Before we delve into the first write-up of December, we want to extend our warmest holiday wishes to you and your loved ones. Merry Christmas! We are thankful for your support!

As for the last month of 2023, here’s our plan:

a) Today's post will focus on Evolution AB. The significant drop in price (over 18% in the last 6 months) has intrigued us to revisit our thesis and explore the possibility of adding to our position.

b) Next week, we will make our analysis of PayPal available to everyone (Decoding PayPal's Figures: Valuation and Growth Analysis) until the year's end. We are delighted to offer this opportunity to celebrate our +3,000 readers and we believe it's an exciting chance to explore into our work and help spread the word about our newsletter.

c) In the last week of December, expect an article featuring a global skincare company. Let's keep the name as a surprise until the release.

d) And finally, the big news! Our 2023 Christmas Offer grants a 25% discount for 1 year on all plans. Don't miss out on this amazing deal! 🎁🎄

Without further ado, let’s dive into Evolution AB (“EVO”, “Evolution”, and “Company”) to assess its recent performance, growth prospects across various regions and the supply chain challenges, to compare EVO with peers and conclude with a revised Discounted Cash Flow (“DCF”) valuation.

If you are interested to learn more about EVO’s business model, we suggest reading our previous (free) article titled Evolution AB – A ‘sin’ stock with healthy returns.

Contents:

Supply chain issues

Regional breakdown

Performance overview

Valuation

Conclusion

1. Supply chain issues

“During Q2 and now also Q3, we see higher demand for Live Casino than we currently can deliver, which is very positive as our games have phenomenal traction on demand. Even so, we need to expand our studio space as well as increase the speed of recruitment. We're addressing this with foot force and at the moment in parallel building new studios in Europe, LatAm and also planning to add new studios in North America as well as expanding existing studios.” Martin Carlesund, CEO (own emphasis).

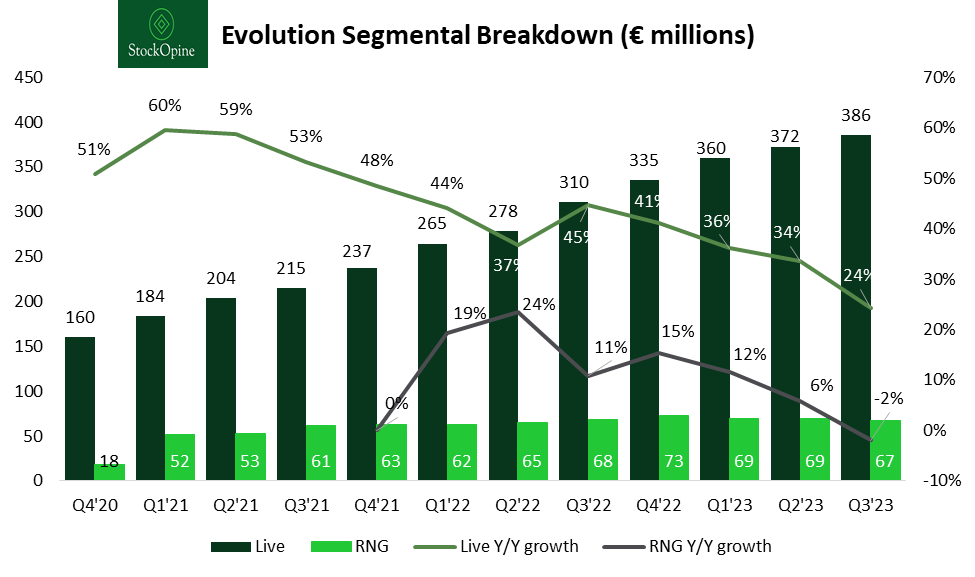

Evolution's Live segment continues to exhibit robust growth, albeit at a slightly slower pace, reporting a 24.3% increase over the most recent quarter. However, there are concerns stemming from the Company's struggle to address undersupply challenges, particularly prevalent in Europe. Admittedly, in Q3’23, revenue was adversely impacted by a 6-8% foreign exchange (“FX”) impact, but focusing on controllable aspects like capacity is more important to our analysis than FX.

