Evaluating the Strengths and Challenges of POOL Corporation

This month, we are revisiting Pool Corporation ("POOL", "Company") to examine the performance and developments of 2023. During this period, POOL experienced a 10.7% decline in sales and a drop of 27.4% in operating income, pushing operating margin from 18.1% in 9M 2022 down to 14.7% in 9M 2023. The impact of rising interest rates on consumer confidence and, consequently, the dollars spent on new construction and remodeling affected both sales and margins.

Subsequently, we will assess the outlook and industry dynamics, comparing Heritage Pool Supply to POOL and evaluate how Pinch A Penny performed relative to Leslie’s. Our article will be concluded with a revised Discounted Cash Flow (“DCF”) valuation.

If you are interested to learn more about POOL, we suggest that you read our prior (free) article (Pool Corporation - Write up).

Contents:

1. Brief introduction

2. The present and the future

3. Industry

4. Valuation

5. Conclusion

1. Brief introduction

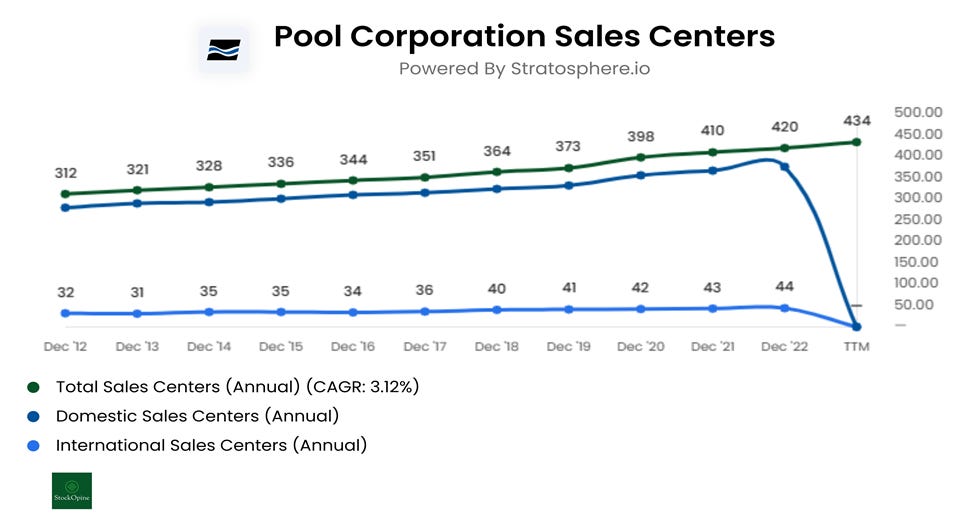

Pool Corporation is the world's largest wholesale distributor of swimming pool supplies by a wide margin. It operates 434 sales centers (as of its latest filing) and serves +125,000 professional contractors and retail customers across North America, Europe, and Australia. It offers a broad range of +200,000 products, sourced from over 2,200 suppliers, demonstrating the resilience of its supply chain.

POOL maintains a significant presence in pool-dense regions like California (77 locations as of 31/12/2022), Texas (55 locations as of 31/12/2022), Florida (62 locations as of 31/12/2022), and Arizona (26 locations as of 31/12/2022). The Company consistently expands its network of sales centers, strengthening its position as the undisputable leader in the pool and outdoor living industry.

Source: Stratosphere.io (use coupon code STOCKOPINE for a 25% discount), Note: No breakdown is provided in quarterly filings

It is estimated that out of the 10.4 million US residential swimming pools, Florida has the highest number at 1.59 million, followed by California at 1.34 million, Texas at 801,000 and Arizona at 505,000. This data displays POOL’s strategic positioning of its sales centers. It’s also worth noting, that over 85% of the Pinch A Penny stores (a specialty retailer of pool related products operating under a franchise model and was acquired in 2021) are located in Florida.

Since 2012, it achieved a remarkable growth of 10.4% Revenue Compound Annual Growth Rate (“CAGR”) until 9M 2023 and an Operating Income CAGR of 16.4%, with the operating margin growing from 7.8% in 2012 to 13.8% on a trailing twelve month (“TTM”) basis. As of November 3, 2023, POOL's market capitalization is ~$13.0 billion, with a stock price of $336.7 (a 13.5% decline from its 52-week high) and a forward dividend yield of 1.34%.

POOL's operating model is resilient, as its revenue composition in 2022 is comprised of 61% non-discretionary maintenance and repair products, 22% somewhat discretionary renovation and remodel products and equipment, and 17% discretionary new pool construction-related products. Meanwhile, ~95% of its net sales are derived from North America.

Source: Pool’s Q3’23 earnings presentation

Peter Arvan has been at the helm of POOL as CEO since FY19. Under his leadership, sales have surged from ~$3 billion in 2018 to around $5.6 billion on a TTM basis while the operating margin has improved by ~330 basis points. Management exhibits a long-term mindset, as underscored by a statement from its CEO Peter Arvan.

“So we tend to be very long-term focused on our investments and deliver it with where we're investing capital on recognizing that sometimes you spend money this year to reap rewards next year or the year after or the year after. But I think if you look back historically on the investments that POOLCORP has made, that's one of the things that has allowed us to continue to grow and to continue to expand the operating leverage.”

2. The present and the future

a. Financial Performance in 2023

Revenues

In 2023, POOL encountered challenges affecting its financial performance primarily due to the impact of a high interest rate environment on new construction and remodeling projects. Additionally, adverse weather conditions accounted for a ~2% negative impact. Year to date (“YTD”) sales were down by 11% driven by notable declines in sales of equipment by 10% (accounts for 29% of sales) and building materials by 9% (13% of sales). These declines were tied to the slowdown in new-pool construction (down by ~30%) and remodeling and renovation projects (down by 10%-15%). Per management, building materials boast higher margins, therefore, beyond the overall operating deleverage impact, the change in mix played a role in driving operating margins from 18.1% in 9M 2022 YTD to 14.7% for 2023 YTD.

Source: Koyfin (affiliate link with a 15% discount for StockOpine readers), StockOpine Analysis

In the most recent quarter, the Company saw a 9% decrease in sales primarily attributed to a 5% drop in new pool construction, a 3% decrease in renovation and remodel projects, while other factors contributed to the remaining 1% decline. On a positive note, chemical sales which account for 13% of sales, were up by 5% due to increased volume, resulting to a deceleration in the declining trend. This performance was achieved despite deflationary pressures from trichlor pricing (down by ~20%) which currently shows signs of stabilization. Looking ahead to Q4’23, the expectation is for a mid-high single-digit decline in sales and a 10% decline for 2023.

Before we move into the profitability metrics, let's address the concern about pricing deflation. Should we anticipate a broad-based price reset? Most likely, that is a NO. Historically, when prices have increased, they rarely return to their previous levels, as such the risk of price deflation appears low. Additionally, vendors have announced a 3%-4% price increases for next season. Needless to mention, but Peter Arvan, CEO indicated that he doesn’t expect (“In fact, I think there's virtually zero chance of that, in my opinion.”) equipment prices to come down as the equipment set accounts for $15,000 or ~23% of the average swimming pool cost ($66,500) in 2022. Consequently, a change in price is unlikely to impact a homeowner's decision to build or renovate a pool.

Moreover, Leslie’s estimates that on average a pool owner spends annually $900 on chemicals, equipment, parts, and accessories necessary to maintain their pools. This amount approximates to 1.5% of the average US salary, which is a negligible percentage to influence a homeowner’s decision in maintaining their pool.