POOL Corp Q1'26: The Green Shoots Are Taking Root

A solid 6% top-line beat meets a highly cautious full-year guide

When we mapped out the expectations for Pool Corp’s Q1’26 print, the primary objective was clear: prove that the stabilization narrative from late 2025 was intact and that the Q4 earnings miss was merely a seasonal, weather-driven blip.

The company delivered exactly that, surpassing expectations on both the top and bottom lines. Net sales increased 6% to $1.1 billion in the first quarter of 2026. Diluted EPS came in at $1.45, representing an increase of 2% year-over-year. When excluding the impact of ASU 2016-09 tax benefits in both periods, adjusted earnings per diluted share actually increased by 8% to $1.43.

The quarter confirmed that the resilient maintenance base remains strong, while the discretionary side of the business is continuing its gradual recovery. Here is the breakdown of the key drivers.

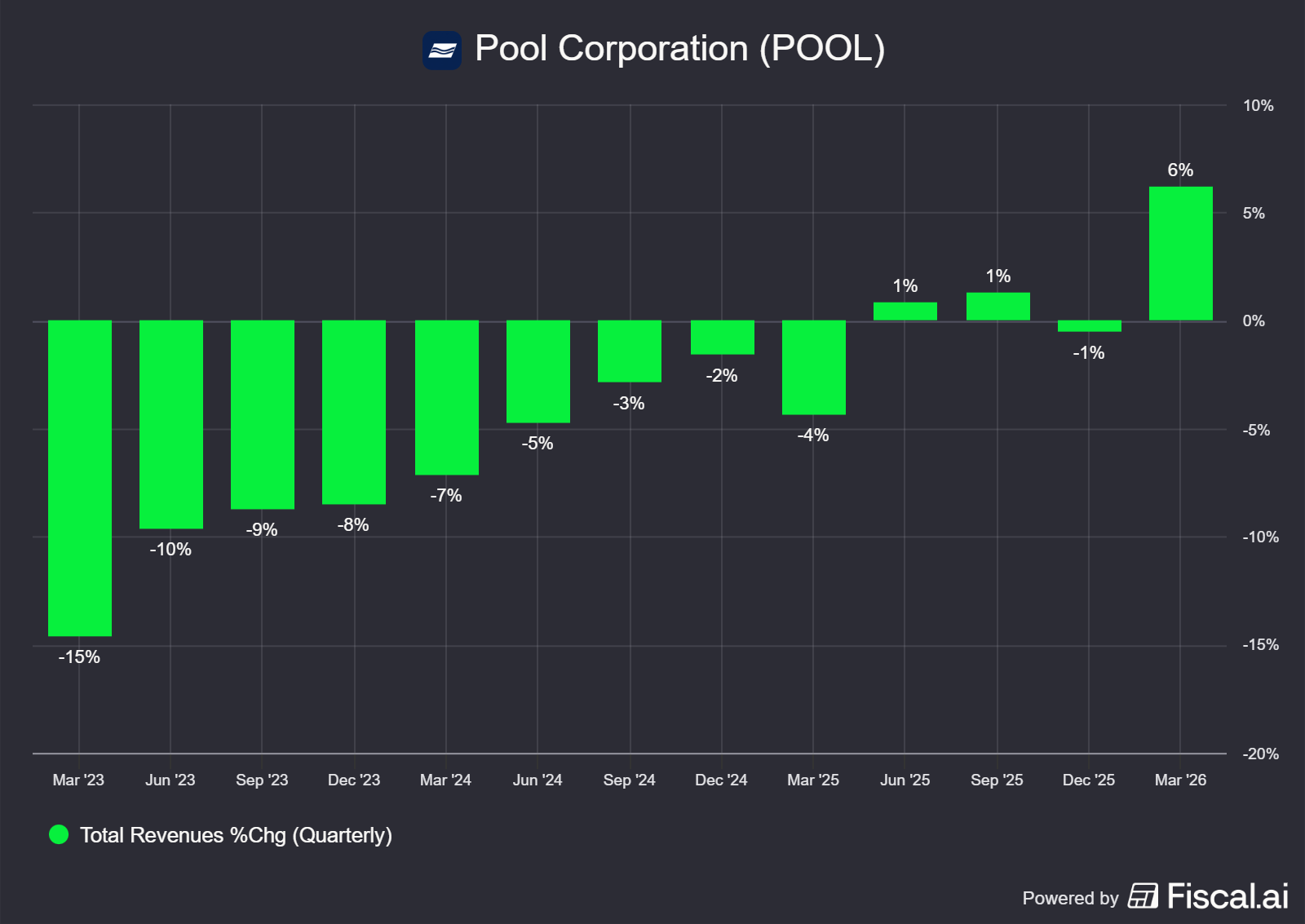

1. Revenue

The 6% top-line growth was a refreshing beat, driven by solid demand for maintenance products, strong equipment sales, and continued improvement in discretionary categories like building materials. This is the first meaningful acceleration after nearly 12 quarters of declines or flatness.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

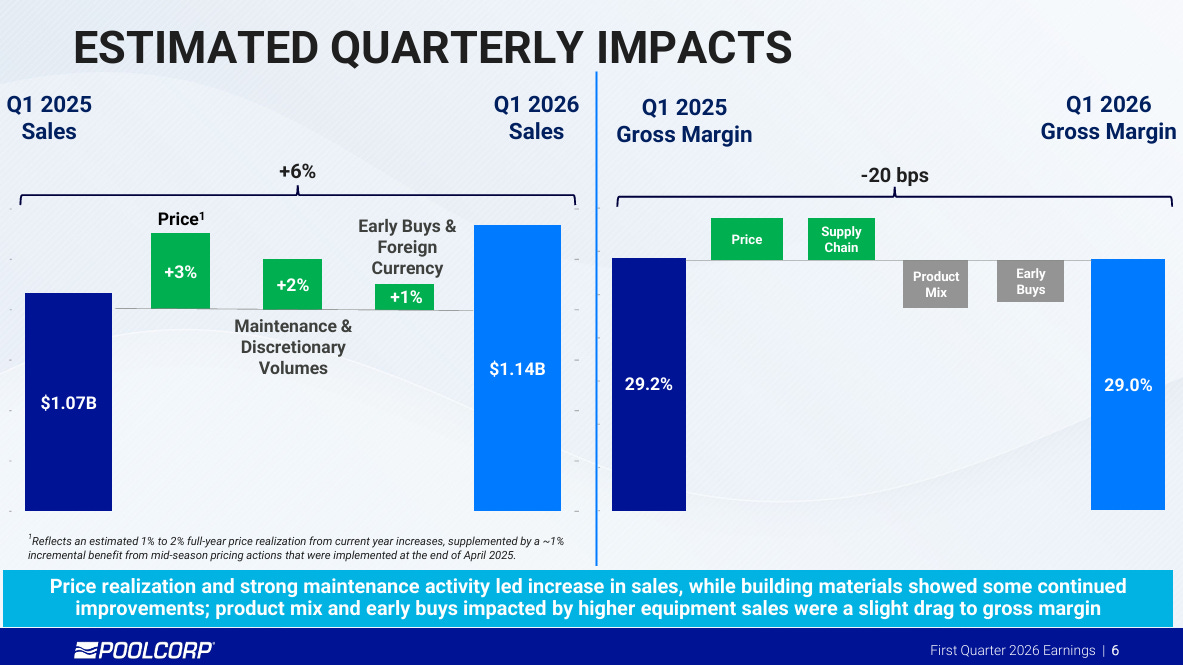

Breaking down the growth, the quarter benefited from approximately 3% from pricing, 2% from volume in maintenance and discretionary categories, and a 1% combined tailwind from customer early buys and favourable foreign currency translation. The pricing contribution reflects a 1% to 2% lift from current year increases, supplemented by a 1% carryover from mid-season price hikes implemented in late April of 2025.

