POOL Corp Q3’25: Momentum Maintained, Building Materials Rebound

Maintenance remains resilient while discretionary shows first green shoots

POOL reported third-quarter 2025 results that continued the stabilization trend we saw in Q2. The operating environment remains challenging, with elevated interest rates weighing on high-ticket discretionary spending. However, the non-discretionary maintenance business provided a solid foundation, and the company delivered another solid performance.

The key takeaway this quarter is a story of confirmation and green shoots. While the discretionary side of the business remains soft, it shows clear signs of bottoming. For the first time since the third quarter of 2022, the company reported year-over-year growth in building materials, a key indicator for remodel and new pool activity. This, combined with a 50-basis-point expansion in gross margins and a confirmation of full-year EPS guidance, suggests that POOL is successfully navigating the trough of this cycle.

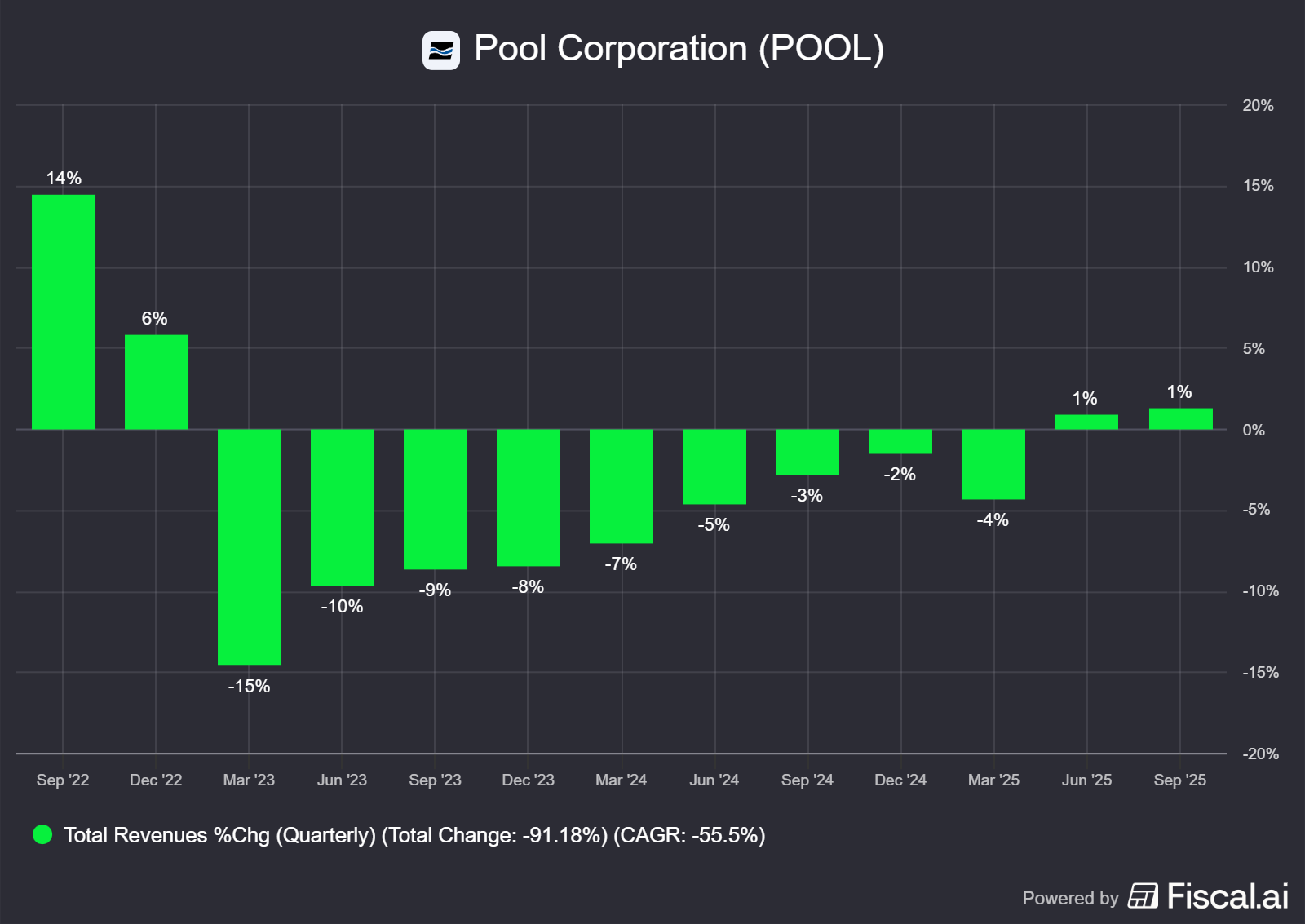

1. Revenue

Net sales for the quarter were up 1% year-over-year to $1.5 billion, building on the 1% growth established last quarter.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

