Evolution AB – A ‘sin’ stock with healthy returns

Every month we share 2-3 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analyzed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

At the end of each write-up, we will state whether we decided to buy the stock or not. If not, keep an eye to our Quarterly Portfolio Update releases in which we will update you for all the transactions that took place during the latest quarter.

In this release we cover Evolution AB (Ticker: $EVO.ST, $EVVTY), a world-leading provider of online live casino solutions.

1. Key Facts

Description: Evolution AB (“EVO”, “Evolution”, and “Company”) was founded in 2006 and develops, produces, markets, and licenses live casino and slot solutions to gaming operators. EVO employs c. 16,000 people and has over 600 customers.

Key Financials: Over the period 2012 to 9M 2022, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 47.1% and operating income CAGR of 58.6%, reaching a Trailing Twelve Month (“TTM”, “LTM”) revenue of c. $1.35B and an operating income of $0.84B (LTM margin of 62.4%). EVO has a healthy balance sheet with Cash and Short term investments of $320M compared to lease liabilities of $69M (nil debt).

Market Cap (as of 12th December 2022): Its market cap is SEK 228B with a 52-week high of SEK 1,323 and a 52-week low of SEK 779.7, whereas it currently trades at SEK 1,069.4, a 19.2% decline from its 52-week high.

Insiders: Österbahr Ventures AB jointly owned by Jens Von Bahr (Co-founder and Chairman of the Board) and Fredrik Österberg (Co-founder and Board Member) holds 10.7%.

Valuation: EVO trades at an EV/EBITDA of 22.1x (7 Year average of 33.5x) and at a TTM P/E of 27.1x (7 Year average of 42.2x).

2. Business Overview

Business model

Evolution develops, produces, markets and licenses fully integrated online and live casino solutions to gaming operators (B2B basis) which then market the products to their end users. Except gaming operators the other type of customers are land-based casinos which expanded online as well as Gaming Aggregators like SoftSwiss and SoftGamings. Game aggregators are effectively a single hub of games from various online gaming providers (like EVO) thus offering a single API to operators.

EVO Live Casino -> Gaming Aggregators (not always necessary) -> Gaming Operator (could be a land-based casino) -> End User

EVO receives revenue from monthly commission fees , i.e. a percentage of the operator’s profit generated from using Evolution casino platform (end user lost a bet of €10, operator gets €10-x, Evolution gets x) and fixed fees from dedicated tables as well as other fees such as set-up fees.

For the basic agreements the streaming is done from generic tables while for dedicated tables the streaming is done from exclusive, customized tables reserved for the operator. Generic tables are used by any operator while dedicated tables are unique, customized to operator’s requirements regarding studio environment, brand, graphics, and language and are used exclusively by the specific operator for its end users helping them differentiate from competitors. The fee structure allows the company to gain real exposure to the Live Casino Market which is expected to grow by more than 20% CAGR in the next 5-10 years.

Evolution is licensed and regulated for its brands; Evolution, NetEnt (acquired in 2020), Red Tiger (was acquired by NetEnt), Ezugi (acquired in 2019), Big Time Gaming, “BTG” (acquired in 2021) and Nolimit City, “Nolimit” (acquired in 2022).

Players need exciting games, unique experience, support, high/reasonable Return to Player (“RTP”) and foremost fair gaming. When properly licensed as it seems to be the case for Evolution (we are not legal experts but we didn’t observe any negative findings / accusations except what we mention in Regulatory Risks) one can assume that Evolution provides fair gaming.

Revenue streams

The Company breaks its revenue into two categories, namely, Live and RNG with Live accounting for 79% of its revenue in 2021 and 81% for the 9M 2022. In the latest quarter, EVO revenue grew by 37% year-on-year (“y/y”), with the key driver being Live (45%) since RNG only grew by 11% (including Nolimit City acquisition) or 2% organically.

The growth in RNG is slower than what was initially anticipated due to releasing less new games than planned but management remains committed to the target of double-digit growth.

