000, while engagement on posts and Notes continued to improve. Fewer subscribers, but better ones.

During the year, we shared a wide range of stock ideas. Some aged extremely well. Teradyne and Micron are up roughly 226% and 187%, respectively, since publication. We also went deep into AI-related companies such as AMD (up ~99% since publication) and ASML, cybersecurity names like Fortinet, and software businesses including HubSpot and Intuit (see the Deep Dive section for the full list).

What you engaged with the most was our ASML Deep Dive, and for good reason as the stock is up around 80% since publication. Other strong engagement came from our coverage of Invisio, a small-cap defense company, our valuation update on Evolution (where we continue to believe the company is undervalued), and our Alphabet valuation update in early June. At a time when panic was widespread, we outlined three scenarios and concluded that selling was the wrong decision. Since then, Alphabet is up roughly 100%.

As part of our core Deep Dive offering, we expanded the format to include valuation updates and Portfolio News, a weekly overview of what’s moving our holdings. In December, we also started making our valuation models available to premium members, with the latest one covering Grab.

On mistakes, two stand out.

The first was Lululemon. We held the position longer than we should have, hoping product newness would revive US sales and justify the valuation, while leaning on international growth as a hedge. That never materialised. Instead, we heard repeated excuses from management, and we eventually exited. It remains a great brand, but consumer discretionary exposure can quickly erode returns when fundamentals fail to catch up with valuation. There’s renewed interest now, with increased activist involvement and the stepping down of Calvin McDonald, but this was still a miss on our side.

The second, and much worse, was Leslie’s, our poorest investment decision of 2025. We looked for a turnaround in a heavily indebted business, hoping for a market recovery. The real mistake was doubling down after the stock fell. Sometimes the right move is to pause and ask what the market is telling you. Instead of sticking with PoolCorp, a high-quality compounder with strong economics (ROIC above 17%, ROE near 29%, gross margins around 30%, operating margins near 11%), we chased upside in a low-quality business. With higher risk doesn’t just come higher returns; it also brings permanent capital loss. Leslie’s had no quality metrics, and it didn’t fit our strategy. That’s on us.

But that’s investing. You get calls right, you get others wrong. The only option is to keep learning and improving.

2. Portfolio Performance

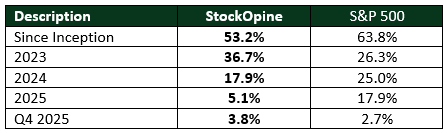

As of December 31, 2025, the portfolio returned +3.8% in Q4, outperforming the S&P 500 by 110 bps (index: +2.7%).

For the full year 2025, performance lagged the benchmark meaningfully (+5.1% vs. +17.9%). The underperformance was driven primarily by the mistakes discussed above, alongside flat performance from Meta and weaker than expected contributions from PayPal and other holdings. We will break this down in more detail later in the article.

Since inception (January 28, 2022), the portfolio has delivered a +53.2% cumulative return, equivalent to ~11.5% annualized. Over the same period, the S&P 500 returned +63.8%.

Source: S&P Dow Jones Indices, Broker, StockOpine analysis

Portfolio Insights

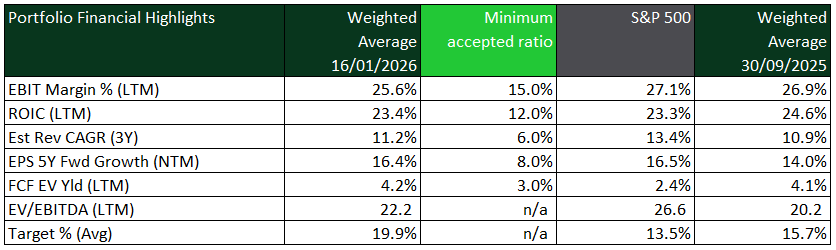

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers), StockOpine analysis

From a quality perspective, the portfolio remains well balanced and comfortably above our internal thresholds. ROIC stands at 23.4%, broadly in line with the S&P 500 at 23.3%, while EBIT margins of 25.6% remain well above our minimum accepted level. The modest quarter-over-quarter drop in ROIC was largely driven by recent portfolio changes rather than deterioration in underlying business quality.

One of the new additions, Grab, currently carries a near-zero ROIC, which diluted headline quality metrics. However, this was offset by a meaningful improvement in the portfolio’s expected EPS growth, now 16.4%, up roughly 240 bps versus the prior quarter. This reflects our willingness to accept short-term pressure on quality when medium-term earnings growth improves materially (ROIC will eventually catch up).

While quality metrics are broadly in line with the index, valuation metrics are strong. The portfolio trades on a free cash flow yield of 4.2%, compared with 2.4% for the S&P 500, and offers ~20% weighted analyst upside versus ~13.5% for the index. Taken together, the portfolio combines quality with more attractive valuation and forward return potential.

Attribution: What Drove Returns This Quarter

As of January 16, 2026, the portfolio consists of 20 holdings.