Welcome to Part 2 of our PayPal Holdings, Inc. (PYPL) analysis, where we assess whether this payment giant remains an attractive investment opportunity.

In this section, StockOpine dives into PayPal’s fundamentals, key financial metrics, and conclude with a valuation. If you’re interested in learning more about PayPal’s business model and competitive advantages, check out Part 1, prepared by our friend Timothy Panic Drop - Timothy Assi.

1. Financials

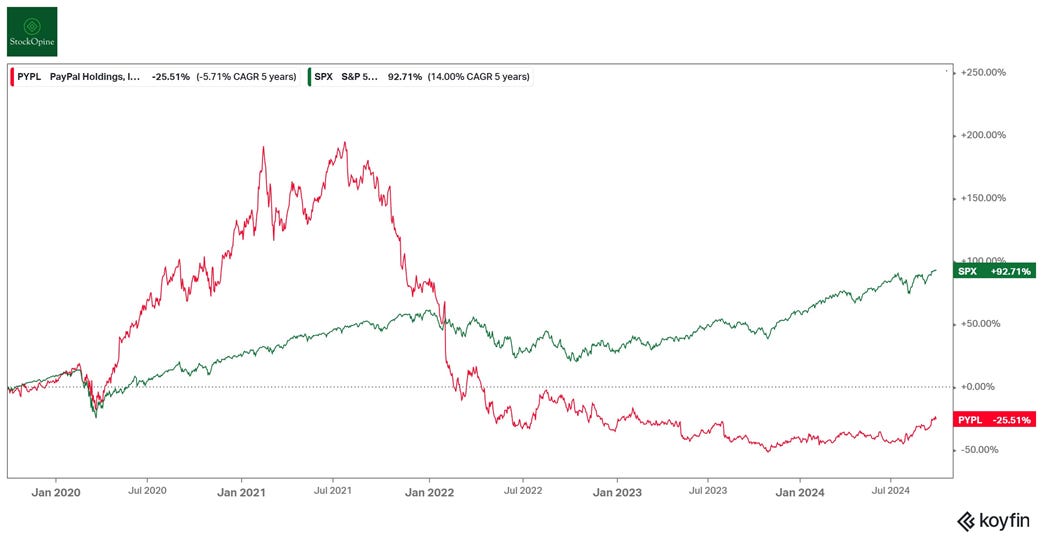

a. Stock Performance

After a post-pandemic bust, this $80 billion market cap giant has been significantly underperforming the index. Despite being flat in the first half of the year, momentum has shifted since early August, with the stock now recording a ~27% YTD increase.

Source: Koyfin (affiliate link with a 20% discount), Note: Premium StockOpine members can get a 3-month free trial on the Koyfin platform

Let’s dive into the numbers to see if PayPal’s share price is reflecting its underlying financial performance and whether there’s potential for future gains.

b. Profit and Loss

Since FY14, PayPal has delivered impressive performance, growing its revenues more than 3x with a CAGR of 15.3%, reaching $31 billion. Operating income has also expanded at a 16.3% CAGR, pushing the operating margin from 15.85% in FY14 to 17.15% on a TTM basis. However, after hitting a 17% margin in FY21, margins dipped to 14.7% in FY22. Thanks to continuous cost discipline, they have steadily recovered.

A similar trend can be seen in net margin and free cash flow margin (adjusted for SBC).

Source: Koyfin (affiliate link with a 20% discount), StockOpine analysis

The key driver of margin recovery has been a reduction in non-transaction-related expenses, indicating that while competition may pressure transactional margins (which we will discuss shortly), PayPal has effectively managed its controllable costs.

Source: Company filings

c. Total Payment Volume

Payment companies typically perform well when more transactions are processed through their platforms, as they earn a percentage of each dollar processed. Growth in transaction volume can be driven by either an increase in users or by users transacting more frequently through PayPal’s platforms. During 2023, PayPal crossed the $1.5 trillion TPV mark and today has a TTM TPV of $1.6 trillion.

Source: Company filings, StockOpine Analysis

As shown in the chart, PayPal’s transaction volume continues to grow, though at a slower pace compared to the pandemic boom of 2020 and 2021, when it surged by 31.5% and 33.1%, respectively, due to the shift toward online payments and reduced in-store activity. In 2022, volume growth decelerated as people returned to stores and competition intensified, putting pressure on branded total payment volume (TPV).