Live Casino: As per Todd Haushalter CPO, Live Casino is unique and is preferred to electronic version due to trust (seeing the dealer) and the social aspect (chat with the dealer and each other), whereas it is preferred to land-based as people can get better bets online. For instance, online roulette has a 2.7% house edge (house advantage that the house has on beating players) (single 0 only - European) whereas land-based casinos in US run at a 5.26% (0 and 00). Online slots run at around 5% house edge where in the main casino floors these have a c.15% house edge.

Live game shows are like TV shows which are entertaining and along with the opportunity to bet small and win big (well above the 1.5x in Blackjack or Roulette of 35x) is what makes them popular among players. For instance, Lightning Roulette (became the biggest Live Roulette table in the world) can go up to 500x, Lightning Dice to 1000x, Crazy Time to 25,000x, Cash or Crash to 50,000x etc. Certain game shows embed advanced RNG gameplay.

RNG: Random Number Generator games in which the outcome is determined by algorithms to ensure that combinations are 100% random (thus fair). People can bet behind the screen and enjoy their privacy, but if they want to ‘GO LIVE’ or never heard of Live Casino, EVO has the solution with its First Person games in which players with a single button can be transferred to and experience the Live Casino gaming. RNG offering is complemented by NetEnt and Red Tiger RNG table games and NetEnt, Red Tiger, Big Time Gaming and Nolimit City innovative slot games.

Brands and Innovation

The key brands are Evolution (wide range of classic table games and range of variants) and Ezugi (localised content and lottery style games) for live casino games, NetEnt, Red Tiger, Big Time Gaming and Nolimit City for the very best online slots as well as DigiWheel, the world’s first patented HD spinning gaming wheels.

Innovation at Evolution is remarkable with a unique game portfolio and a continuous introduction of new games. In 2021, 10 new live games and 59 new slots games were introduced whereas the plan for 2022 was to release a total of 88 (around 60 released already) new games across all categories (new games or new takes on players favourites).

Studios

Evolution is live across the world and operates through 15 studios (own estimate based on annual report 2021 and press releases) whereas at the end of 2021 it had over 1,000 live tables, an increase of 300 compared to 2020.

“This was a dramatic expansion reflecting our way of securing and taking market share”, Martin Carlesund, Group CEO.

Three out of the fifteen studios (Latvia, Malta, Georgia) serve as production hubs where the games are developed, tested and launched.

Increasing the number of studios drives business growth and as Evolution manages to enter new markets early it can benefit from a first mover advantage. For instance, the most notable recent launches of studios are in New Jersey (over $1B market) on 10th Nov, 2022 (2nd in New Jersey and 5th in US) and Connecticut on 18th Jul, 2022 (4th in US) while it also went live on West Virginia on 28th Jun, 2022 and Ontario – Canada on 4th April, 2022.

The studios are run by dealers who as disclosed by Todd Haushaulter, CPO on a recent GBB podcast are not former dealers as the time schedule is demanding (24/7, 3 shifts) and they mostly hire early graduates or students that may want to work. “Youth is where you find a lot of people”. These people go through an extensive 3-week program in the Academy to turn into highly productive game presenters. The fast pace of growth, the demanding job requirements along with the age of staff may explain the generally low Glassdoor score (Management & Culture section).

In our opinion, the low score (3.5*) makes sense as the majority of EVO employees are game presenters who might be young and see EVO as a starting step in their careers or just a way to earn extra income whereas management knows that these people can be easily replaced (i.e. with a 3-week training and 3 months of trainee period).

Geographies

Europe is the largest market of Evolution accounting for 39% of 2021 revenue, with Asia region and North America being next with revenue shares of 27% and 11%, respectively. Management sees a growth potential in North America which justifies the investments made as of today in US whereas in Asia, EVO considers itself as a ‘small actor’ with attractive opportunities.

“I would say that we're still small in Asia. Asia is a huge market….And then there's simply many more players in Asia than in Europe because it's a larger population.” Martin Carlesund, Group CEO.

