While writing this post, a few thoughts naturally came to mind.

How do we explain a quarter of underperformance, and a roughly 10% gap versus the S&P 500 over this year, when the investing world on Substack and FinTwit seems full of people beating the market with ease?

What’s our edge? Should we view this as a short-term setback, or question whether our focus on quality compounders is outdated in a momentum-driven market?

These are serious questions we don’t take lightly, especially since we’ve committed to sharing our performance transparently. But this is exactly where conviction matters.

The question is: Are we here to chase what’s working now or to build wealth steadily by owning businesses we would be comfortable holding for decades?

With that mindset, we reviewed our portfolio closely this quarter and we closed two positions and added three new ones. Each move has strengthened our portfolio fundamentals and reinforced our confidence in the long-term trajectory.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers), StockOpine analysis

That said, periods of underperformance don’t mean we are not finding great ideas. Quite the opposite.

Our August idea, Micron, has surged from $117 to over $200 (+75% in two months).

Our April one, Teradyne, moved from $69.8 to $139 (+99%).

For transparency, we didn’t purchase Micron or Teradyne in our own portfolio, but we highlighted both as high-quality opportunities for readers. Not every idea fits our portfolio at the time, but we aim to turn every stone to uncover long-term winners.

Our AMD deep dive in March (buy at ~$100, now +140%) and June analysis on Google (then $166, up +50%) are proof that deep research pays off.

At StockOpine, our goal isn’t to predict every quarter but it’s to help you understand businesses deeply and make informed, long-term decisions. Whether you use our analysis to shape your own portfolio or view our portfolio directly on eToro*, our commitment remains the same: clarity, quality, and conviction.

(*eToro is a multi-asset investment platform. The value of your investments may go up or down. Your capital is at risk.)

Now, let’s dive in. But first, here’s a quick recap of the deep dives we shared this quarter, in case you missed any!

Deep Dives

1. Portfolio Performance

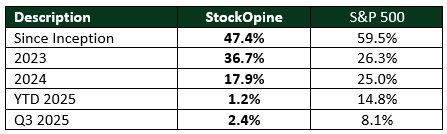

As of September 30, 2025, our portfolio returned +2.4% in Q3, underperforming the S&P 500 by 580 bps (index: +8.1%). Year to date, we are trailing the benchmark (+1.2% vs. +14.8%).

Since inception (January 28, 2022), our portfolio has delivered a +47.4% cumulative return (+11.1% annualized), compared with the S&P 500’s +59.5% over the same period.

Source: S&P Dow Jones Indices, Broker, StockOpine analysis

2. Portfolio Insights

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers), StockOpine analysis

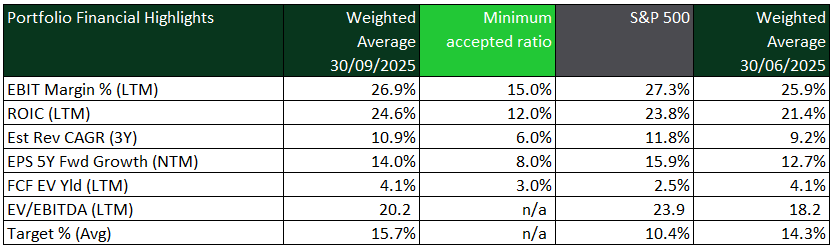

Our portfolio continues to meet the minimum quality thresholds we’ve set, showing improvement across all key metrics compared to Q2 2025. ROIC improvement is notable, as two of our new positions have ROICs above 40%, driving the average higher. In terms of valuation, the increase in EV/EBITDA may appear negative at first glance, but free cash flow yield remains stable, and analyst target prices have risen from the prior quarter.

When compared to the S&P 500, our portfolio trails slightly in profitability (26.9% vs. 27.3%) and revenue/EPS growth (11.8% and 15.9%, respectively). However, it now has a higher ROIC of 24.6% vs. 23.8%. From a valuation standpoint, our portfolio has a 4.1% free cash flow yield versus 2.5% for the index and trades at an EV/EBITDA multiple of 20.2x, roughly 15% below the S&P 500. At the same time analysts’ expect higher upside of 15.7% vs. 10.4% for the index.

All in all, we hold businesses well-positioned for long-term value creation.

Winners and losers

As of September 30, 2025, the portfolio consists of 20 stocks,