This Month’s Stock Idea Is Out!!

Each month, StockOpine Premium members receive a well-researched stock idea, delivered straight to their inbox. This week, we released our August 2025 idea.

👉 To give our free subscribers a taste of what’s behind the paywall, we’re unlocking one of our past ideas: Teradyne (April 2025). Since our original write-up, the stock has surged +65%, a clear example of the kind of opportunities we aim to spot early.

But remember, by the time free readers see these ideas, the move may already be well underway. Don’t miss the next Teradyne. Upgrade today and get access to our August pick immediately.

As a bonus, here’s an exclusive 25% lifetime discount for our free readers.

Below, you’ll find the full April 2025 Teradyne write-up, exactly as it was shared with Premium members.

Finding a great investment idea isn’t easy, but that’s exactly what we aim to deliver each month.

Each edition highlights a compelling opportunity from our coverage universe, focusing on catalysts we believe can drive share prices higher and deliver long-term returns.

This month, we’re featuring a niche market leader in the semiconductor supply chain, currently trading 57% below its 52-week high. The drop stems from softer 2025 guidance, impacted by tariff-related uncertainty that has affected nearly every company in the sector.

Despite near-term headwinds, the company’s fundamentals remain strong:

EBIT margins have averaged 23% over the past decade (currently lower)

Return on invested capital (ROIC) has averaged 22%, now closer to 18%

Revenue CAGR: 6.2%

Operating income CAGR: 9.1%

Net income CAGR: 11.3%

EPS CAGR: 14.9%

Total shareholder return over the past decade: +302.7% (~15% CAGR)

This performance shows that price has closely followed earnings per share growth.

However, since the company’s Q4 results announcement and the revised 2025 outlook, valuation multiples have compressed significantly, by roughly 35–40%. It now trades at:

EV/EBITDA (NTM): 14.5x

P/E (NTM): 21.6x

These multiples might not scream "deep value," but in a duopoly, a premium valuation is both expected and deserved.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

Contents:

The business

Valuation

Catalysts

Risks

Teradyne Inc. ($TER) - Market Cap: $11.2 Billion (as of 21st April 2025) – Share Price $69.8

1. The business

Company Overview

Teradyne, founded in 1960, designs, develops, manufactures, and sells automated test equipment (ATE) and industrial automation (IA) solutions globally. Its test systems are used across semiconductors, wireless products, data storage, and complex electronic systems. On the robotics side, Teradyne offers collaborative robotic arms and autonomous mobile robots (AMRs) for global manufacturing, logistics, and industrial customers. The company plays a critical role in ensuring high-performance, reliable electronic products and semiconductors.

Customer concentration is significant as Teradyne derived ~36% of revenue from its top five customers in 2024 (up from 32% in 2023). Samsung (including its OSAT partners) was the largest customer at 12.5%. In previous years, Texas Instruments (2023) and Qualcomm (2022) topped the list. It’s worth noting that Teradyne is the only US-based test company capable of testing the most advanced semiconductors.

