Several of our portfolio companies have reported earnings over the past few weeks. While we share key highlights in the premium chat when necessary, we want to provide additional context on PayPal's Q3 2024 earnings, which led to a share price drop of over 4% on October 29, 2024.

But first, a word from our sponsor!! 👇

With earnings season here, we want to share a tool that has become indispensable in our research routine: Borsa. Don't have time to read an entire earnings call transcript? Borsa's latest AI Summary feature makes catching up on earnings calls quicker and easier than ever. Borsa provides concise summaries of the opening remarks and the Q&A portion of every earnings call.

Borsa's AI Summary includes citations that link directly to the moment in the call where the topic was discussed, providing an interactive table of contents for every earnings call. Skip to specific discussions on operational metrics, market trends, guidance, etc with just one click.

Borsa isn’t just simple—it’s a powerful tool for finance pros. With presentation slides, earnings releases, and transcripts for every call, Borsa makes researching companies incredibly easy. Trusted by analysts, fund managers, and individual investors worldwide, Borsa has been featured live on CNBC twice. The Borsa team is 100% bootstrapped and has been at it for over six years.

Don’t miss a beat this earnings season—streamline your research with Borsa (iOS | Android).

1. Financial Results

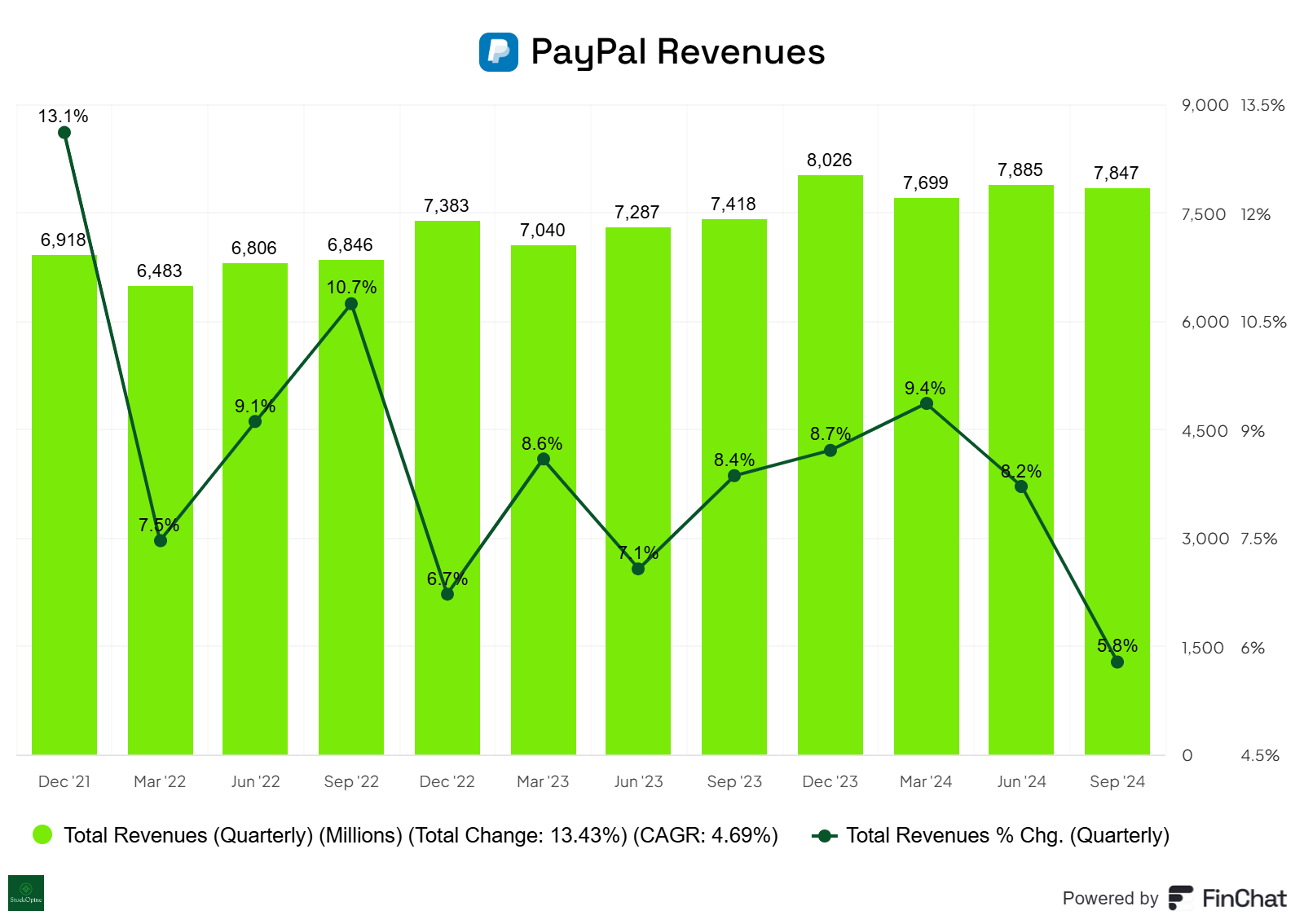

