In today's report, we cover Adyen. Adyen stood out from our screening in "Fresh Stock Ideas." As we already hold PayPal, we decided to take a deeper look to better understand the industry dynamics.

In this article, we provide an overview of Adyen’s business, assess the recent drop in margins, and analyze the competitive landscape, specifically comparing it with Stripe and PayPal's Braintree. We conclude this report with a DCF valuation and a sensitivity analysis.

For new subscribers: Every month we share 2 detailed company write-ups; one on an existing portfolio company and one on a potential portfolio candidate. To discover more about our offering, visit the “About StockOpine” section.

1. Key Facts

Description: Adyen N.V. (“Adyen”, “Company”), is the global financial technology platform of choice for leading businesses. It offers a single in-house developed solution that manages the entire payments lifecycle, including gateway, risk management, processing, issuing, acquiring, and settlement. Adyen supports various payment types across +100 countries.

Key Financials: Over the period FY14 to FY23, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 48.2% and operating income CAGR of 54.5%, reaching an FY23 net revenue of €1.6 billion and operating income of €681.8 million (margin of 42%). Adyen has cash and short term investments of €8.3 billion compared to nil total debt and lease liabilities of €223.1 million.

Price & Market Cap (as of 15th July 2024): Its market cap is €35.4 billion with a 52-week low of €602.8 and a 52-week high of €1,699.2, whereas it currently trades at €1,139.4.

Valuation: Adyen trades at a TTM EV/EBITDA of 35.6x (3 Year average of 61.4x) and a TTM EV/Sales of 16.8x (3 Year average of 34.7x).

2. Business Overview

a. Brief History

Adyen, meaning “start again,” was founded in 2006 by Pieter van der Does and Arnout Schuijff, marking their second startup project after Bibit (now part of Worldpay Inc.). Arnout stepped down in January 2021, while Pieter continues to serve as Co-CEO, focusing on an oversight role within the Management Board. Ingo Uytdehaage, appointed as Co-CEO in mid-2023, oversees Product Solutions and Operations, effectively succeeding Pieter. Pieter holds approximately 3% of the Company's ownership, valued at about €1.1 billion (as of July 11, 2024), while Ingo holds about 0.6%.

Since its inception as a payments platform in 2006, Adyen has transformed into a global financial technology platform. With 27 offices worldwide, it processed over €970 billion in payments in 2023, providing end-to-end capabilities (acquiring, gateway, processing, settlement, etc.), data enhancements, and financial products (issuing, FX services, PoS terminals) within a single internally built solution. Adyen effectively manages the entire payments lifecycle.

Adyen's significant expansion began in 2012 with the opening of offices in San Francisco, Paris, and London. Recent achievements include obtaining a US branch license in 2021 and acquiring licenses in regions such as Japan and UAE in 2021, and Malaysia and Puerto Rico in 2020. A milestone in its history was the IPO in June 2018, which opened at €240 per share with a €7 billion valuation. Since then, Adyen has achieved a remarkable 16.1% CAGR (until July 11, 2024), despite being lower than the Nasdaq 100. Recent volatility in the payment industry post-pandemic and the shift towards AI stocks like Nvidia explain this “underperformance.”

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

Due to its Dutch origins, Adyen's presence in EMEA is prominent, accounting for 56% of its net revenues in 2023. Meanwhile, the North America region has expanded rapidly, increasing its share of net revenues from 15% in 2019 to 26% in 2023. Today it has reach in over 100 countries and supports over 200 local currencies.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers), StockOpine Analysis

b. Customers

Since its IPO in 2018, Adyen has consistently maintained a low volume churn rate of less than 1% while in 2023, over 80% of Adyen's growth came from existing customers, reflecting the commitment to proving value upfront and expanding collaboration over time.

Customer concentration with the top 10 merchants represents 16% of revenue in 2023. No single customer accounted for more than 10% of total revenue or net revenue in 2023 and 2022. It shall be noted though, that the majority of Adyen's processed volume comes from large enterprises.