This modest growth was driven by two key factors: a +1% contribution from the maintenance business and a +2% benefit from net pricing. The net price benefit itself was composed of a +3% gain from pricing actions offset by a -1% headwind from commodity price deflation in chemicals.

These gains were partially offset by a -2% drag from discretionary spending on new pools and remodeling. This is the exact same impact we saw in Q2, which strongly suggests that the decline in the discretionary business has stabilized and is no longer worsening.

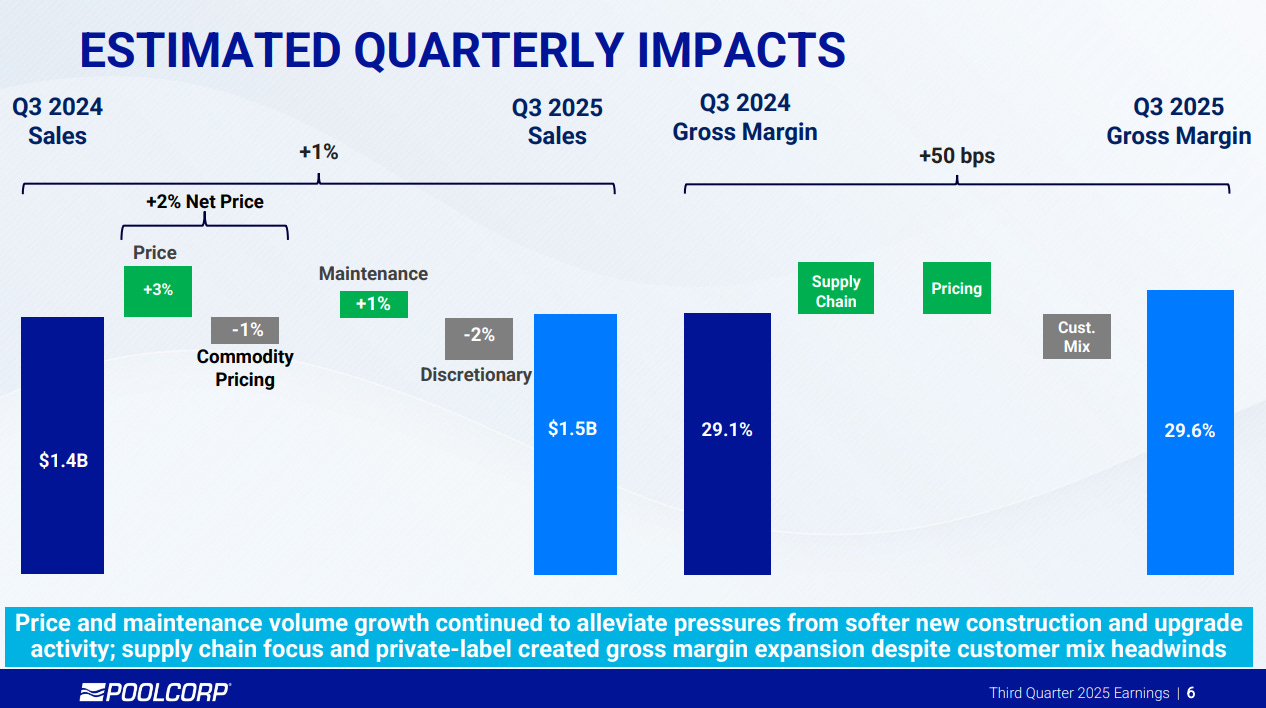

Source: Pool Corporation Q3’25 Earnings Presentation

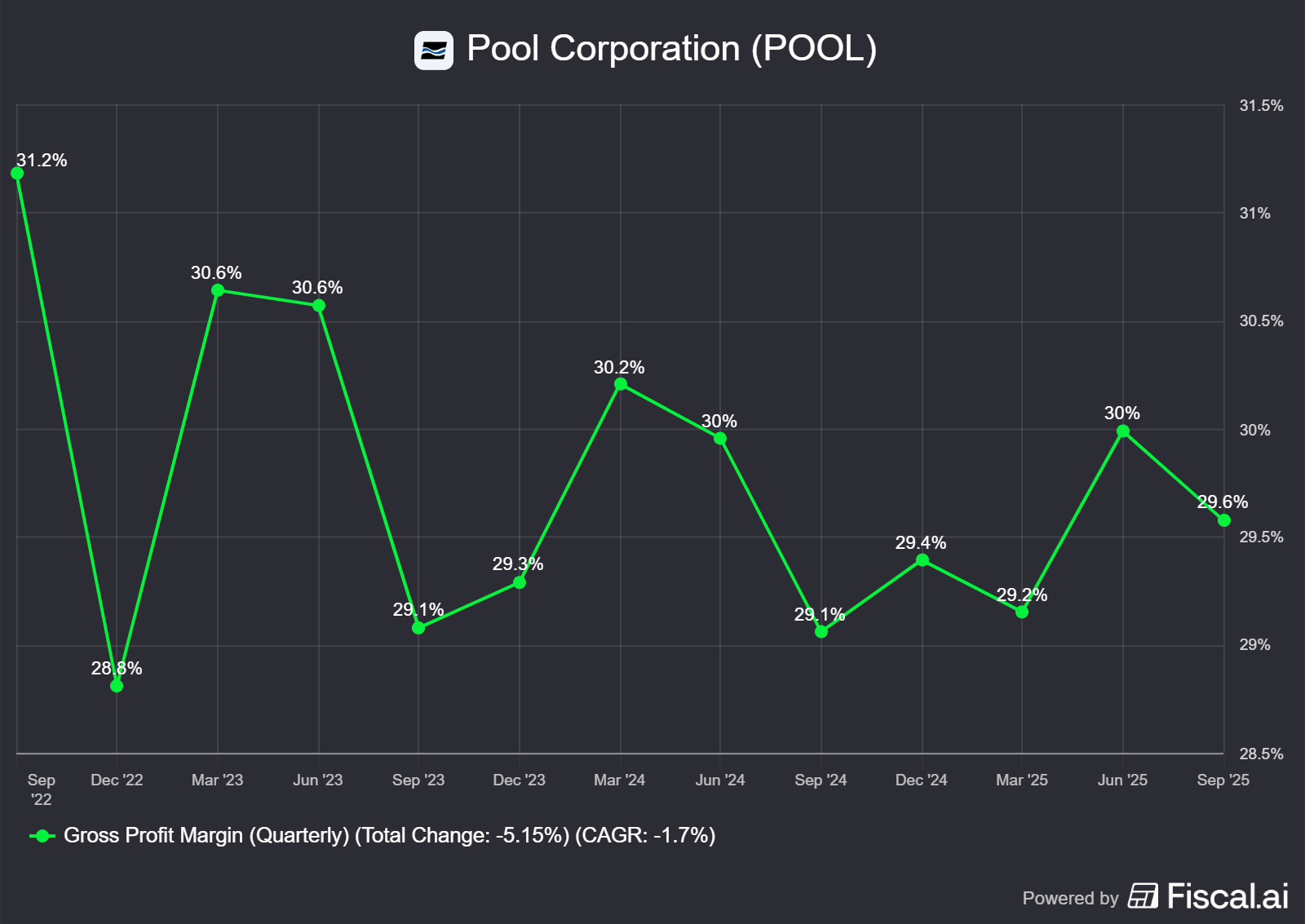

2. Gross Profit Margin

Gross margin for the quarter came in at 29.6%, a 50 basis point expansion compared to Q3 2024. This is a welcome improvement from the flat performance in Q2 and demonstrates strong execution in a tough environment.