Source: Evolution annual and quarterly reports, StockOpine analysis

Asia is growing fast, accounting for 33% of revenue for the 9M 2022 compared to 27% in 2021, due to an increasing end user preference for EVO products in Asia possibly as a result of adding more Asian flavour (new versions of Baccarat, Teen Patti, the hugely popular Asian variant of three card poker etc.) to the games. As per the latest call, nothing can be attributed to one-off events for Asia growth.

Regarding Asia and North America “we see good potential in both these markets and expect continued high growth rate going forward.” Martin Carlesund, Group CEO whereas Latin America can also be a key growth driver in the future (main growth driver in ‘Other’ category).

“Latin America is still in the infancy recording online casino, and I expect the market to continue to develop well. We have great momentum in the market and we are well prepared to continue our expansion here.” Martin Carlesund, Group CEO.

This analysis shows that EVO’s country risk is diversified as there is no +50% reliance on a single region and two of its key regions are growing really fast. Regulation can impact these revenues but as other parts of the world enter the regulatory era, the Company believes that it will be positioned to transition accordingly, like it did with Europe.

Clients

Evolution claims to have over 600 customers including key industry names such as Paddy Power, Betfair, William Hill (acquired by 888 Holdings), 32 Red, Unibet, 888 Casino, MGM, Ceasars to name a few.

Despite the large number of customers there is customer dependency as in 2021 the largest customer accounted for 11% and the top 5 for 22%. Nonetheless, this represents an improvement from 2017 where the #1 accounted for 9% and top 5 for 38%.

Source: Evolution Annual Report 2021

Such relationships are built on trust and having sophisticated clients scrutinising processes adds pressure to Evolution to keep at the highest standards and ensure game protection (e.g. eliminate any card counters or those using algorithms to trick the system, detect fraud attempts or money laundering). Likewise, Evolution runs an annual due diligence for its customers and investigates any suspected irregularities so as to mitigate any regulatory or fraud risks.

3. Governance

Insider Ownership

Founder/insider led companies is always a plus but given that we are dealing with a company being more prone to regulatory risks, we feel that having skin in the game enhances stewardship.

Currently, Österbahr Ventures AB jointly owned by Jens Von Bahr (Co-founder and Chairman of the Board) and Fredrik Österberg (Co-founder and Board Member) holds 10.7% down from 15.0% back in 2019.

Other Board members with a sizable holding are Ian Livingstone (0.23%), the brother of Richard Livingstone who owns 4.24% compared to 16.4% back in 2019 and Joel Citron (0.73%). From the Management Team none holds more than 0.5%.

Stewardship

The Board of Directors is experienced with 5 members elected in 2015 and 2 in 2021 and the necessary Board Committees (Audit, Remuneration, and Nomination) are in place.

We consider the size of the board small for a mid-cap company (although in line with Articles, 3-8 members) and we should have expected the CEO, Martin Carlesund to be a member of it (similar to other Swedish companies like Ericsson and Volvo) despite the fact that he is already attending the meetings.

Nomination Committee proposed to increase the Board member fees from €30k per annum (“p.a.”) to €100k p.a. on 8th April 2022 AGM, which is more comparable to Playtech. A competitive fee is necessary to ensure that Board Members will continue to serve the Company but they could have avoided the €400k fee to the Chairman (despite being market fees) since he is already paid in his capacity as employee (total remuneration of c. €549k in 2021).

One of the duties of the Board of Directors (in which Jens Von Bahr is the Chairman) is ‘evaluating the Group CEO’ whereas Jens Von Bahr in his capacity as Executive Chairman reports to the Group CEO. That’s not necessarily bad as “The Board of Directors’ rules of procedure state that the work performed by the Chairman of the Board as an employee is separate from, and in addition to, his work as Chairman of the Board”, however, this is not a normal practice.

Management & Culture

Key Management (7 people) is experienced with the most ‘recent’ joiners being Jacob Kaplan, CFO, David Craelius, Chief Technology Officer and Louise Wiwen-Nilsson, Chief Human Resources Officer who joined in 2016.