c. Segments

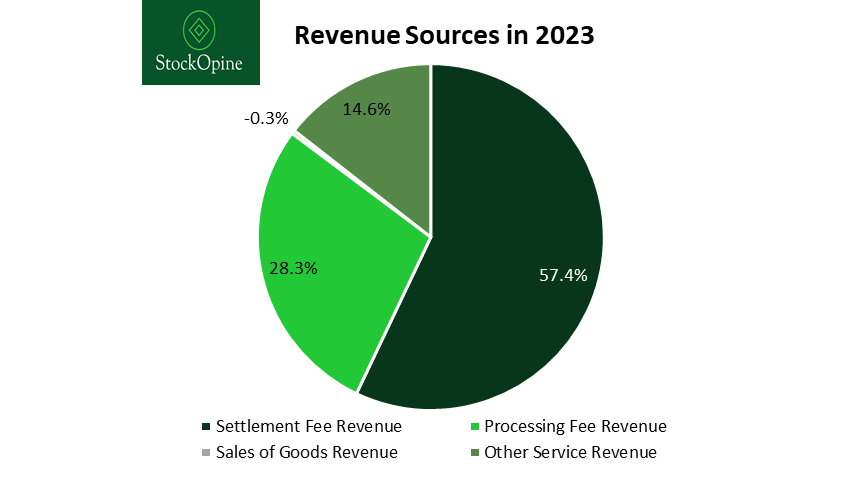

Adyen generates revenue through processing and settlement fees for its gateway and acquiring services. In 2023, revenue composition was 57% from settlement fees, 28% from processing fees, and the rest from other services, maintaining similar proportions over the past three years.

Source: Company filings, StockOpine analysis

Settlement Fees: Adyen earns settlement fees from merchants, typically as a percentage of the transaction value, for providing acquiring services. The fees include interchange and payment network fees, with Adyen charging a mark-up on its incurred costs.*

Processing Fees: Merchants pay a fixed fee per transaction (€0.11 as per its website) for using Adyen’s platform.

Sales of Goods: Revenue from selling POS terminals and accessories, distinct from Adyen's payment services. This revenue source is loss-making but crucial for building Adyen's POS business, with POS processed volume accounting for 16.5% of the total volume in 2023.

Other Services: Additional services include foreign exchange fees, third-party commissions, and issuing physical or virtual payment cards.

* In 2023, Adyen changed its approach to reporting settlement fees. Previously, Adyen was responsible for the entire settlement process and acted as a Principal. With updated terms, Adyen clarified it doesn't control third-party services for merchants. Thus, from January 1, 2023, Adyen acts as an Agent for these fees, no longer recognizing them as revenue.

Let’s now dive deeper into the 3 commercial pillars of Adyen.

Digital

Adyen's Digital segment is dedicated to facilitating effortless online payments in the digital economy. This segment is the largest within Adyen, contributing €605.5 billion in processed volume in 2023, which accounts for 62.4% of the total processed volume.

Adyen aims to be the preferred financial technology platform for enterprises, continuously evolving to meet new payment methods (screenshot below), regulations, and technologies. It addresses significant issues such as the 15% failure rate of online transactions when a card is not present and the increasing complexity of payments due to regulatory changes and shifting consumer preferences. By offering a single, integrated solution, and leveraging machine learning, Adyen helps businesses simplify these complexities (by enhancing approval rates, reduce friction, and minimize fraud) and achieve cost savings at scale.

Source: Website

These efforts have paid off, as evidenced by the chart below, showing a CAGR of 33% in volumes since 2019. The ramp-up of an existing client, CashApp, in H2 2023 significantly impacted 2023's figures. Overall, growth mainly comes from existing customers with minimal churn, demonstrating a successful land and expand strategy. The CashApp volume is also reflected in Q1 2024, where volume grew by 51% to €196.8 billion.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers), StockOpine analysis

It’s worth noting that Adyen's value proposition is not about offering the lowest price but optimizing the payment process. Adyen accounts for about 5-10% of the total payment fee and focuses on reducing overall costs for customers. For instance, at its Investor Day, Adyen announced working with a large US issuer to provide additional data from merchants, minimizing failed payments and lowering fees.

“And so a 10% reduction in Adyen fees is nothing compared to a 10% reduction in the rest of this pie. And that's where we see the value. How can we help our customers reduce their cost with this whole pie? And we've already made a lot of investments in this space. We can send additional data to the issuers to qualify for lower interchange, lower scheme fees, we do that today. We can route transactions down different alternative rails that are cheaper for our customers, we do that today.” Trevor Nies

Another point worth discussing is Adyen's extensive banking licenses, such as those in the UK and US, enabling it to offer services like issuing cards and real-time payouts, presenting an opportunity to add more volume when competitors do not offer such services. In the second half of 2023, Adyen processed over 100 million issuing volumes, up from tens of millions in 2022, demonstrating the importance of this service to merchants.

Going forward, management has identified the U.S. market as strategic for Adyen's growth. With recent investments in engineering and commercial teams, Adyen aims to increase its market share beyond the current single digits. Overall, Adyen targets global expansion as payment complexity rises.

Unified Commerce

Adyen's Unified Commerce solution powers cross-channel experiences, providing valuable data insights and advanced point-of-sale (POS) technology. As businesses worldwide increasingly digitalize, this solution bridges multiple geographies, supporting seamless in-store, digital, and in-app payments through a single platform.

“We are the only global financial technology provider that runs all channels, which is online, in-store, mobile and then app on a single end-to-end technology platform that spans across multiple geographies that is fully built in-house. No one else can do that.” Alexa von Bismarck, President EMEA

By integrating all payment channels, Adyen simplifies the payment process for merchants, allowing them to manage their payments more efficiently.