Revenue of $7.85 billion Vs consensus of $7.89 billion. Revenue was up 5.8% year over year.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Non-GAAP operating income was $1.48 billion, exceeding the consensus estimate of $1.37 billion. This represents an 18% increase, adding 194 basis points to the operating margin, which improved from 16.9% to 18.8%.

Non-GAAP EPS came in at $1.20, surpassing the consensus estimate of $1.07.

Source: PayPal filings, StockOpine analysis

Overall, there was an improvement in transaction margin (rising from 45.4% to 46.6%), which we will review shortly, and continued cost control, as non-transaction costs increased by only 3%. These factors support the margin improvement, which has followed a steady upward trend since Q2 2023. For Q4, management anticipates accelerated operating expenses due to deferred marketing costs shifted to the second half of the year, prompting a revision of the outlook from a slight increase to a low single-digit increase.

“We expect higher non-transaction OpEx growth in the fourth quarter as we have intentionally concentrated more of our discretionary investment spend, particularly in marketing during the back half of the year and in the holiday season. This is strategically timed to support key initiatives, including the go-to-market of new products and innovation, as well as ongoing marketing and brand campaigns for PayPal and Venmo.” Jamie Miller CFO

2. Payment Volume

a. Total Payment Volume

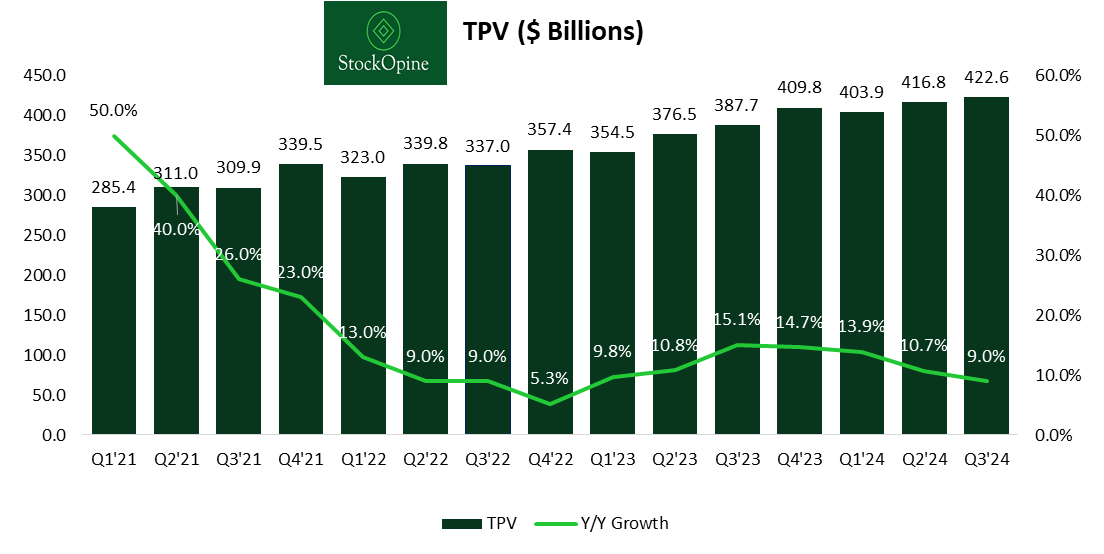

Total Payment Volume (TPV) reached $422.6 billion, a 9% increase from Q3 2023, driven by healthy growth across all categories.

