Adyen Investor Day: From gaining share in payments to owning the financial lifecycle

Key takeaways from Investor Day and an updated valuation

About 20 days ago, Adyen held its 2025 Investor Day, where management clarified the strength of its moat, explained how its banking licenses set it apart from peers, outlined the future of embedded financial products, introduced its thinking on agentic commerce, expanded on its dynamic identification capabilities for smarter risk and authorization decisions, and provided a clearer view of the TAM that helps investors gauge the runway ahead.

We reviewed the new information, revisited our valuation, and assessed whether our position needs adjustment.

If you want more context before we dive in, check out last year’s deep dive: Adyen: Simplifying Payments with Top-Notch Quality

1. The Durable Moat: Single Platform and Banking Licenses

The investment thesis for Adyen has always rested on its “single platform” architecture. Combined with their proprietary banking licenses, it creates a compounding advantage that is becoming increasingly difficult for competitors to replicate.

CTO Tom Adams articulated the cost of fragmentation. Most legacy competitors and even modern fintech peers rely on a patchwork of systems, different stacks for different regions, or acquired gateways. This creates an “integration tax” where data is lost in handoffs, and innovation slows down.

Adyen’s single codebase and single tech stack allows for accountability at the core and pragmatism at the edge. This means:

Compounding Performance: An optimization built for a merchant in Singapore is immediately available to a merchant in Brazil. Every transaction trains the same global model.

Agility: New capabilities do not require building new stacks; they are modular extensions of the existing foundation.

Banking Licenses

While the tech stack is the engine, the banking licenses are the rails. Mariëtte Swart (CRCO) argued that we are entering the “age of infrastructure,” where owning the license is critical for resilience. It is no longer a nice to have feature.

Adyen now holds full banking licenses in Europe, the UK, and the US. This is distinct from the “partner bank” model used by many fintechs (e.g., Stripe, various BaaS providers), where the fintech inherits the risk appetite and operational fragility of a third-party bank.

Strategic Advantages of Owned Licenses

Predictability: Adyen sets its own risk appetite and owns the relationship with the regulator. That means, merchants are not subject to sudden shutdowns or delays because a partner bank changes its policy.

Speed: By connecting directly to central banks (like the Federal Reserve in the US), Adyen eliminates middlemen. This allows for true Instant Payouts 24/7/365, moving money when the customer wants, not when the banking window opens.

Uniform Product Growth: Adyen can lend from its own balance sheet and issue cards without seeking third-party permission, enabling faster scaling of financial products. This is key to the embedded financial products (issuing, capital, accounts) which we will cover shortly.

2. Dynamic Identification: The New Foundational Layer

The most significant strategic announcement was the introduction of Dynamic Identification as the third foundational layer of the company, sitting alongside the Single Platform and Banking Infrastructure.

The Co-CEO Ingo Uytdehaage described the current industry approach to identity and risk as broken. The industry relies on static checks such as uploading passports, utility bills, and manual reviews. This results in an 11-day average onboarding time, a 95% false positive rate on AML alerts and up to 10% blocked transactions for legitimate shoppers. Furthermore, GenAI has made it easy to fabricate static documents, which pushes the need for a dynamic solution that can adapt to real signals rather than fixed proofs.

Dynamic Identification replaces static checks with continuous, behavioral monitoring. Because Adyen sees €1.3 trillion in volume across online and physical channels, they have a unique view of legitimate behavior.

How it works: Instead of asking “Is this document real?”, Adyen asks “Does this entity behave like a legitimate business?” It uses a graph-based model that connects shoppers, cards, devices, and businesses. This gives Adyen visibility into real activity, when someone buys a coffee, takes a taxi, purchases a pair of shoes, and so on. According to Ingo, this pattern of behavior is hard for AI to fake.

Network Effects: If a sub-merchant on a platform has shoppers who are known to be good customers elsewhere in the Adyen network, that merchant is deemed lower risk.

