KLA Corporation Q4’FY24 Earnings

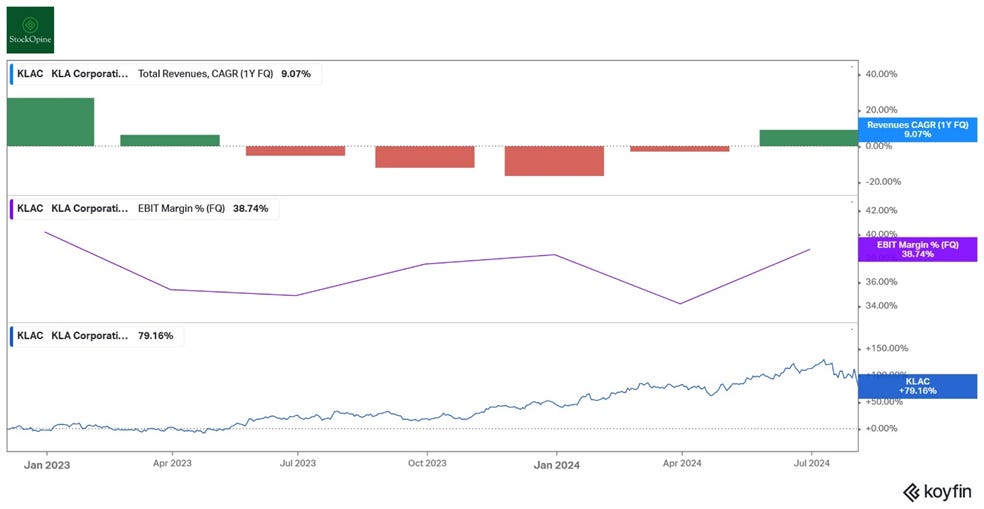

It’s been a while since we last released an update on KLA Corporation. Although the company has executed well; during the last four quarters preceding its Q4 FY24, it faced declines in both revenues and gross and operating profitability. However, its share price (as shown in the last chart of the image below) has followed a different trajectory, mainly as a result of the ongoing Gen AI frenzy that drove valuation multiples higher. In its March 2024 update (Q3 FY24), management stated,

“We are confident quarterly revenue levels for KLA bottomed in the March quarter as expressed in our prior earnings call.”

This appears to be the case, given the 9% increase in revenue over the latest quarter.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

In this update, we'll review the latest results, discuss the outlook across the key industry players, and provide an updated valuation (DCF and Reverse DCF).

If you're interested in learning more about KLA Corporation, check out our deep dive from 2022 (free):

We've extended the 25% summer offer to monthly plans! Try it out today.

1. Results Overview

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

a. Quarterly Performance

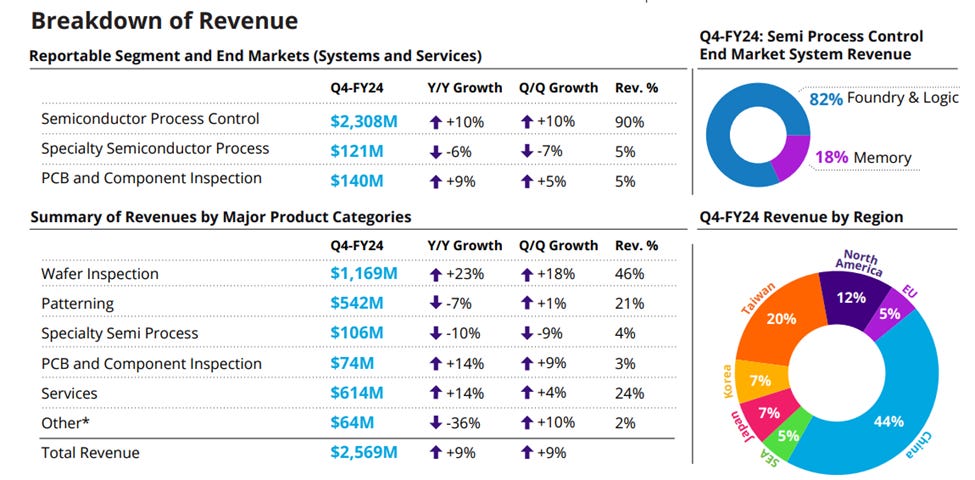

Revenues: $2.57 billion, up 9.1%, surpassing consensus and at the high end of guidance.

Wafer Inspection (46% of revenue) grew 23% year-on-year, driven by strong foundry/logic demand.

Patterning (including metrology and reticle inspection) increased 1% sequentially but fell 7% year-on-year.

Services reached $614 million, up 14% year-on-year, aligning with the upper end of the 12-14% long-term growth target. Management expects this growth rate to continue in the near term.

Specialty Semiconductor declined both sequentially and year-on-year, but management attributes this to timing (lower power semi for automotive applications) and anticipates modest growth for the calendar year.

Source: Q4’24 Earnings infographic KLA

Non-GAAP Gross Profit: $1.61 billion, up 11.5%, with a gross margin of 62.5%, compared to 61.2% in Q4’23, due to a better product mix and higher-than-expected revenues.

Operating Profit: $977.3 million, up 18.6%, with an operating margin of 38%, compared to 35% in Q4’23. Non-GAAP operating income rose 17.5% to $1.05 billion, with a margin of 41% compared to 40.1% in Q4’23.

Net Income: $836.4 million, up 22.2%, with a profit margin of 32.6%, compared to 29.1% in Q4’23.

Key yearly updates

China Sales Contribution: In FY24, sales from China, a major region for manufacturing legacy node logic and memory chips, increased to 43%, up from 27% in FY23 and 29% in FY22. This presents a significant risk due to