For instance, Burberry's adoption of Adyen's Unified Commerce solution led to a significant reduction in PSPs from 20 to 1 and a decrease in contracts for processing, terminals, and fleet management from 94 to 12. These changes not only streamline operations but also automate reconciliation processes, saving time and reducing overall costs.

During 2023, the Unified Commerce segment processed €253.4 billion, accounting for 26.1% of Adyen's total processed volume and showing a CAGR of 54% since 2019. Given the nature of Unified Commerce, POS volumes account for over 55% of this segment's processed volume and have been growing slightly faster than the total volume over the past three years. In Q1 2024, volumes increased by 30% with POS volumes continued to outpace eCommerce volumes.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers), StockOpine analysis

Furthermore, in Q1’24, the number of transacting Unified Commerce terminals grew to 279,000, up from 209,000 in Q1’23 and 85,000 in 2020, and the number of customers processing in multiple regions increased to 515, compared to 445 a year ago and 274 in 2020. Lastly, 333 merchants processed across channels at scale* in Q1 2024, up from 272 in Q1’23 and 100 in September 2020.

* Defined as the number of merchants processing at least €10 million on both POS and eCommerce, with over €50 million in total processed volume in the last 12 months.

Adyen has introduced Tap to Pay on iPhone in 2022, expanding to the UK, France, the Netherlands, and Australia throughout 2023, and launching in Canada in May 2024. Meanwhile, Tap to Pay on Android debuted in 2023, empowers merchants to meet the needs of emerging shopping trends where nearly a third of consumers no longer carry a physical wallet. This solution reduces hardware costs and enhances the checkout experience.

Data is also key. By capturing rich insights, Adyen enables businesses to improve customer journeys and enhance the customer experience. According to the Adyen 2024 Retail report , businesses that adopted unified commerce achieved 10% more revenue growth in 2023. Moreover, 44% reported increased customer loyalty, while 40% gained a better understanding of customer behavior for targeted marketing.

Looking ahead, Adyen is poised for significant expansion as explained below.

“if you think about the portion of point-of-sale volumes that we have compared to the way that those are set up in the world. I think we did around 17% in the second half, and that's more like 80%, 85% in the market. So I think we have a long way to go,” Ethan Tandowsky CFO

“Fast, it's our bread and butter. We run a single platform. We can really help them scale. So summarizing this up, we feel there's a huge opportunity for us out there…we feel it's a big opportunity in the countries that we already operate in, but also in new ones that we see, which are the likes of Mexico and Japan.” Gayathri Raja, SVP Product

Platforms

Adyen's Platform offering originally started with eBay but now it serves a number of marketplaces enabling SMBs businesses, to embed seamless payment capabilities across various channels and geographies. When Adyen releases new features, the marketplaces and platform businesses using these services gain real-time access, eliminating the hassle of managing payment complexities.

“It's very important for these marketplaces to be able to tell their sellers. Not only can they reach a larger, more diverse group of buyers, but they can do that by offering all the relevant local payment methods and currencies. Two, our solution is invisible by design. We take a white label approach. We stand behind the scenes.” Blake Breathitt SVP Global Head of Platforms & Financial Services

Source: Adyen’s 2023 Investor Day presentation

These businesses leverage Adyen's ecosystem, which includes embedded payment offerings and a suite of Embedded Financial Products such as business bank accounts, cash advances, and prepaid cards. By also utilizing Adyen’s unified commerce capabilities through the platform, SMBs can meet customer needs both online and in-store. The increasing usage of these unified commerce capabilities is reflected in the Platform POS processed volume, which grew from €0.2 billion in 2020 to €17.1 billion in 2023.

The total processed volumes within Adyen's Platforms segment achieved a remarkable 145% CAGR since 2019 and reaching €111.2 billion in 2023, contributing 11.5% of the total processed volume for that year. Meanwhile, Q1 2024 processed volume grew by 55%, and when excluding eBay, it grew by 116%. Although eBay initially partnered with Adyen, they chose to manage their payments independently due to strategic reasons.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers), StockOpine analysis

Adyen has also witnessed substantial increases in key metrics, such as the number of platform business customers and platforms processing over €1 billion in volume annually. By Q1 2024, the number of platform business customers surged to 96,000, up from 58,000 year-over-year. Similarly, the count of platforms processing over €1 billion in volume rose to 19, up from 17 in November 2023 during Investor Day, showing consistent growth from 7 in 2021 and 10 in 2022. This highlights the scalability and effectiveness of Adyen's platform capabilities, bringing access to customers previously unreachable.

Source: Adyen’s 2023 Investor Day presentation

“Most of those SMBs have embraced digital transformation. 80% of them are already working with platforms and platforms are helping them gain efficiency, streamline operations and keep up with the evolving needs of the user base. But only 34% today are getting their payments serviced via platforms, which presents for our platforms a pretty incredible opportunity for future growth and additional revenues.” Karolina Noronha, SVP Product, Platforms & Financial Services

This 34% is expected to reach 74% in the future proving a huge opportunity.