Source: Stratosphere.io (use coupon code STOCKOPINE for a 25% discount), StockOpine analysis

Capacity is a factor that directly affects meeting customer demand and expanding market share. If Evolution fails to meet this demand, operators might turn to other providers, providing them with an opportunity to capture market share as players become more familiar with their games.

Evolution has previously faced similar challenges in Europe in 2020 due to favorable evolving EU regulations, and in 2021 in the US. Although successfully navigated in the past, the landscape has shifted and it’s no longer a ‘one-man show’. Other players exist, albeit smaller than EVO in Live offering, such as Playtech, which reported significant growth from €62M in FY19 to €143M in FY22 (Compound Annual Growth Rate “CAGR” of 32%) in the live casino revenues. While Playtech's growth over the same period falls short of EVO's 48%, it's noteworthy that Playtech now possesses the capacity to scale due to the ample number of studios to secure market share, currently operating above 10 live studios compared to ~20 for EVO.

Why is this concerning? Management highlighted the need for global capacity expansion more than 12 months ago in Q3’22 and specifically emphasized the demand surge in Europe in Q4’22. However, no additional studios have been launched in the EU since then. Yet, it’s crucial to note that setting up a studio can take anywhere from 12-18 months and while management should be partly blamed, they deserve credit for launching two studios in Latin America (“LatAm”) – one in Argentina in Q2’23 and a smaller one in Colombia in Q3’23 – a region that has substantial growth potential.

During 2023, EVO underinvested in CAPEX in absolute terms and as a percentage of sales. This underinvestment stems from a decrease in Property, Plant, and Equipment (“PPE”), as opposed to intangible assets (such as the development of new games and technical enhancements of the platform), which displayed a year-on-year (“Y/Y”) growth. EVO reported a total CAPEX of €64 million for the first 9 months of 2023, well below its targeted 2023 CAPEX of €120 million. Nonetheless, it expects a rise in Q4.

Source: Stratosphere.io (use coupon code STOCKOPINE for a 25% discount), StockOpine analysis

Expansion efforts take time and monitoring the progress towards the set-up of the new EU studio that is expected by the year's end (less than 20 days left…!) and the planned 3-4 studios for the next year across Europe, North America, and LatAm is a must. If Evolution executes on these plans effectively, these concerns are likely to be alleviated.

It’s important to note, that the establishment of new studios won't contribute effectively to capacity if recruitment efforts don't keep pace. In the first 9 months of 2023, EVO added 1,746 full-time equivalent (“FTE”) employees, which, when annualized, amounts to 2,328—falling short of both the 2021 and 2022 FTE hires of 2,799 and 2,885, respectively as well as the Company's internal expectations. EVO acknowledges the need to accelerate its hiring process, but the decline in its Glassdoor rating, from 3.5* per our last year’s report to 3.3* as of December 12, 2023, raises concerns about the Company's readiness to achieve timely success.

Our overall stance on these issues is neutral, with confidence that EVO will navigate these hurdles as it has substantial resources, with cash reserves totaling €813.3 million as of September 30, 2023, and zero debt along with lease liabilities amounting to €80.1 million. Additionally, EVO’s robust EBITDA margins at ~70%, provide a cushion to absorb any fluctuations if the Company opts to expedite the recruitment process. However, it's essential to keep a balance while addressing short-term challenges; and EVO should avoid rashly raising wages beyond market rates.

Historically, we haven’t observed irrational increase in the cost per employee (excluding senior executives), except for 2022 when costs surged by 12.9%. Though, two distinct factors justify this increase. Firstly, the average number of employees in the US (where wages are higher) grew as a percentage of the total workforce from 7.4% to 11.9%. Secondly, there was an 11.9% appreciation in the average exchange rate of USD against EUR, along with a 23.4% appreciation of the Georgian Lari (Georgia being the country where 43.5% of employees are located).