Running a quick check on Martin Carlesund CEO, Jason Kaplan CFO and Todd Haushalter CPO we did not identify anything that questions their integrity, therefore, we feel comfortable that the existing management can continue execute.

The compensation of Martin Carlesund grew significantly from €1.8M in 2020 to €10.1M in 2021 driven mainly by the bonus of €5.8M. EVO does not give the specific metrics used, although it claims that performance criteria are based in promoting long term value creation.

Per Simply Wall St, CEO’s payroll is well above the average of $2.54M for similar size companies in Sweden. Nevertheless, it should be noted that in 2021, the Company almost doubled revenue and increased operating margin from 53.4% to 61.2%. CEO’s payroll was similar to Playtech’s CEO of €10.8M (€1.9M in 2020).

Glassdoor score which can be used as a proxy for culture is not optimal with an overall score of 3.5*, 75% Approve CEO, 63% Recommend to a Friend and 56% Positive Business Outlook. Looking at various players of the wider industry (live casino, gaming operators, land-based casinos etc.) it seems that the industry in general lacks other sectors which can be attributed to the job and industry nature.

Source: Glassdoor, StockOpine analysis

4. Industry

The ecosystem has the game providers (those who compete directly with EVO) who develop and provide the software, the game aggregators (see description in business model), the game operators who can be online (888Casino, Paddy Power, Draft Kings etc.) or land-based (MGM, Ceasars, Las Vegas Sands, etc.) and the final end user.

The industry for game providers is fragmented, though not everyone offers live dealer solutions like EVO which is regarded as the leader in this arena. Additionally, Evolution competes indirectly with land-based casinos (despite that land-based casinos are also customers of Evolution) as some people might prefer a land-based experience rather than online.

Who are the key Game providers (software)?

Evolution AB (founded in 2006) – listed on the main market of Stockholm, €1.1B Revenue in 2021, Operating Margin of 61.2%, c.16,000 employees, numerous awards although after 12 consecutive wins, it lost its ‘Live Casino Supplier’ EGR B2B Award in 2022 to Vivo Gaming.

Playtech (founded in 1999) - listed on London Stock Exchange (market cap c.1.6B GBP), €1.2B Revenues in 2021 (B2B is €554M), Operating Margin of 9.3%, operating across 26 countries, has over 6,600 employees and over 180 licenses. Has also won the ‘Poker Supplier’ EGR B2B Award for 2022 and ‘Aggregator Platform’ for 2021.

Microgaming (founded in 1994, acquired by Games Global Ltd in 2022) – private company licensed among others in UK, Malta and Gibraltar. Has won various awards throughout its history with one of those being ‘Platform of the Year’ EGR B2B Award for 2020

Pragmatic Play (founded in 2015 – part of IBID Group) – considered as one of the fastest growing provider of slots games and entered live dealer games in 2019, certified and licensed in over 20 jurisdictions, partner with similar clients as EVO and has the quality ingredients to contend EVO (still a long way to go given the lower number and type of games they offer). Won the ‘Bingo Supplier’ and the ‘Casino Software Supplier’ Awards EGR B2B 2022.

Vivo Gaming (founded in 2010) – private company and considered one of the best live dealer games providers, which also won the ‘Live Casino Supplier’ 2022 EGR B2B Award (an award for which EVO was the undisputable leader for 12 years). Vivo Gaming mainly operates in Latin America such as Peru, Colombia and Uruguay and per livecasino.com, Vivo Gaming is not considered US friendly which is positive for EVO given its expansion in US.

Other names include but are not limited to Authentic Gaming (acquired by Light & Wonder former Scientific games, a $6b company), Play’n GO (no live dealer games), SA Gaming (marketed towards Asia), Asia Gaming, BetGames etc. More information for each competitor can be found here.

The barriers of entry (i.e. developing a live casino solution) are relatively low, however to gain trust with leading operators, avoid legal pitfalls and deliver a technically and operationally great product (high volume, profitable etc.) is easier said than done, which effectively gives an edge to key players like Evolution. The new metric introduced by EVO (game rounds index – shows the development of game rounds played weighted by revenue contribution) to measure activity in its network grew by 70% y/y (higher than revenue) and it gives an indication to the stickiness of users to EVO games.