However, since the start of FY23, branded checkout, which accounts for about 30% of TPV, has shown healthy mid-single-digit growth, driven by improvements in user experience and bundling with unbranded processing (Braintree). Additionally, PayPal’s PSP (unbranded card processing) TPV—primarily Braintree's full-stack volume—also made up 30% of TPV at the beginning of 2023, posted impressive growth rates of over 25%, contributing to the reacceleration of TPV.

So, what makes Braintree (a competitor to the likes of Stripe and Adyen) a key driver for PayPal’s future growth? Let’s explore further!

d. Braintree

Processing payments for large companies, SMBs, and marketplaces requires a trusted partner that delivers speed, minimizes fraud, optimizes authorization rates, improves conversion rates for merchants and offers a great user experience.

Braintree operates with lower transaction margins (due to lower take rates and higher transaction expenses, such as funding costs), but in the long term, it can become more profitable as marginal costs decrease with higher volumes.

In our Decoding PayPal's Figures: Valuation and Growth Analysis and Adyen: Simplifying Payments with Top-Notch Quality articles, we compare PayPal with key players in the industry but here the focus is PayPal’s.

Since PayPal began reporting PSP (unbranded card processing) TPV, we observe impressive growth rates. However, this has negatively impacted transaction take rates, causing concern among investors, who were put off by the decline without fully understanding the reasons behind it.

Source: Company filings, StockOpine Analysis

Investors fear (and some still do) that PayPal’s aggressive pricing strategies to gain market share will continue indefinitely, ignoring the fact that it takes two to tango. Price isn’t everything as value-added matters too.

Management has already indicated that the moderate growth of 19% seen in Q2’24 was due to a shift in discussions with merchants. The focus has moved from simply gaining market share at any cost to emphasizing value propositions and protecting margins. PayPal has now reached a point where it has a solid product offering and a strong market share, allowing it to prioritize sustainable growth over aggressive pricing.

“So let me take you back. Braintree, if you go back a few years ago, was really trying to establish itself in the market. It hasn't delivered at scale, and there were gaps in the product. We've invested heavily in the product and have really focused on some of the largest U.S. enterprise customers, which now have proven the scale while we've gotten the product to parity. Then you look at what we just rolled out with innovations like Fastlane, I think we've now leapfrogged the competition.

We now are shifting towards being able to have a price-to-value conversation with our merchants and being able to really start to think about how will we ramp up go to market for not only Braintree, but also PPCP. We also are now moving into markets that have higher margins. So international and small business with both Braintree and PPCP allow us to now, again, price to value and have different conversations. So that is how we think about it. We're not focused on unprofitable growth when it comes to Braintree.” Alex Chriss, CEO Q4’23

“I mean, this product, the Braintree product, in particular, has highest auth rates, highest availability, highest performance. It's really best-in-class compared to our peers out there.

“And so how we've entered this year is really working with our teams to say, profitable growth matters. We shifted our incentive structures, which are all around transaction margin dollars and operating income dollars now.”

Jamie Miller CFO June 2024 RBC call

Turning to the latest quarter, we finally saw Braintree positively impact transaction margin dollars.

“Braintree is now meaningfully contributing to transaction margin dollar growth for the first time in over 2 years.” Alex Chriss, CEO

With that said, we are confident that Braintree will remain a key growth driver.

