ASML Q3 2025: Navigating China Dynamics & Pushing Tech Boundaries

A closer look at the key technological leaps in High-NA EUV, a strategic entry into 3D integration, and a pivotal partnership in AI.

ASML reported a solid quarter, driven by robust demand for its advanced lithography systems. Its results and outlook reflect broader trends in AI, which are supporting long-term secular growth in advanced logic and DRAM investments.

a. Results: Steady Performance and Shifting Dynamics

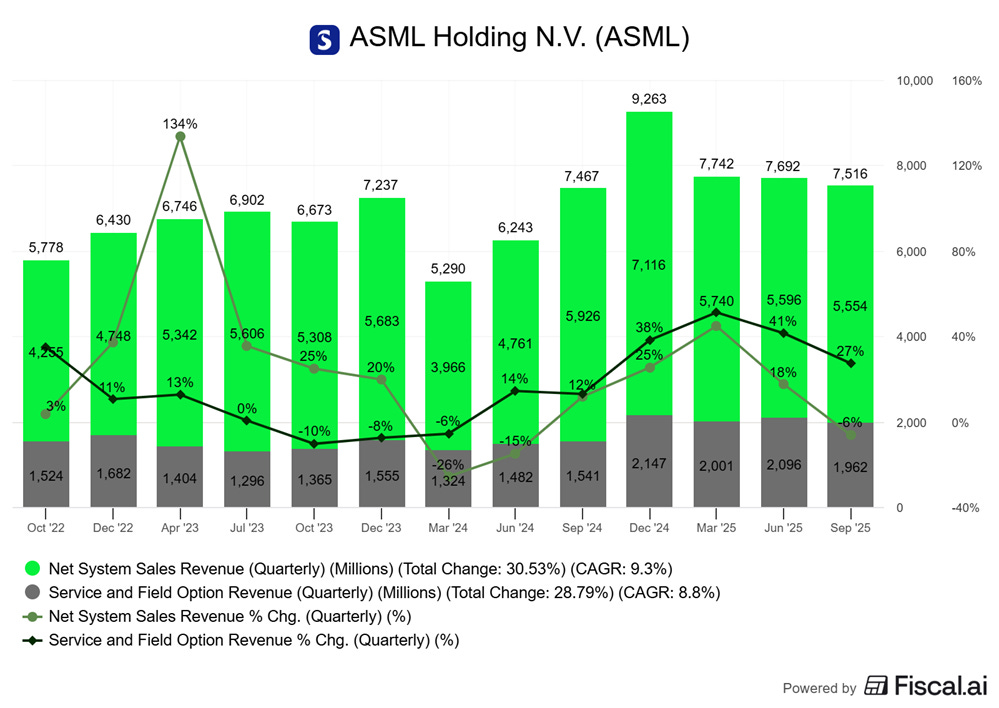

ASML delivered Q3 2025 net sales of €7.5 billion, a slight increase of 0.7% year-over-year, within the company’s guided range. The Installed Base Management segment, which includes service and field option sales, contributed a strong €2.0 billion, up 27% year-over-year, reflecting the expanding and increasingly essential fleet of ASML’s lithography systems in operation.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