The margin expansion was primarily driven by favorable pricing and successful supply chain initiatives. Growth in higher-margin private label products also contributed. These positive factors were strong enough to offset headwinds from an unfavorable customer mix and lower sales from more-profitable discretionary products.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

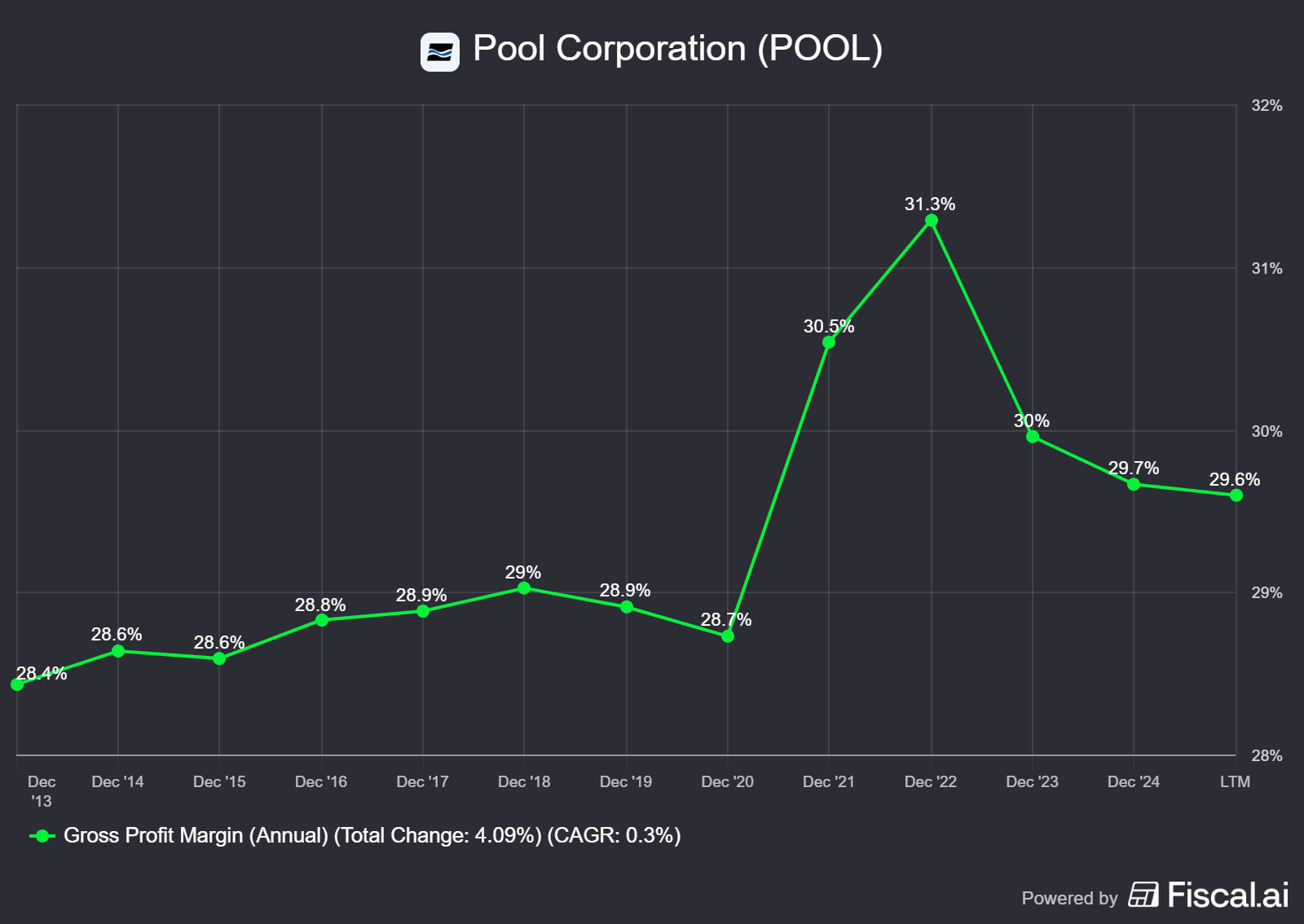

What’s impressive is that even with these discretionary headwinds and chemicals’ deflation, the company’s gross profit margin remains above pre-pandemic levels. This signals strong execution and durable pricing power. Once the current pressures from chemical deflation and the construction slowdown reverse, we see a clear path for gross margins to expand back at the 30% level.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)