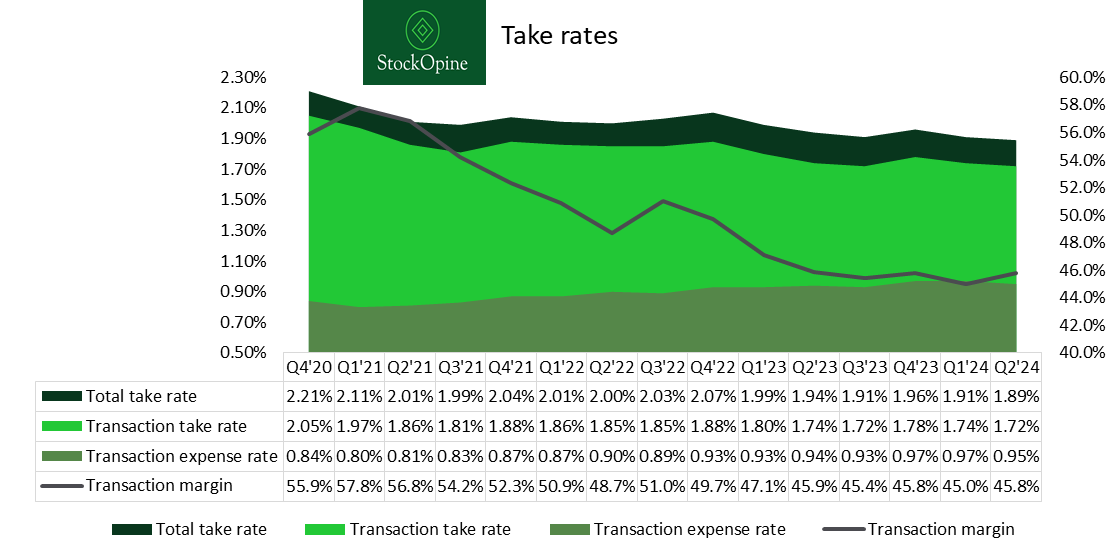

e. Take rates

Beyond total payment volume (TPV), the take rate is a key factor for the revenue of payment companies. It reflects the percentage PayPal earns from each dollar processed on its platforms. Since losing eBay to Adyen in 2020, PayPal’s total take rates have dropped significantly, falling from 2.67% in 2018 and 2.5% in 2019 to around 2%. Transaction take rates have similarly declined, moving from 2.3%-2.4% to approximately 1.85%, and now closer to 1.7%.

Source: Company filings, StockOpine Analysis

Another contributor to the lower transaction take rates and higher transaction expense rates has been Braintree’s accelerated growth. However, we believe that as PayPal shifts its focus towards profitable growth, take rates should stabilize. Additionally, further efforts to monetize Venmo—PayPal’s under-monetized P2P app—could help boost take rates and protect transaction margins. So, what is Venmo, and where does the opportunity lie?

f. Venmo

Venmo’s digital wallet processed over $70 billion in the latest quarter, representing around 18% of PayPal's total TPV. Venmo currently boasts about 90 million accounts, with 62 million active users who transacted within the past month.

Based on our previous estimates and data from PayPal, Venmo's take rate is approximately 0.5%, which is well below the company’s overall average. This highlights why CEO Alex Chriss is committed to boosting Venmo’s monetization efforts.

Source: Company filings, StockOpine Analysis

While Venmo’s volume is growing at healthy high single-digit to low double-digit rates, its impact on revenue remains modest. However, PayPal’s “Pay with Venmo” campaigns, new partnerships with merchants like AliExpress, Venmo on eBay, Teen accounts, and Venmo debit/branded cards available in Apple and Google wallets signal promising potential for growth. An interesting statistic shared in Q4'23 and Q2'24 demonstrates this momentum.

In Q4'23, management emphasized the push to drive adoption of the Venmo debit card, noting that Venmo debit cardholders are among the most engaged users, generating 6x the incremental revenue compared to P2P-only customers. At that time, only about 6% of active Venmo users (say about 3.6 million) had a Venmo debit card. In the two following quarters, management reported a 21% and 30% increase in monthly active debit card users, suggesting that users could now exceed 4 million, with significant potential as the product reaches all 62 million active monthly users. This growth also aligns with PayPal’s omnichannel strategy (e.g., the PayPal Everywhere campaign) making Venmo an untapped growth engine for PayPal.

To conclude this section, here are two relevant quotes from Alex Chriss, PayPal’s CEO:

“What excites me most about Venmo is that we are only scratching the surface of its potential, starting to drive customer-led profitable innovation, and we see substantial headroom for growth. Said simply, Venmo is primed for growth.” Alex Chriss, CEO

“You've heard me talk about our Venmo customers looking for us to provide more money in and money out opportunities. As we are improving opportunities to spend Venmo balance with products like Venmo Debit Card or Pay with Venmo, we are seeing a corresponding improvement in funds being used within the Venmo ecosystem rather than transferred out. This is an example of meeting our customers where they are, solving their needs and driving monetization and margin improvement in the process.” Alex Chriss, CEO