Source: Pool Corporation Q1’26 Earnings Presentation

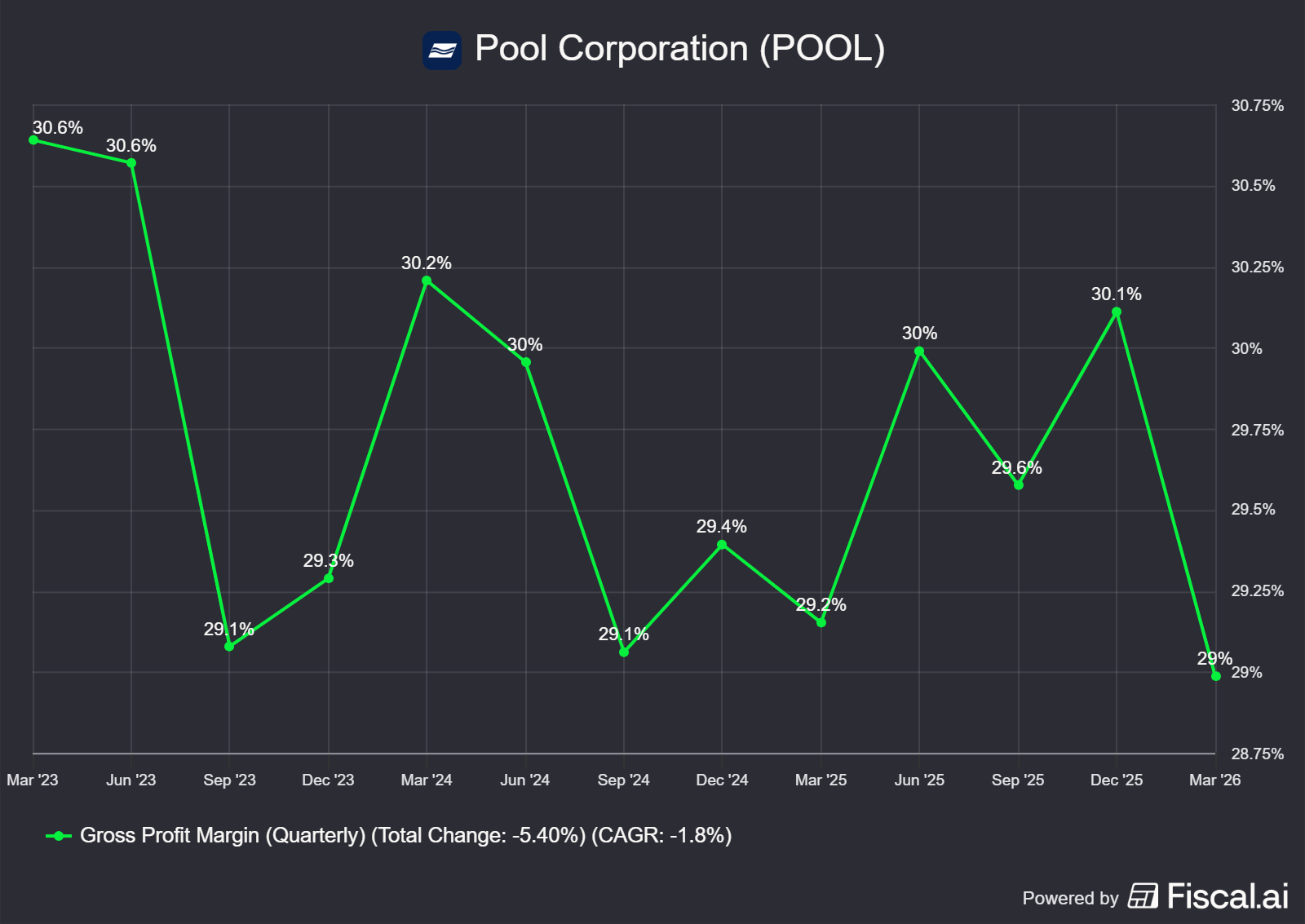

2. Gross Profit Margin

While gross profit dollars increased by $17.5 million, the gross margin percentage decreased by 20 basis points year-over-year to 29.0%. However, context is critical here. This contraction wasn’t due to a loss of pricing power.