Source: Company filings, StockOpine Analysis

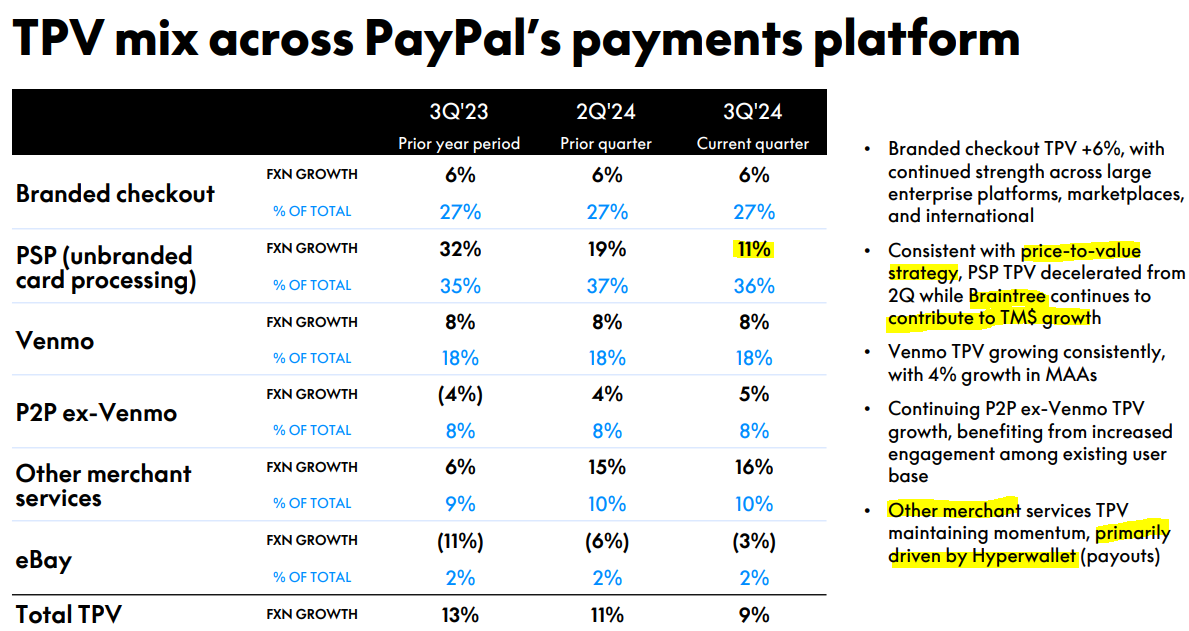

However, TPV growth for PayPal's unbranded card processing (primarily Braintree) decelerated to 11%, down from 19% in the prior quarter.

Source: PayPal Q3’24 earnings presentation

Source: Company filings, StockOpine Analysis

While this slowdown may seem concerning—particularly as Braintree has been a major growth driver—we need to give management time to deliver on their promises. PayPal is implementing a 'price-to-value' strategy in Braintree's renewal contracts, which, as reflected in improved transaction margins, supports profitability even if it risks some business loss. Does this mean no changes were needed? We don’t think so but achieving the right balance between growth and profitability will take time.

“As part of our price-to-value strategy, we are moving deliberately and making decisions that prioritize healthy, profitable growth rather than targeting a high proportion of processing volume at low or even negative margins.

What this looks like in practice with some of our largest enterprise customers is often a renegotiated agreement that reduces our total share of payment processing to a more balanced level. So for example, from 95% to 75%, but with better economics and with a greater breadth of products and services. This means we are driving Braintree transaction margin dollar improvements and more strategic partnerships, but with lower volume and revenue growth.” Jamie Miller CFO

This also reveals another side of the story—or at least raises the question of whether payments have become commoditized and if this is a race to the bottom. We think that merchant’s decision to retain 75% of volume with Braintree indicates that merchants are looking for more than just low prices.

“When I talk to the CEO of a merchant, yes, they want great processing pricing, but you know what they're really focused on, how do they grow customers? How do they get more customers to buy their products? And those are now value services that we're able to bring to them.” Alex Chriss, CEO

b. Venmo TPV

Venmo remains a significant growth opportunity for PayPal, as it is still largely unmonetized. Nonetheless, its 8.2% growth to $74.8 billion is healthy.