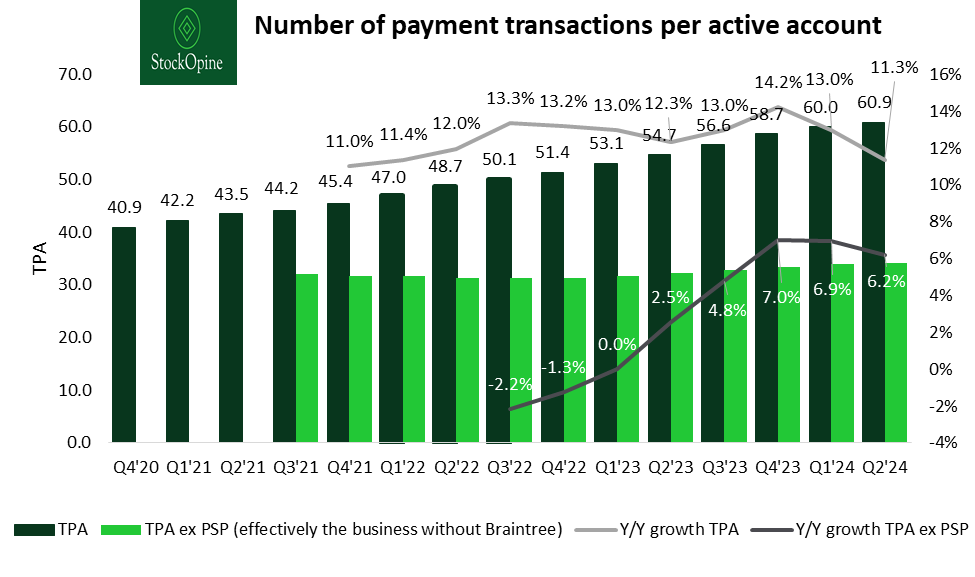

g. Transactions per active account

No matter how you slice the numbers, claiming that PayPal is in decline is simply incorrect. One main KPI we monitor to track the progress of our thesis is the number of payment transactions per active account (TPA), as it reveals a lot about user engagement.

Source: Company filings, StockOpine Analysis | Note: TPA ex PSP refers to the business excluding Braintree, providing insight into branded checkout and Venmo.

Similar to our earlier findings, TPA has been growing at double-digit rates. While PayPal has lost some users (active accounts—those that transacted in the past 12 months—peaked at 435 million in Q4'22 and are now at 429 million), each active user is performing more transactions. A further sign of improving engagement is the slight increase in monthly active users (those transacting within the past month), which grew from 221 million in Q4'22 to 222 million today.

Digging deeper into the data, we see that since Q3'23, TPA growth rates excluding PSP (primarily without Braintree) have been accelerating, reaching 6.2% in the last quarter. This demonstrates that growth is not only driven by Braintree but also by increased activity from Venmo and branded checkout users. We believe that a major catalyst for further acceleration in TPA could be Fastlane, which was discussed in detail by Panic Drop - Timothy Assi in Part 1.