The unit economics of EVO compared to Playtech, i.e. consistently higher profit margins (EBITDA 2017 - TTM averages: 56% Vs 21%), as well as the consistently higher returns on capital (2017 - TTM averages: 28% Vs 4%) demonstrate competitive advantages that make EVO a strong player for a long-term success.

Competition is fierce both on Live and RNG, but the need for constant innovation results to inventing better games that could attract more players in the online space.

Market size and forecasts

On the wider industry, the online gambling market per Straits research is expected to grow from $57B in 2021 to $153B in 2030 (CAGR of 11.7%) whereas Databridge Market Research predicts that the online gambling market is expected to reach $144.74B by 2028 (CAGR of 13.7%).

Live Casino which is the bread and butter of EVO is considered to be one of the attractive verticals in the industry. Global online casino market, per EVO Annual report (uses data from H2 Gambling Capital), is estimated at €23.9B in 2021 (up from €19.4B in 2020) with Live Casino accounting for €7.5B and RNG for €16.4B and generated a CAGR during 2017-2021 of 31.1% and 14.7%, respectively. Comparing the €7.5B in 2021 to the $18bn in Gross Gaming Revenue by 2025 disclosed in Playtech H1 2022 presentation (using the same source – H2GC), a CAGR of c.23% is implied in the figures for Live Casino.

5. Financials

As stated above, EVO depicted a Revenue CAGR of 47.1% for 2012 - Q3 2022 (“Historic Period”), while profits and free cash flows grew at a faster rate reaching an Operating Margin (“OPM”) of 62.4% compared to 30% in 2012 and a Free Cash flow (“FCF”) margin of 52.2% compared to 19% back in 2012.

Source: Evolution annual and quarterly reports, StockOpine analysis, Koyfin

Recent acquisitions (under RNG) were accretive to sales with NetEnt having the largest impact, however, Evolution also grows organically. RNG sales accounted for €229.5M in 2021 compared to €17.8M in 2020 whereas the remaining growth of €295.9M (or 58%) in 2021 was driven organically by the Live segment.

Operating margin improvement from 30% in 2012 to 62.4% TTM, demonstrates operating leverage. While product development cost may increase as development becomes more complex this cost is of fixed nature whereas the number of players and the amount wagered can grow exponentially once a game is launched. Personnel costs, which account for over 50% of total costs, increase as more studios or new tables are launched but revenue tends to grow faster.

Given its equity only capital structure, net income follows a similar trajectory with a CAGR of 58.8% and margin growing from 27.8% in 2012 to 58.6% in TTM.

Likewise, FCF follows a similar path with profitability, showing an average FCF to operating profit and FCF to net income conversion of over 80% and over 85%, respectively (since 2017).

EVO has a strong balance sheet with Cash and Short term investments of $320M compared to lease liabilities of $69M (nil debt). It also has non-current liabilities of $365.8M relating to the potential earn outs for BTG and Nolimit acquisitions but with operating cash flows of $795M in TTM, EVO will have no issue in meeting these obligations.

6. Capital Allocation

The Company in its attempt to position itself as the #1 world-leading content provider, actively engages in acquisitions to enhance its offering, mainly in the slot space (except DigiWheel). Regarding live casino acquisitions, Martin Carlesund, Group CEO indicated that “And I don't see the potential in buying a company in Live” as they are already increasing gap to competition.

The most notable acquisitions are Nolimit City in 2022 for €340M (all in cash, €200M upfront, €140M in earn-outs up to 2025), Big Time Gaming for €457.8M in 2021 (Cash €80M, €147.8M in shares and €230M in earn-outs up to 2024) and NetEnt (which owns Red Tiger) for €2.3B in 2020 in shares. From the below graph it can be inferred that EVO overpaid for its acquisition of NetEnt as the returns on capital (“ROC”) and (“ROE”) have declined since the acquisition. EVO equity base grew from €281M in 2019 to €2.7B in 2020 while profits did not increase proportionately.