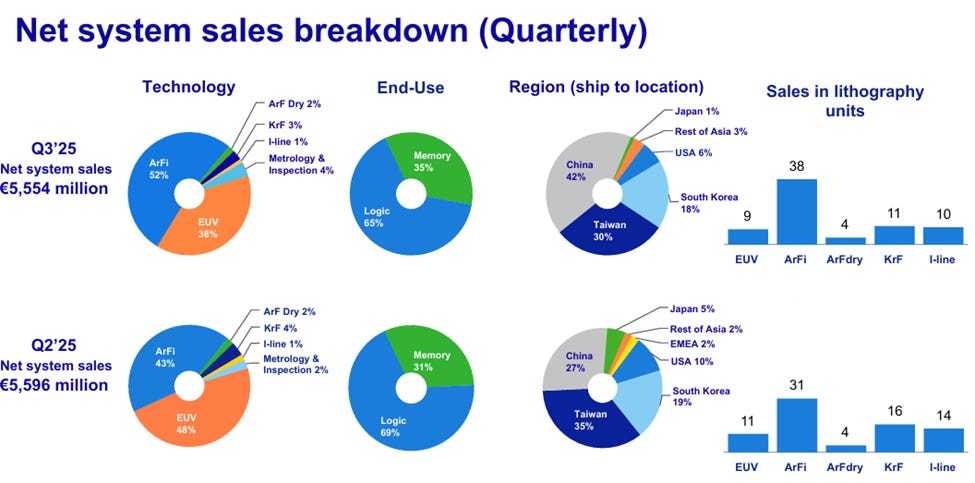

Net system sales for the quarter stood at €5.6 billion. A closer look at the technology mix reveals that ArFi (immersion) systems accounted for 52% of system sales, while EUV systems made up 38%. From an end-use perspective, the memory segment showed an increase, constituting 35% of net system sales, up from 31% in the prior quarter.

Source: Q3’2025 earnings presentation

Geographically, China was a significant contributor, accounting for 42% of system sales in the quarter, a substantial increase from the 27% seen in the previous quarter. That being said, management noted that this reflects shipments against a large backlog from prior years and expects demand from China to normalize at a lower level in 2026.

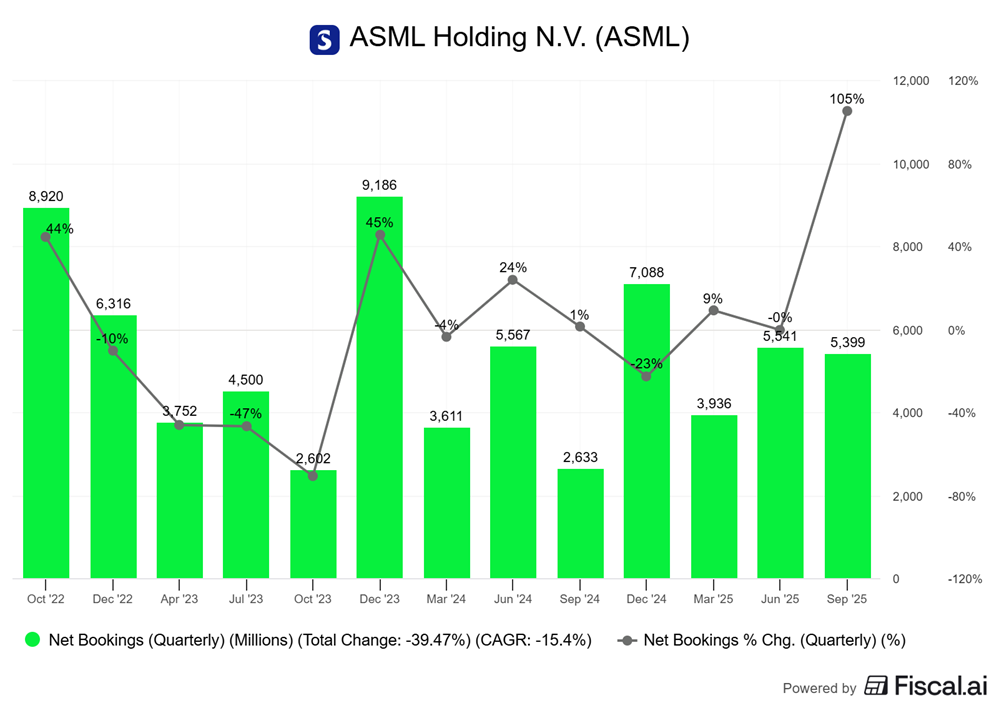

Total net bookings were strong at €5.4 billion, a YoY increase of 105%, with €3.6 billion of that for EUV systems, signaling continued customer commitment to the most advanced nodes. That being said, bookings are lumpy in nature and should be treated with caution and over time.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The gross margin for the quarter was 51.6%, at the higher end of the guidance and an improvement from 50.8% in the prior year, though slightly down from the 53.7% achieved in Q2 2025. The fluctuation in gross margin reflects the complex interplay of product mix, with the initial low-margin High-NA systems having a dilutive effect, while the established EUV and upgrade business provide a positive contribution.