3. Management

a. Culture

As evidenced by Glassdoor ratings, Adyen ranks highly among its peers in overall score, CEO approval rating (the highest), and the percentage of employees willing to recommend Adyen to a friend. Although its score of 3.8 is relatively low compared to other industries, it is on the higher end within the fintech space.

Source: Glassdoor

b. Leadership

As mentioned earlier, Adyen was founded in 2006 by Pieter van der Does and Arnout Schuijff. Pieter, now 55 years old, has served as CEO since then, while Arnout stepped down from his CTO role in January 2021. Ingo Uytdehaage (51), who had been the Company’s CFO since 2011, was appointed as Co-CEO in mid-2023. Other important members of its leadership include Ethan Tandowsky, the new CFO since May 2023, who is only 34 years old but has been with Adyen for the last 7 years; Roelant Prins (49), the Chief Commercial Officer, who joined the Company in 2007; and Alexander Matthey (43), the current CTO since January 2021, who joined Adyen 9 years ago. The remaining two management members have been with Adyen for 7 and 9 years.

The leadership team has been together for a while, contributing to Adyen's significant achievements. Revenue grew from €100 million in 2015 to €1.6 billion in 2023, and processed volume increased from €32 billion to €970 billion. The stability and experience of its leadership, along with a culture of promoting from within (as seen with Ingo, Ethan, and Alexander), position the Company well for at least the next 10 years.

c. Compensation

Adyen’s remuneration for its Management Board is quite simplified. The Co-CEOs and Chief Commercial Officer (Roelant Prins) receive only a base fixed salary in cash, while the remaining members receive additional 50% of their fixed cash compensation in shares. There is also a small pension and benefits component, but no variable remuneration.

Given this simplified structure and the very low CEO pay ratio (7:1), one might assume that management could be short-term focused. However, their long tenure and the absence of annual bonus targets, which could potentially manipulate results for a larger bonus, indicate a long-term focus.

While the pay appears low, raising concerns about talent retention, the new remuneration policy (effective from 1st of January 2024) aims to position Adyen around the median of its peer group. They plan to deviate from this only in certain cases to recruit and retain top global talent. We believe that increasing compensation would make sense, especially as competition extends beyond the Netherlands, to ensure continuity.

d. Ownership

Adyen's Management Board collectively holds about 4.7% of the total outstanding shares, with Pieter van der Does owning approximately 3%, Roelant Prins owning 0.93%, and Ingo Uytdehaage owning 0.6%. We believe that this level of insider ownership is reasonable and effectively aligns management's interests with those of the shareholders.

4. Industry

The payments industry is rapidly evolving, driven by changing consumer and business needs. According to Adyen’s 2024 Retail report, 55% of consumers will abandon a purchase if they can't pay how they want, emphasizing the need for alternative payment methods and seamless, secure processes. Security remains a top concern, with 25% of consumers feeling more unsafe shopping today than 10 years ago due to fraud.

Fraud is an issue, with consumers losing 234% more money to scams in 2023 compared to the previous year, averaging $808.42 per incident. The global retail industry faced $429 billion (per Centre for Economics and Business Research) in fraud costs last year, with 45% of retail businesses experiencing cyberattacks. This underscores the need for trusted payment partners like PayPal, Adyen, and Stripe.

A growing trend in the space is social commerce, with 75% of retailers reporting revenue increases after enabling it, further highlighting the importance of a smooth checkout experience.

Omni-channel and unified commerce present a market opportunity for companies like Adyen to expand their share of wallet, as 76% of businesses lack easy cross-channel shopping capabilities.

Finally, personalized and engaging customer experiences, such as loyalty programs, are crucial, as 57% of consumers want better rewards from retailers which highlights the importance for merchants to understand shopper trends.

a. Market Size and forecasts

As per Statista, the total transaction value in the Digital Payments market is projected to reach $11.53T in 2024, up from $10.08T in 2023, and is expected to grow to $16.58T by 2028, depicting a CAGR of 10.5%. The largest segment within Digital Payments is Digital Commerce, which is projected to have a total transaction value of $7.63T in 2024, representing approximately two-thirds of the total industry.

It should be noted that this figure does not encompass the entire range of industry services, as it excludes, business-to-business payments, eBanking, payments via social networks and more.