This is also justified by the higher EV/EBITDA multiple paid for NetEnt (i.e. 28.4x) compared to 14.8x for Nolimit and 15.8x for BTG and the lower estimated EBITDA margin of 48% Vs 77% of Nolimit and 88% of BTG. Nonetheless, the acquisition was strategically important to enhance its B2B offering and to strengthen its presence in important markets like the US.

Source: Koyfin, StockOpine analysis

The Company’s dividend policy is to distribute a minimum of 50% of its profits and has distributed dividend since 2016 with a 5-year CAGR of 73.6% and a current yield of c.1.34%. The key risk is any goodwill (€2.4B, or €3.2B including intangibles - out of total assets of €4.2B) write-off that could distort profitability and thus dividend policy.

The Company does not have a repurchase program in place as the repurchase program announced on 3rd December 2021 was completed on 18th February 2022 (less than 1% of shares were repurchased).

7. Risks & Opportunities

Risks

Regulatory framework is complex, dynamic and inconsistent across jurisdictions: keeping up with changes is of paramount importance as engaging with countries in which gambling is illegal or which are sanctioned might result to revocation of licenses, which could be detrimental to revenues and expansion plans, and to massive fines. Not only EVO but also its clients should keep up with regulations and adapt to licensing regimes, otherwise they may lose their license to operate, negatively affecting EVO’s growth. Recently, in Nov 2021 EVO was accused by a rival complaining to US regulator that it operates in some countries illegally, with EVO denying the claim and concluding its internal review in April 2022 which resulted to some changes in processes with “no material impact” on earnings.

Martin Carlesund, CEO “When this report was created, of course, we review everything internally, and we prepare ourselves to hand over any information that is requested. And of course, we found a lot of things that we could do better as we do in all areas every day. So we are happy with that result and move on from there. And we have a good relation with the regulators in all over the world.”

Technological advances and change in consumer taste: As live casino has disrupted the land-based casino, virtual reality can disrupt live casino. There are not many games implementing such technology but NetEnt offers the Gonzo Quest VR game. This might give a leap to Evolution but it is unknown whether this disruption will materialize (is on the early innings). The Company has to be on its toes to continuously innovate on a game level and a technological level so as to keep up with digital trends and to offer improved gaming experience.

Online card counters: Card counters are harder to deal online as they can use software to count cards while the game is run or run algorithms to detect ball speed in roulette or to detect how the wheel is spinning, thus Evolution needs to ensure that such activities are detected as early as possible. Otherwise, the reputation can be damaged and the relationship of trust with its high esteemed clients can be destroyed. The dedicated Game Integrity and Risk Department (setting-up protection systems) as well as the Mission Control Rooms which are responsible for ensuring operational excellence, system availability, security and regulatory compliance shows how serious is EVO regarding game integrity and eliminating fraudulent activity.

Opportunities

Regulation is not only a risk but can be a huge opportunity for the industry. As per American Gaming Association (“AGA”), Americans bet $337.9B with illegal iGaming websites and with a $13.5B in estimated revenue, the illegal market is estimated to be 3x the legal US iGaming market (estimated at $5B for 2022, $3.7B in 2021). As iGaming is only legal in six states, 48% of Americans have played online slots or table games with illegal online casinos. Further to these findings, the study shows that 40% of all gaming machines are unlicensed and house edge rates stand around 25% Vs 7.16% in Nevada.

Source: AGA, State of the States 2022 - ANNUAL U.S. INTERNET GAMING REVENUE

As, and if, more states legalise online casino (see Indiana, potential for nearly $1B) it can be an opportunity both for Evolution to capitalise on these new markets and for end users to play fair games with much lower house edge. Nonetheless, illegal/unregulated game will never vanish as there will always be people that don’t go by the book and solely use these gambling methods (no KYC, no taxes, illegal source of money etc.).