With the Venmo Debit Card and Pay with Venmo serving as key channels to boost monetization, it’s worth noting the 30% growth in monthly active debit card users, consistent with the prior quarter—though only 5% of monthly active Venmo users are currently active debit card users. These users spend four times more, so expanding this group would improve profitability. As for Pay with Venmo, only 8% of consumers are active users, leaving considerable room for growth despite a 20% increase last quarter.

For merchants, management has announced that Pay with Venmo will be bundled with PayPal Checkout to accelerate distribution. While this may initially mean lower pricing and profitability, following Braintree's precedent, in the long term, this approach is expected to benefit transaction margins, where it is already having a positive impact.

Source: Company filings, StockOpine Analysis

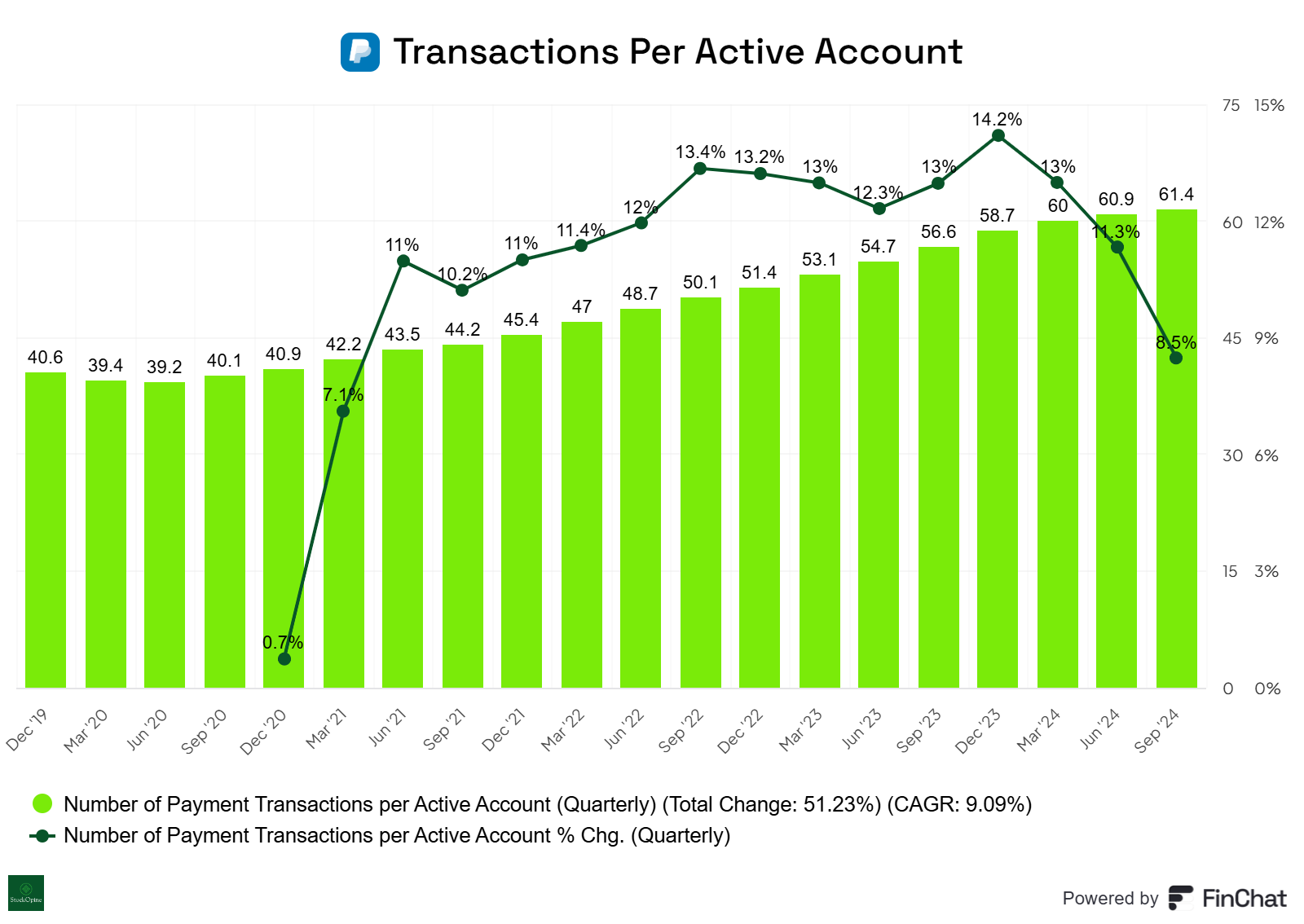

c. Transaction Per Active Account

There wasn’t much mention of this metric on the call, but if you’re tracking PayPal user engagement, growth in transactions per active account is quite revealing. This metric continues to grow at healthy levels, and in Q3 2024, we also saw the first year-over-year increase in Active Accounts since Q1 2023, now reaching 432 million.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

3. Take rates

The transaction take rate, declined to 1.67%, down from 1.72% in the previous quarter and the prior year. However, transaction margin improved once again, reaching 46.6%. Given that Braintree, which accounts for 36% of volume, previously pressured margins but began positively impacting transaction margins last quarter, we are confident that Q1 2024 marked the low point.

The take rate of 1.67% benefited from Braintree and Venmo monetization but was offset by a higher mix of large enterprise and marketplace growth within Branded Checkout. While these customers have lower take rates than SMBs, they contributed to higher volume.

Transaction expense decreased to 0.91% from 0.93% in the prior year, due to a favorable product mix, and transaction loss also improved, driven by better loss performance.

With the company's focus on the SMB space through its PayPal Complete Payments Platform (PPCP), Braintree’s improved unit economics and enhanced Venmo monetization, we anticipate at least a stabilization of transaction rates going forward.

“And then if I pull to 2025, I think the thing to think about is when we look at 2025, ex-interest income, we expect transaction margin dollars to grow at least as fast as 2024 on that same basis.” Jamie Miller, CFO

Source: Company filings, StockOpine Analysis

4. Other