Source: Statista

Another metric we evaluated to assess the trend of the industry was US e-commerce retail sales. Although this is a subsegment of the global industry, it is promising to observe that, on an adjusted basis, the industry has grown year-on-year by 8.6%, 10%, and 9.5% in Q1 2024, Q4 2023, and Q3 2023, respectively.

b. Competitive landscape

Although the fintech space is very crowded and includes a number of competitors like Wise, Stripe, Revolut, PayPal (and its subsidiary Braintree), Block (formerly known as Square), Fiserv, banks, and card networks (Visa, Mastercard), in this segment, we will focus on comparing Adyen to Stripe and Braintree of PayPal given their greater similarity in offering and volumes. If you wish to learn more about the fintech industry, we urge you to read this guest post written in our newsletter by our friend Dave Ahern, co-host of The Investing for Beginners Podcast.

Processed volume

Processed volume is the most important metric for these companies since its growth, especially when outpacing e-commerce growth rates, indicates that they are improving their market penetration and share of wallet. Stripe reported a 25% increase in 2023, exceeding $1 trillion in total payment volume. PayPal's Braintree (PSP) total payment volume, is estimated to have reached $520 billion, up from $400 billion in 2022, reflecting a 30% FX-neutral growth rate. Adyen has also performed strongly, achieving a processed volume of €970.1 billion with a growth rate of 26.4%. In US dollar terms, using average EUR/USD FX rates, Adyen's volume exceeded $1 trillion.

Source: Company filings, Stripe 2023 annual letter and other sources mentioned in our Decoding PayPal's Figures: Valuation and Growth Analysis report

In our view, there is no clear winner in this race as all three companies are expanding at similar levels. In contrast, Block appears to be falling behind, with a gross payment volume of $227.8 billion in 2023 and a year-on-year increase of just 12%.

In the most recent quarter (Q1 2024), Adyen reported a 46% year-on-year increase, while PayPal reported a 26% increase for its P2P segment. This deviation is partly due to CashApp, a digital customer of Adyen, which expanded in H2 2023.

Return on Invested Capital

There are no available metrics for Stripe to assess it comprehensively, but in 2022, it was loss-making, and in 2023, according to unconfirmed sources, it was marginally profitable in terms of EBITDA. On the other hand, Adyen has been leading the pack with the highest returns on invested capital (“ROIC”), with PayPal closely trailing. However, Adyen’s ROIC has been on a declining trend.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

The key reason for Adyen’s decline was the drop in net operating profit after tax (“NOPAT”), with the main detractor being income tax expense, which grew by 57% while operating income was relatively flat in 2023 (from €665 million to €682 million). Meanwhile, its average invested capital grew at a fast rate as the Company does not repurchase shares or pay a dividend. In contrast, PayPal improved its operating profit by 20%, with tax expenses increasing proportionately by 23%. With an aggressive share buyback policy ($5.3 billion in 2023), its invested capital marginally increased, allowing PayPal to maintain its returns on capital.

By examining the details, we don’t view Adyen’s decline as concerning, as there are reasons justifying the drop. For starters, the Company is in an investment phase and completed its 2-year employee investment program in 2023, which required retaining cash to support these investments. Additionally, the effective tax rate increased from 21.6% in 2022 to 25.9% in 2023, negatively affected by adjustments relating to 2022, certain non-deductible expenses, and finance income that does not benefit from the innovation tax box regime of the Netherlands but still added €246.4 million before taxes to its net profitability.

Achievements

Adyen was recently recognized as a Leader in the IDC MarketScapes for Worldwide Retail Online Payment Platform Software Providers and Worldwide Retail Omnichannel Payment Platform Software Providers. The following strengths were identified: a comprehensive solution, innovation, and a focus on merchants.

Source: IDC

Additionally, in Forrester's Q1 2024 Merchant Payment Provider report, Adyen was recognized as a 'Strong Performer,' performing on par with Stripe and better than PayPal. Notably, Adyen achieved the highest possible score (5) in categories such as vision, innovation, payment performance optimization, omnichannel payments, POS terminals, and payment data enrichment. Forrester commented, “Adyen is a best fit for merchants looking to consolidate on one partner for their omnichannel customer journeys….”

Other notable scores from the report include:

Innovation: Adyen, PayPal, and Stripe each scored a 5.

Customer Support: PayPal and Stripe scored a 3, while Adyen scored a 1.

Authentication: Checkout.com scored a 5, outperforming the rest.

Fraud and Risk: PayPal scored a 5, surpassing Stripe and Adyen, both of which scored a 3.

Source: Forrester, The Forrester Wave™: Merchant Payment Providers, Q1 2024

Similar to the findings on processed volume, we can conclude that Stripe and Adyen are leading, with PayPal trying to catch up.

5. Financial Analysis

a. Performance

Over the period FY14 to FY23, Adyen depicted a revenue CAGR of 48.2% and operating income CAGR of 54.5%, reaching a TTM revenue of €1.6 billion and operating income of €681.8 million (42% operating margin). The free cash flow margin (“FCF”) averaged 45.3% from FY15 to FY23, while 2023 FCF reached €639.5 million, translating to a FCF margin of 39.3%.