International expansion: Beyond North America, EVO has a significant potential for growth in Asia as it is still considered a small player and in Latin America which is at its infancy regarding online casino.

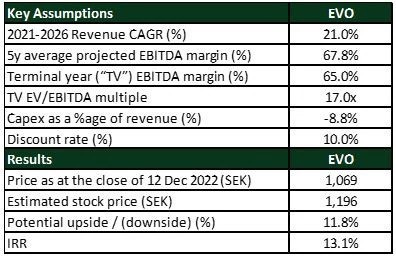

8. Valuation

The stock price as of 12th of December 2022 stands at SEK 1,069.4 and is down by 16.9% YTD. The market cap of the Company stands at SEK 228B and trades at an EV/EBITDA TTM multiple of 22.1x. Based on our DCF valuation the estimated value of EVO share is SEK 1,196, 11.8% higher than the current price level, with a resulting IRR over a 5-year period of 13.1%.

Source: StockOpine analysis

To estimate the fair value (“FV”) of Evolution we assumed a revenue CAGR of 21% which is well below its 5-year CAGR (2016-2021) of 56% and rather in line with the Live Casino expected industry growth of 23%. The forecasts imply a CAGR of 23.6% for Live Casino and 9% for RNG. Given the wider market forecasts, the execution of EVO and the trend in US of legalizing iGaming thus reaching the untapped illegal market of $13.5B, we consider that revenue assumptions are fair. It shall be noted that there is an upside from RNG, as in the recent earnings call management reaffirmed its long term target of a double-digit growth for the RNG segment (excluding Nolimit).

In terms of profitability, we used an average projected EBITDA margin of 67.8% and a terminal EBITDA margin of 65%. Both average and terminal EBITDA margins are higher than the average EBITDA margin of 56% for 2017-TTM, however, these are lower than 2021 margin of 68.7% and 69.5% for the 9M 2022. Management estimates 69%-71% for 2022 and we keep a 69% margin until 2024. Thereafter, we gradually reduce that to 65% to account for the upward pressure on costs and the generally higher wages in North America.

To derive the free cash flows to the firm we deducted projected Capex requirements of 8.8% in line with its 5 year average.

In respect to the terminal EV/EBITDA multiple, it is assumed to be around 17x which is lower than its 5 year average of 27.3x (excluding 2020) and its current multiple of 22.1x. The peer set is limited to gaming operators (except Playtech which carries a multiple of 7.6x) rather than gaming providers and carries an average EV/EBITDA multiple of 11.8x. We do not consider that multiple to be representative of a company that generates EBITDA margins at the high 60s when peer’s set average is below 20%. The multiple assumption used is closer to the c. 15x used for Nolimit City acquisition and the c. 16x of BTG acquisition.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialise at all), we reach a value per share of SEK 1,196, 11.8% higher than the current price of SEK 1,069.4 with a resulting IRR over a 5-year period of 13.1%.

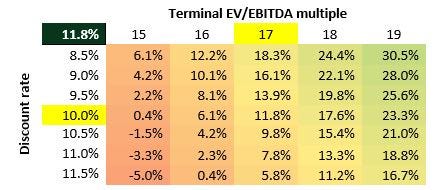

Sensitivity analysis

The below table gives an indication of the potential upside/(downside) %age compared to the current price (SEK 1,069.4 as of 12th of December) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

9. Concluding Remarks

EVO is the undisputable leader in Live Casino with superior margins and returns on capital compared to peers, despite operating in a highly fragmented market. Although the barriers of entry are relatively low, building a relationship of trust with key gaming providers takes a long time to be established.

Considering the above, the addressable market and the potential IRR, we believe that Evolution can be a long term winner. Consequently, we decided to initiate a position equal to 3.5% of our portfolio. For full transparency, it shall be noted that the price has changed from SEK 1,069.4 and the position was initiated at SEK 1,006.8.

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

Excellent report, StockOpine. Evo's operating margins are remarkable!

Outstanding Report StockO! ;)

Thanks my good friend.

Kiwi <3