Fastlane: Over 1,000 merchants have joined since its August launch, and this is only the beginning. It’s also worth highlighting the key partnerships with Adyen, Fiserv and Global Payments.

PayPal Everywhere (the go-to solution for spending, sending, and earning rewards both online and offline): Already at 1 million debit card users, with plans to expand to Europe in 2025. This initiative not only grants PayPal access to the offline total addressable market (TAM) but also enhances the value of other PayPal products.

“In addition, these debit card users are now choosing PayPal branded checkout more frequently when they shop online. Early data from our existing customers shows a 5x increase in total omni spend within the first two weeks of sign-up.” Alex Chriss, CEO

PPCP: Recently expanded to new geographies, including China and Hong Kong, with further markets planned for 2025. In regions where PPCP is available, nearly 40% of PayPal’s SMB processing and checkout volume has shifted from legacy products to this platform. PPCP has also partnered with Shopify, broadening access to small and medium-sized businesses. Here’s how management views PPCP’s impact:

“I'd love to just pile on small business. This is, as you all know, a very strong passion for me. What I feel great about is the innovation that we're rolling out. PayPal Complete Payments is now really the best one-stop shop for merchants to be able to do money in and access to capital. Money out, we still have opportunities as we think about the opportunity to allow small businesses to be able to send payments to others.” Alex Chriss, CEO

5. Outlook

Before we conclude this earnings review, we would like to highlight the most important items in the outlook:

Increased growth in transaction margins due to Braintree’s progress to date.

Higher EPS driven by improved profitability, although this would be impacted in the last quarter due to elevated marketing expenses.

Share repurchases have been maintained at $6 billion, consistent with free cash flow.

Source: PayPal Q3’24 earnings presentation

6. Conclusion

It was a mixed to solid quarter. Profit dynamics are improving, partnerships and new solutions are ramping up, innovation is progressing, and growth remains healthy. While the 11% growth in Braintree volume is somewhat concerning, the justification for the drop, namely the price-to-value strategy, makes sense. We simply need to allow time for transaction margins to continue improving.

If you would like to learn more about PayPal, check out our article, Unpacking PayPal: A Comprehensive Deep Dive into its Financials and Business (PART 2), where we also share our valuation estimate.