Source: Koyfin (affiliate link with a 15% discount for StockOpine readers), StockOpine analysis

As mentioned earlier, the key driver of Adyen's revenue growth has been its "land and expand" strategy, where the Company increases its share of wallet after signing new partners. Alongside revenues, operating profits grew at similar pace until 2021, but thereafter there was pressure on operating margins.

This stemmed from Adyen's increased investment in commercial and engineering teams over the past couple of years. Employee expenses accounting for 59% of total operating expenses in 2021 and growing by 58% in 2022 and 56% in 2023, outpaced revenue growth by 25.4% and 33.8%, respectively, pushing margins down. Consequently, EBITDA margin fell from 63% in 2021 to 45.7% in 2023.

As Adyen slowed its hiring pace in Q1 2024, metrics per employee are expected to improve, contributing to better margins.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Similarly, FCF moves in tandem with operating margin and EBITDA, with FCF conversion averaging 88.4% over the last five years and 86.1% in 2023, indicating high-quality earnings. Although not shown in the chart above, net margin remained stable at 42.9% compared to 42.4% in 2022, despite an 800 basis point drop in operating margin. This was impacted by net interest income contributing 15% of sales in 2023!

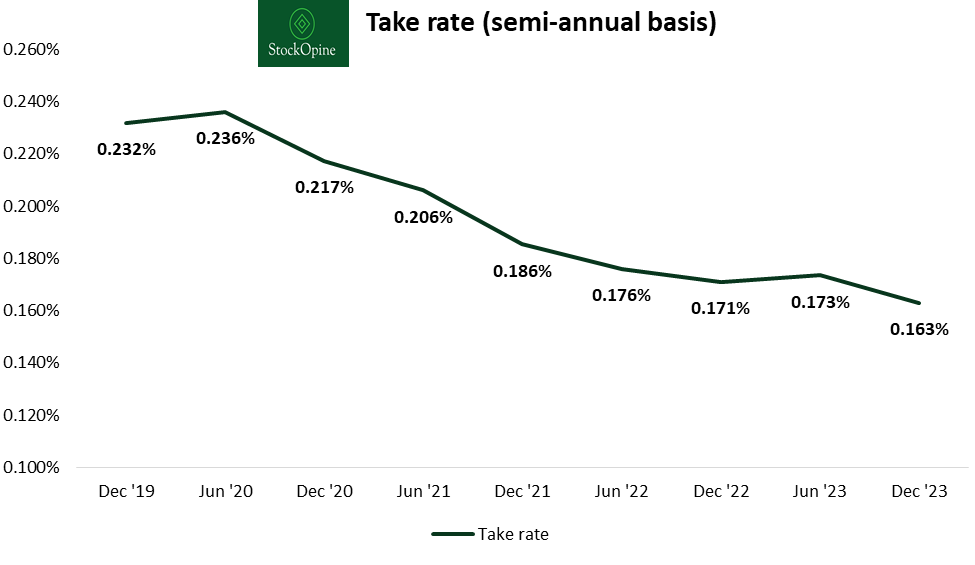

Take rate

There is a lot of talk among investors about Adyen's declining take rate, but this is not a sign of weakness. Adyen uses a tiered pricing model, where pricing per volume declines as volume increases. Nevertheless, the cost to support this volume is minimal since the same single platform is used.

Source: Company filings, StockOpine analysis

b. Financial position

In terms of its financial position, the Company holds cash and short term investments of €8.3 billion with no debt and €223.1 million in lease liabilities. This results in one of the healthiest balance sheets in the industry, allowing Adyen to maintain an industry-leading credit rating so as to comply with regulators, and leverage its banking licenses.

It should be noted, however, that a net amount of €5.5 billion relates to net payables to merchants and financial institutions. Therefore, we consider the cash available to Adyen to be approximately €2.8 billion.

c. Capital allocation

A straightforward policy focusing on reinvestment to grow the business is best explained by the following quote:

“We want to be able to continue to invest in our growth. And consistent with the approach that we've taken since our foundation, we have plans to continue to reinvest in the business rather than issuing dividends or doing share buybacks. A big reason for that is also to maintain the flexibility that we have in our business and the relationships we have with our regulators and in keeping an industry-leading credit rating that we have with S&P.” Ethan Tandowsky, CFO

Source: Adyen’s 2023 Investor Day presentation

d. Outlook

Market Share Growth

Currently, Adyen accounts for a small percentage of market share even in its most commercially established regions.

Significant untapped potential exists in high-growth regions like the US and in nascent countries such as Brazil, Japan, and India.

Continued support for Chinese brands wishing to sell internationally, presenting ongoing opportunities.

Net Revenue Growth

Aim to grow net revenue annually between the low twenties and high-twenties percent through 2026. For 2024, it is expected to be at the lower end.

Growth will be driven by market volume increases, share of wallet gains, and new wins, offset by a tiered pricing model.