“So let me give you an example. If a new merchant starts with us and the first shoppers that come in and we have seen those shoppers before that they are well-established shoppers on our platform, we don’t have to take additional steps. It’s probably a legitimate business, you don’t need to take additional steps. Or if a new merchant has a bank account or a card that has been used on our platform before, we need less manual work to verify these accounts. And these are examples how we can do it better.” Co-CEO Ingo Uytdehaage

Commercial Applications

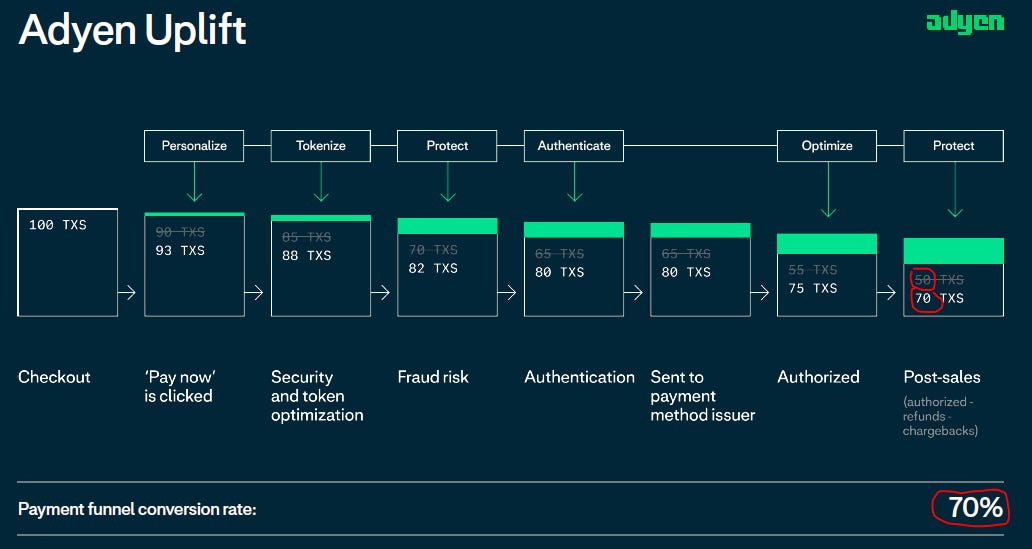

Uplift (Revenue Optimization): By understanding the shopper’s context (e.g., a high-value transaction in a foreign country is normal for this specific user), Adyen can approve transactions others would block. This has helped in reducing false positive to 42% (Vs 95%) and has delivered a 1.07% - 2.76% conversion uplift for major merchants like Just Eat Takeaway and American Eagle.

Source: Adyen Investor Day 2025

Frictionless Onboarding: Adyen can auto-verify sub-merchants. If a business owner is already a known shopper or entity in the ecosystem, they can skip manual ID checks. This has already reduced manual reviews by 6%.

Compliance at Scale: Adyen is deploying AI agents powered by LLMs to process alerts, especially for PEP (Politically Exposed Persons). These agents use Dynamic ID data to clear alerts in minutes instead of hours, with a target of 90% automation for investigations. This shift already delivers about 50% time savings internally, as reviewers can focus on the complex and high-risk cases that actually matter rather than spending time on the 95% of alerts that turn out to be false positives.

3. Agentic Commerce

Adyen is placing a strategic bet on Agentic Commerce, that is, the automation of purchasing by AI agents on behalf of consumers. While management admits this is nascent today, they view 2026 as the “year of experimentation” and estimate a $2 trillion GMV opportunity by 2030.

What is Agentic Commerce? Think of it this way: instead of a human searching, selecting, and buying, a consumer simply gives a prompt to an AI (e.g., “Find me a gray cashmere sweater under $100 and deliver it by Friday”). The AI then handles discovery, selection, and payment.

Despite the promising future of agentic commerce, Adyen noted that many merchants are terrified of disintermediation and of losing their direct relationship with customers to an AI interface. That fear puts brand and loyalty at risk, so merchant adoption won’t happen quickly.

Adyen aims to position itself as a universal translator that lets merchants accept agentic transactions while keeping control of the customer relationship. These were the four principles outlined for agentic commerce:

Verifiable intent: The shopper must clearly approve the transaction, reducing fraud and disputes.

Merchant control: A universal token carries the context so merchants keep control over cards, wallets, local methods, and their own checkout flows.

Universal recognition: As chat and voice replace log-ins, the universal token helps identify the same user across channels and payment methods.

Ownership: Merchants keep the customer data they need for refunds, exchanges, and ongoing service — all without extra integration work.

4. Financial Products: The Embedded Finance Engine

Beyond payments processing Adyen highlighted its Embedded Financial Products (EFP) suite: Issuing, Capital, and Accounts.

Management sizes the revenue opportunity for these embedded products at €127 billion, growing at 20% annually.