The margin dilution was primarily driven by product mix, specifically a higher proportion of lower-margin equipment sales during the quarter. Additionally, Q1 saw an increase in customer early buy activity. While these early buys carry discounts that modestly pressure Q1 margins, they are a highly positive indicator that dealers are confidently stocking up for a strong core season. These headwinds were partially offset by ongoing pricing and supply chain optimization initiatives.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

3. Operating Margin and Potential Efficiencies

Operating margin expanded 10 basis points to 7.3% as operating income grew 7% to $82.6 million. Operating expenses increased 5% to $247.3 million, driven by the addition of six greenfield locations opened after Q1 of last year, technology investments, and general inflation.

Importantly, management expects the year-over-year expense growth rate to moderate in the coming quarters as the company laps prior-year investments and focuses on driving efficiency through its existing, expanded footprint. Therefore, if revenue continues to grow in the mid-single digit rate for the rest of the year, we should expect higher operating leverage going forward.

4. Performance by Product Category

The Q1 product mix provided several encouraging signals:

Building Materials: Sales grew +5%. This builds directly on the green shoots we identified in Q3’25, supported by the national pool trend offering and signaling further stabilization in remodeling activity. Additionally, given the muted construction market, it appears that Pool is actively gaining market share in this category.

Chemicals: Sales surged +8%. This strong volume growth was heavily supported by private label lines, which carry structurally higher margins. It is also worth noting that this category faced deflationary headwinds over the past few quarters. Management’s commentary indicates that pricing has stabilized, giving us the impression that the worst of the deflation is finally fading away.

Equipment: Sales grew +7%. This was driven by both price and solid volume, likely indicating a normalization of the replacement cycle for older installed components.

5. Regional and End Market Performance

Independent Retail & Pinch A Penny: Sales to independent retail customers grew 3%, setting up a solid foundation for the core season. The Pinch A Penny franchise network saw end-customer sales grow 4%, with franchisees opening seven new locations in the quarter.

Regional Performance: Favourable weather aided the West, with California growing 10% and Texas growing 7%. Conversely, Florida declined 1%, pressured by weather and some softness in irrigation, while Arizona grew 1%.

Commercial: Sales were flat for the quarter, largely due to project timing, but the segment exited Q1 showing slight growth.

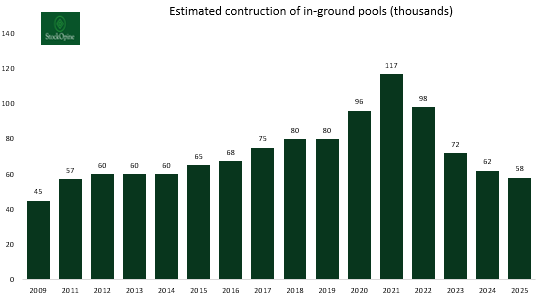

6. New Construction Vs Maintenance

Management noted that new pool units for 2025 came in at roughly 58,000, marking four consecutive years of decline in new pools built. Management expects 2026 to hover close to that same 58,000 unit mark. Holding near these 2011 levels gives us confidence that we have finally hit the bottom in the new construction segment.

Source: Pool Corp 10-K Filings, Pool Corp Earnings Transcripts, StockOpine Analysis

While expectations are for 2026 to stay flat, the long-term thesis relies on the 5.5 million in-ground pools already installed. As we have consistently tracked, this installed base generates recurring maintenance revenue, meaning Pool Corp’s growth does not strictly require a massive recovery in new pool construction to succeed.

Below paywall, we break down why the outlook is a classic ‘sandbag’ setup and our live portfolio actions….