Source: Adyen’s 2023 Investor Day presentation

EBITDA Margin

Target to improve EBITDA margin to above 50% by 2026.

Benefits expected from operating leverage inherent to the business model, slowing hiring rates, and limited investment requirements for platform maintenance.

Quote from Ethan: “So the ability to run a lean team and a lean company, small teams who make a big impact, we feel strongly we can execute on. That means that as the business grows, the team doesn't have to grow in tandem.”

Capital Expenditure

Aim to maintain sustainable capital expenditure levels of up to 5% of net revenue.

6. Competitive Advantages, Opportunities and Risks

Competitive Advantages

Own build platform: Adyen's internally developed platform provides flexibility for rapid adaptation to new regulation and innovation, ensuring ongoing relevance and compliance. Operating under a single platform allows Adyen to seamlessly offer capabilities to customers without transferring the administrative burden to them (think of transferring the capabilities from one commercial pillar to another, such as unified commerce on platforms). Additionally, as revenue grows, operating leverage benefits kick in since platform maintenance costs do not increase proportionally.

Trusted Solution: Adyen holds acquiring and banking licenses globally, instilling trust among merchants and customers in an environment increasingly threatened by fraud and cyberattacks.

Partnerships with Global Payment Methods: Adyen integrates with a wide array of payment methods, aligning with trends where younger generations prefer alternative payment methods. This broad integration enhances conversion rates for merchants.

Pricing Model: Adyen's cost relative to the total transaction fee is minimal, yet its service remains critical in complex payment transactions. Its tiered pricing model enables merchants to expand their share of wallet with Adyen while minimizing cost concerns.

Opportunities

Digital Payments Market Growth: Despite the risk of payments becoming commoditized, the market is projected to grow by 10.5% over the next few years. Given Adyen’s leading position, it is poised to outpace this growth rate.

Platforms: Adyen offers its technology as a white-label solution to platforms, allowing them to integrate payment services under their own brand for SMB customers. This strategy helps Adyen access new customers and expand its Total Addressable Market. With only 34% of SMBs getting their payments serviced via platforms, the growth opportunity is substantial.

Global Expansion: Adyen is increasing its market share in North America, while Latin America and the Asia Pacific regions remain under-penetrated markets with significant growth potential.

Risks

Commoditization of Payments: While acknowledging the risk of commoditization, we believe it will have limited impact on Adyen. The essential nature of its services suggests that its take rate, currently at 0.16%, is unlikely to approach zero. Despite fierce competition and increasing regulation, Adyen benefits from its strong market position. Moreover, add-on services such as FX, issuing, risk management, and data insights enhance the Company's overall offering and simplify operations for merchants.

Management Changes: The management team at Adyen has demonstrated stability with years of collective experience. While succession planning, particularly when Pieter van der Does steps down, may introduce some turbulence, the appointment of Ingo Uytdehaage as Co-CEO since mid-2023 helps mitigate this risk to some extent.

7. Valuation

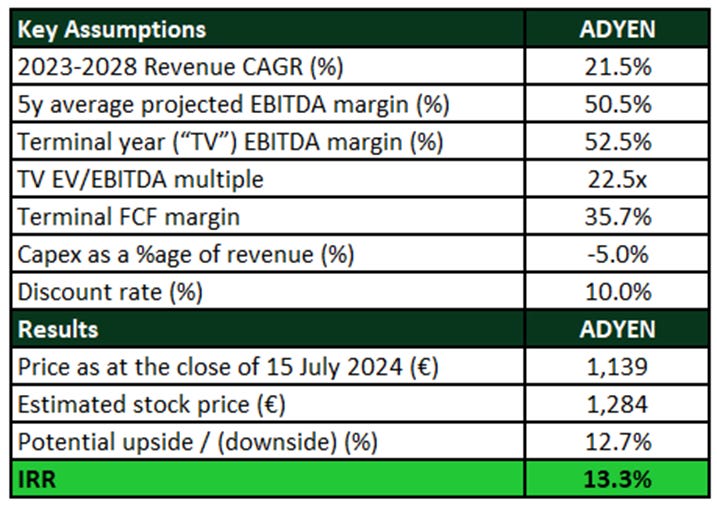

The stock price as of 15th of July 2024 stands at €1,139 with a 1-year return of -23%. The Company's market capitalization is €35.4 billion and it trades at an EV/EBITDA TTM multiple of 35.6x. Based on our DCF valuation, the estimated price of Adyen is €1,284, ~13% higher than its current price, and an expected IRR over the projected period of 13.3%.

Source: StockOpine analysis

To estimate the fair value of Adyen, we have projected a revenue CAGR of 21.5%, reaching sales of €4.3 billion by FY28. This aligns with management's guidance of low to high twenties net revenue growth for 2024-2026. Anticipating lower take rates as volume increases, we assume a take rate of 0.14% by 2028, implying a processed volume CAGR of 25.9% from 2023 to 2028, reaching €3 trillion in processed volumes.