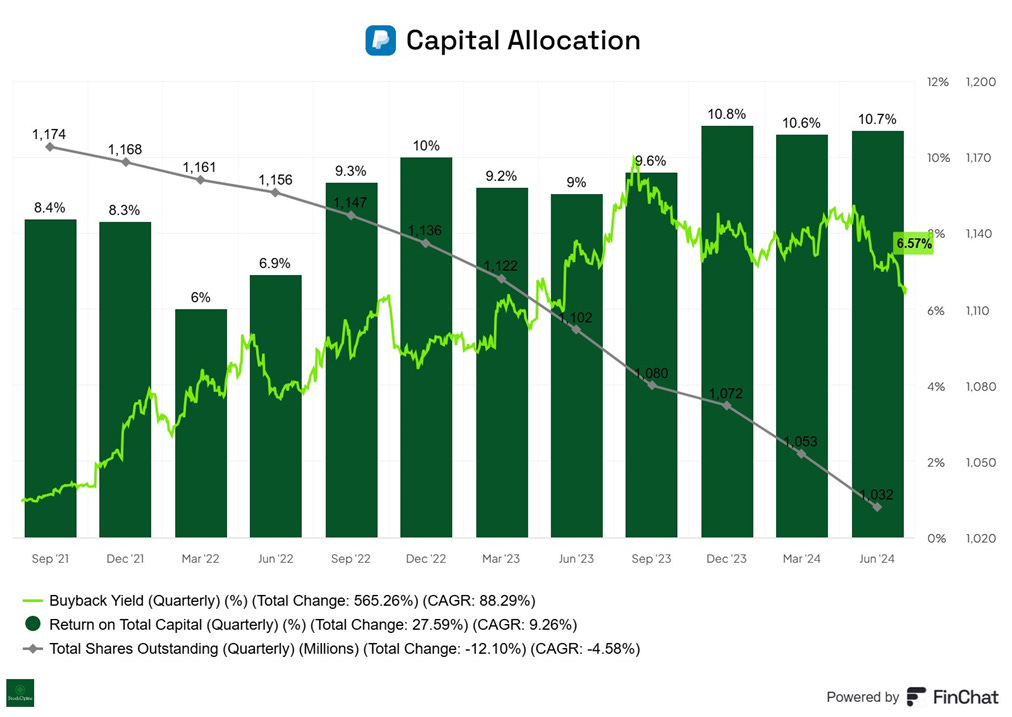

h. Financial position and Capital Allocation

PayPal maintains a healthy balance sheet, with $18.3 billion in cash, cash equivalents, and investments compared to $12.2 billion in debt. At the same time, the company has been delivering value to shareholders through share buybacks.

As shown in the chart below, PayPal ramped up its share repurchases in 2023, buying back $5 billion worth of shares compared to $4.2 billion in 2021 and $3.4 billion in 2020. This was done during a period when the stock was trading at depressed levels (around $65). In 2024, PayPal continued this momentum, repurchasing approximately $3 billion worth of shares with a target to buy back $6 billion by year-end, aligning with expected free cash flows. This capital allocation strategy has reduced the total number of shares by about 11% since June 2022, and returns on capital have recently improved to above 10%, supported by the company’s enhanced profitability.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Looking ahead, we expect returns on capital to continue improving as profitability increases and the company further reduces its share count given the $7.9 billion available for future repurchases.

2. Valuation

Having analyzed PayPal’s financials, we will now move into its valuation. First, we will do a Reverse DCF and discuss whether the growth implied in the current price is reasonable. Afterward, we’ll conduct a “sanity check” and conclude with our best estimate of the company’s fair value using a traditional DCF.

a. Reverse DCF

In our Reverse DCF, we maintained the operating margin in line with PayPal’s TTM non-GAAP operating margin of 18%, applied a tax rate of 21% (consistent with its statutory tax rate), and used a 10% discount rate (our required rate of return) as fixed variables. Based on these inputs, we derived an implied 10-year revenue growth rate of 5.8%, which is embedded in the current price as of September 24th, 2024.

Is this reasonable?

Considering that analysts project a +7% revenue growth over the next three years and the Digital Payments market is expected to grow at a 9.5% CAGR from 2024 to 2028, we believe the market is pricing in higher risk for PayPal, likely due to competitive pressures within the fintech space. It appears that pessimism is baked into the current valuation, despite the company’s execution under its new CEO and potential growth levers. For context, PayPal achieved a 14% revenue CAGR between 2018 and 2023.

Source: StockOpine analysis, Note: If you want to learn more about Reverse DCF and to download a model you can do so here.

b. Sanity check

This is a simple exercise in which we divide the market cap of each comparable company (the list is not exhaustive) to assess the value the market assigns to each dollar processed. For private companies, we used their latest reported deal valuations (see links below).

It’s important to clarify that not all processed dollars are equal. For instance, a dollar processed through PayPal’s branded checkout (with a higher take rate) is significantly more valuable than one processed via Venmo or Braintree. However, this comparison provides useful insights into potential outliers.

In our view, Stripe stands out (potentially overvalued?) at 6.86x compared to Adyen’s 3.68x. If you are interested to learn more about Adyen, you can refer to Adyen: Simplifying Payments with Top-Notch Quality.

Source: StockOpine analysis, Revolut, Stripe Valued at $70 Billion

With that context in mind, let’s move on to our DCF analysis to estimate PayPal’s price.