Every month we share 2 detailed company write-ups; one on an existing portfolio company and one on a potential portfolio candidate. If you wish to learn more about our offering, visit the “About StockOpine” section.

Contents:

Key Facts

Business Overview

Management

Industry

Financial Analysis

Competitive Advantages, Opportunities and Risks

Valuation

Conclusion

1. Key Facts

Description: Nemetschek SE (“Nemetschek”, “Company”) with ticker $NEM.DE is a leading provider of software solutions in Architecture, Engineering, Construction and Building operations industry (AEC/O).

Key Financials: Over the period FY13 to trailing twelve months (“TTM”) Q2 FY23, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 16.7% and operating income CAGR of 18.3%, reaching a TTM revenue of c. €818 million and operating income of €176 million (margin of 21.5%). Nemetschek has cash and cash equivalents of €209 million compared to total debt and long-term lease liabilities of €116 million.

Price & Market Cap (as of 24th October 2023): Its market cap is €7.8B with a 52-week low of €42.8 and a 52-week high of €75.3, whereas it currently trades at €67.7.

Valuation: Nemetschek trades at a TTM EV/EBITDA of 32.9x (3 Year average of 37.6x) and a TTM EV/Sales of 9.5x (3 Year average of 11.7x).

2. Business Overview

Background

Nemetschek SE is a German entity founded in 1963 by Prof. Georg Nemetschek. The Company is a leading provider of software solutions for the architecture, engineering, construction, and building operations industry (AEC/O) and was one of the first companies which used computers for design in the construction industry, exemplified by its flagship CAD software, Allplan, launched in 1984. Its software solutions cover the entire lifecycle of a building, including design, construction, and operation while these solutions are utilized by architects, engineers, construction firms, and property managers.

AEC/O represents the core revenue driver for Nemetschek, accounting for approximately 87% of its total revenue. In addition to AEC/O, the Company expanded into the Media and Entertainment industry with the acquisition of Maxon brand in 2000. Nemetschek’s Media and Entertainment solutions specialize in 3D animation and rendering of visual effects.

Nemetschek became a publicly traded company in 1999 and has since delivered impressive returns of 2,298% for its shareholders, representing a CAGR of approximately 14.3%. Over the years, the Company has demonstrated excellence in capital allocation, expanding primarily through strategic acquisitions.

Segments

Nemetschek operates through four segments; Design, Build, Manage and Media generating 49%, 33%, 6% and 13% of 2022 sales, respectively.

Source: Nemetschek Annual report 2022

It manages a portfolio of 13 brands, each functioning independently but supported by the holding company Nemetschek SE. However, Nemetschek is actively exploring ways to streamline and harmonize its brands to enhance operational efficiencies and cross-selling opportunities.

Source: Annual Report 2022

Nemetschek claims to serve approximately 7 million users globally, though it's important to note that the number of paid subscribers within this user base is not specified. Nonetheless, this places the Company among the industry leaders in providing software solutions for the AEC/O sector. In terms of market leadership, Autodesk, the largest player in the industry, generated around $2.3 billion from its AEC segment (excluding AutoCAD) for FY23, compared to Nemetschek’s AEC/O revenue of €707 million for FY22. Autodesk boasts 6 million paid subscriptions and an estimated 15 million non-compliant users.

a. Design

Design is the most substantial part of Nemetschek's business, contributing €392 million in revenues for FY22, which constitutes 49% of the total business. The Design segment's major brands, including Graphisoft, Allplan, and Vectorworks, position the Company as a prominent player in the Building Information Modeling (BIM) software sector, with a strong presence in Europe.

Although the Design segment may not be the fastest-growing within Nemetschek, it stands out as an attractive segment due to the high customer retention rate and increasing regulatory requirements mandating the use of BIM software across various regions. This mission-critical software is predominantly used by architects and engineers, making it an integral part of their workflow with a steep learning curve, resulting in high switching costs. Overall, the Design segment represents Nemetschek's core strength.

Source: StockOpine Analysis, Nemetschek Annual Reports

Over FY18 to FY22, the Design segment recorded a revenue CAGR of 8.2%, with EBITDA margins typically ranging around 30%. The transition to a subscription-based model has impacted EBITDA margins, but this is expected to be a short-term challenge. Looking ahead, the Design segment is poised for sustained growth, fueled by the increasing adoption of BIM practices.

Notable competitors in the Design segment include Autodesk, Trimble, Bentley Systems, and Hexagon (further discussed in the industry section). Autodesk, with its Revit (BIM solution) and AutoCAD solutions, is viewed as a leader in this space.

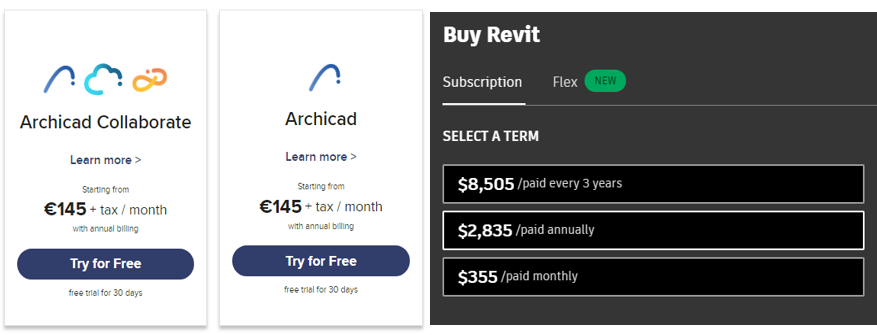

As it can be observed from the below images, Nemetschek maintains competitive pricing across its major brands, differentiating from Autodesk, which often prices Revit at a premium compared to Nemetschek's offerings. Nemetschek's robust pricing power enables the Company to implement price increases to further support its growth.

Source: Graphisoft, Autodesk

b. Build

The Build segment offers construction lifecycle solutions which enhance construction planning and project management. Nemetschek’s customer base primarily consists of construction companies and developers, predominantly in the United States and German-speaking countries.

The Company serves two key niches within the construction lifecycle through this segment. It encompasses the Bluebeam brand, the Company's US-based subsidiary and largest brand in terms of revenue, which specializes in workflow solutions for collaboration and documentation. The other key brand is Nevaris, offering ERP solutions tailored for the construction sector.

Major competitors in this space include Procore and Autodesk's Construction Cloud. When comparing Bluebeam to Procore, a leader in construction lifecycle solutions, it becomes evident that Procore offers a more holistic construction management solution which includes scheduling, accounting management, bid comparison, project management and more. Procore exhibited remarkable revenue growth of 40% in FY22, reaching $720 million compared to Nemetschek's Build segment, which achieved a 24% growth, reaching €268 million. Additionally, Autodesk reported an impressive year-over-year increase in Q2'24 of over 100% in Autodesk Construction Cloud Monthly Active Users, underscoring the industry's momentum.

Over FY18 to FY22, the Build segment demonstrated robust growth with revenue CAGR of 17.3%, reaching an EBITDA margin of 38.5%. However, EBITDA margin slightly declined to 35.2% for the last twelve months due to the ongoing transition to subscription model at Bluebeam. Over the long-term, the transition is expected to have a positive impact on margins while the under-digitization of the construction industry presents an opportunity for sustainable growth.

Source: StockOpine Analysis, Nemetschek Annual Reports