Regarding profitability, we applied an average EBITDA margin of 50.5% and a terminal margin of 52.5%. Although this is lower than the 5-year average of 56.3%, it is higher than the 2023 margin of 46%. Given that Adyen has completed its investment plan and slowed down hiring, we believe margins can return to historical levels, thus we applied a gradual increase. Management also expects to reach EBITDA margins above 50% by 2026.

To derive free cash flows to the firm, we deducted projected Capex requirements of 5.0% of revenue, which is in line with the 5-year average of 4.8% and the long-term target set by management of up to 5% of net revenue. Factoring in taxes and working capital needs, our analysis results in a terminal FCF margin of 35.7%, lower than the 5-year average of 49.9%. Adyen's reported FCF does not include tax paid, inflating the figure. Adjusting for taxes, the historical 5-year average FCF margin is 39%.

For the terminal EV/EBITDA multiple, we assumed a multiple of 22.5x, significantly lower than the 3-year average of 61.4x and the TTM of 35.6x. Adyen plays a prominent role in the payment ecosystem, evidenced by its high returns on capital. Considering that Adyen reinvests heavily into the business, a multiple of 22.5x is reasonable. Comparatively, durable companies like Visa and Mastercard have 5-year averages of 25.4x and 31x, respectively, indicating that our assumption is not overly optimistic.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on these calculations and assumptions (which may not materialize), we estimate a value per share of €1,284, which is 12.7% above the current price, resulting in an IRR of 13.3% over the projected period.

a. Sensitivity analysis

The below tables give an indication of the potential upside/(downside) compared to the current price (€1,139 as of 15th Julyl 2024) when a) the terminal EBITDA multiple and the discount rate are changed and b) the terminal EBITDA multiple and EBITDA margin are changed.

Source: StockOpine analysis

b. A different perspective on valuation

Companies like PayPal and Adyen have seen declines in market value, with PayPal down 14.7% and Adyen down 22.6% over the past year (until July 14, 2024). In contrast, Stripe in April raised $694.2 million to enhance liquidity for existing and former employees, valuing the company at $65 billion—a 30% increase from last year's $50 billion valuation. Most recently, it was reported that Sequoia Capital offered Stripe investors a share deal valued at $70 billion.

Considering Adyen's comparable processed volume to Stripe, strong profitability, and robust returns on capital, it's perplexing how Adyen is valued at €35.4 billion (~$38.6 billion). Similarly, PayPal's valuation at $63 billion (as of July 12, 2024) seems low compared to Stripe, especially since Braintree processes less than half the volume of PayPal’s total volume and it is a payment platform with very low take rate compared to its branded checkout.

The market valuation disparity between Stripe and Adyen/PayPal suggests a misalignment in market perceptions. While the truth likely lies somewhere in between, we lean towards questioning the valuation of Stripe and believe that Adyen and PayPal may have upside potential.

8. Conclusion

Adyen stands out in the fintech industry. Its single platform allows for rapid innovation and lower maintenance costs, while global acquiring and banking licenses build trust among merchants. Partnerships with global payment methods and a tiered pricing model further enhance its appeal.

The Company has substantial growth opportunities in the US, Brazil, and Asia Pacific. It’s financially strong with significant cash reserves and no debt, while it has industry-leading margins and high returns on capital.

Risks include potential commoditization of payments and management changes, though the latter is mitigated by the appointment of Ingo Uytdehaage as Co-CEO since mid-2023.

Adyen ticks many quality boxes: high margins, impressive returns on capital, significant insider ownership, and a long-tenured management team. It also trades at an attractive valuation, presenting a strong investment case.

Although we hold PayPal, another strong player in the space, we will open a 2% position in Adyen tomorrow provided the price does not exceed €1,190. It has been a long time since we last identified such a quality company, and we can’t remain on the sidelines. In the coming days, we will also release an investment thesis for those who prefer a shorter read.

Great analysis, but I'd like to add some insights that in my opinion were left out, but are vital to Adyen. I shared it in my own deep dive, I hope its fine if I link to it here( https://heavymoatinvestments.substack.com/p/adyen-adyey-powering-global-commerce). I can't post a picture in the comments, but the vital part missing is that Adyen does NOT primarily compete with Stripe and Braintree. To quote my article: "Stripe is focused on SMBs, like this blog you are reading right now. Adyen, on the other hand, focuses on multinationals with global operations. Braintree is owned by PayPal and thus is biased towards PayPal solutions.". Furthermore these modern acquirers only hold around a 10% share in the total payments processing market, with 90% in the hands of legacy players who are losing market share. The real opportunity is not in competiting with Stripe and braintree, but in taking share off legacy players that can't offer what modern, digital businesses need.