Net income came in at a healthy €2.1 billion, or 28.3% of sales demonstrating the strong profitability even as it invests heavily in future technologies.

b. Outlook: Strong Finish to the Year

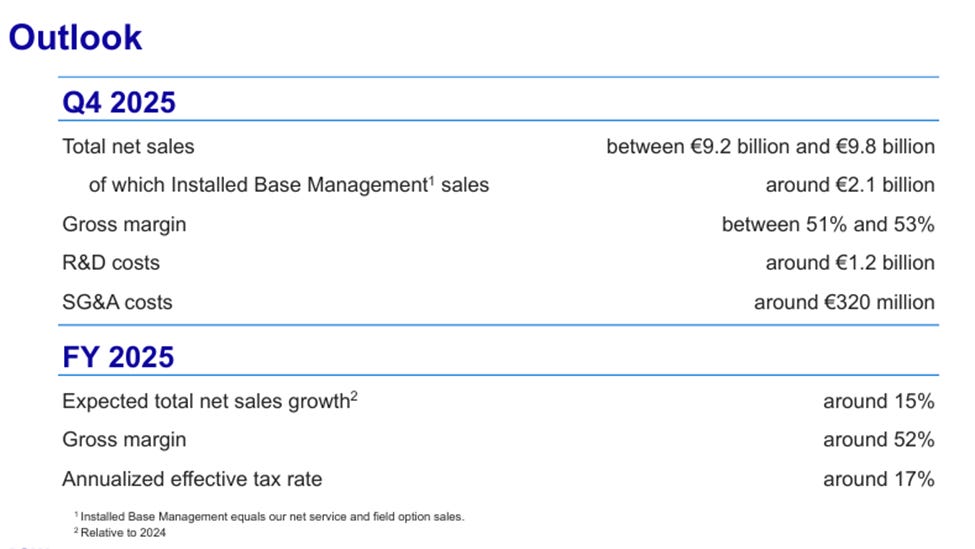

ASML projects total net sales between €9.2 billion and €9.8 billion indicating a strong end to the year, a pattern also observed in 2024. Installed Base Management sales are expected to be around €2.1 billion.

The gross margin is estimated within 51% and 53%, a slight improvement at the midpoint compared to Q3. This strong Q4 performance would bring the full-year 2025 total net sales to approximately €32.5 billion, with a growth of around 15% over 2024, with a full-year gross margin of about 52%.

Source: ASML Q3’2025 earnings presentation

Looking ahead to 2026, the company expects net sales to be at least at the level of 2025. This balances two opposing trends: an expected increase in EUV sales driven by both logic and DRAM customers, and a decrease in DUV sales to China as the current backlog is worked through.

The long-term outlook remains positive. As CEO Christophe Fouquet stated,

“there has been a positive news flow across the industry in recent months that has helped to reduce the level of uncertainty that we were reporting last quarter.”

The continued massive investments in AI infrastructure support a favorable outlook for ASML, although the timing of their impact on bookings and revenue remains uncertain. What is certain is that these large-scale investments at advanced nodes rely on ASML’s machinery.

Today, industry validation came from TSMC, which reported Q3 revenues up 30% YoY, with 74% of wafer revenue from 7nm and below technologies (60% from =<5nm), where EUV is essential for advanced chips. TSMC’s 2025 CapEx guidance midpoint was increased to $41B, up from $40B last quarter, with 70% allocated to advanced process technologies while they indicated that CAPEX is unlikely to decline in any year and will continue to grow as long as high-revenue opportunities exist.

In short, there is no signal of slowing demand, and strong industry trends suggest ASML is well-positioned to benefit from ongoing AI-driven growth in semiconductors.

c. Technology: Pushing the Boundaries of Physics

ASML’s technological leadership is the cornerstone of its success, and these are the recent developments.

*For investors looking for more context and insights, here’s our full deep dive into ASML.