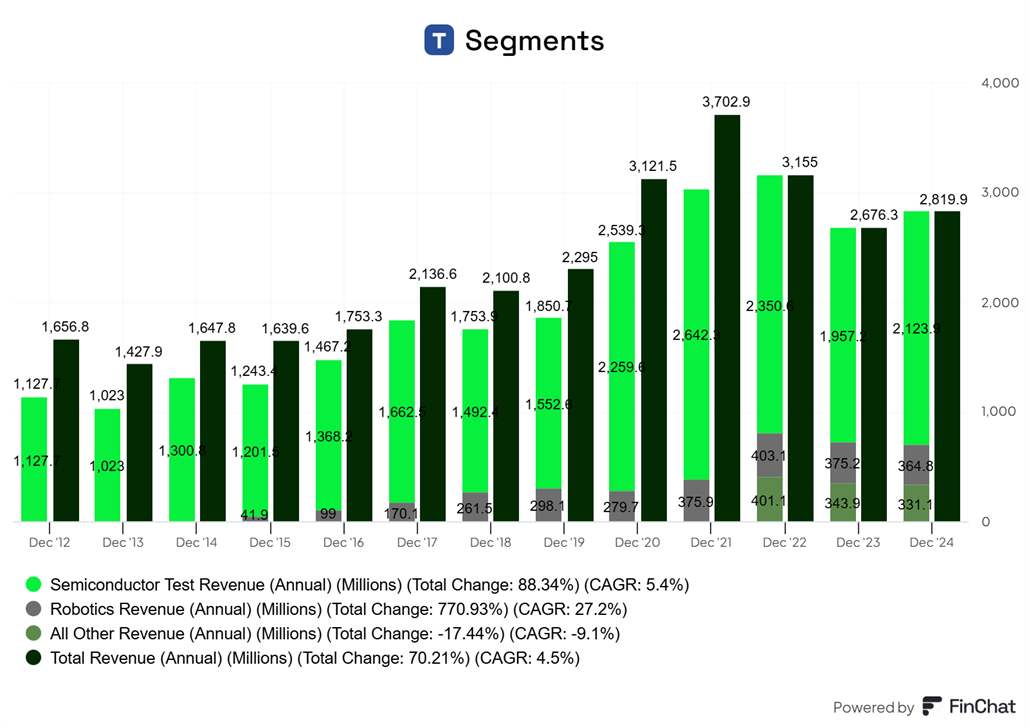

Segments

Semiconductor Test (ATE): Teradyne’s largest segment (~75% of 2024 revenue) provides test solutions for SoC, memory, analog, and wireless semiconductors. It operates in a cyclical industry tied to semiconductor capital expenditure and is effectively part of a global duopoly with Advantest (market share of +50% Vs +35% for Teradyne). Growth is driven by rising chip complexity across computing (especially AI), automotive (ADAS), and memory (HBM DRAM).

2024 Revenue: $2,124M, up 12.5% | Q4 2024: $561M, up 28%

13% YoY SoC revenue growth (excluding DIS divestiture), driven by mobile and continued momentum in compute, driven by AI

Memory was up 30% YoY, led by demand for HBM DRAM

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers) / Note: In Q4 2024, Teradyne consolidated its segment reporting into two groups —> Semiconductor Test and Robotics & Other. Historical comparisons may vary.

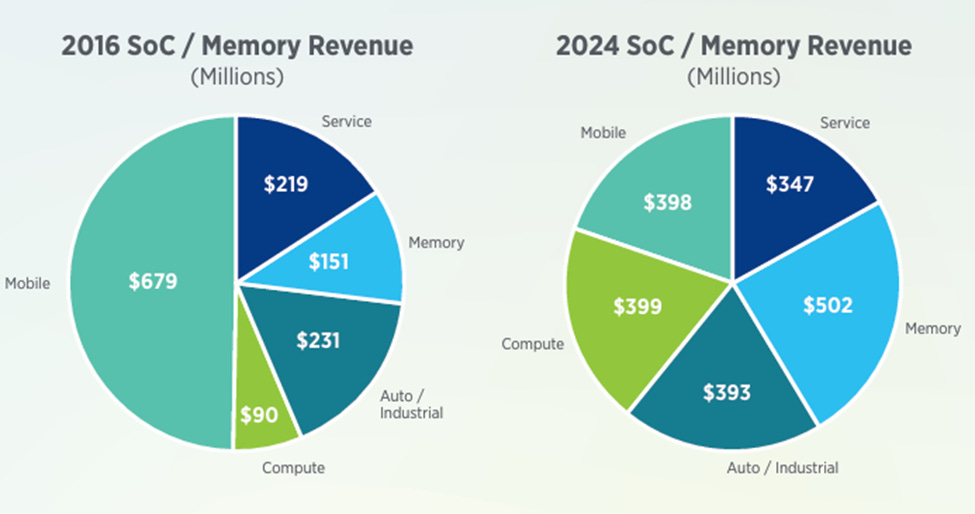

According to management, 2024 marked an inflection point following two years of declines. The business is now less dependent on mobile, which once accounted for half of revenue in 2016 but now stands closer to 20%. Compute and memory revenues have grown 4.4x (3.5x times 2023 revenue) and 3.3x respectively since 2016, helping diversify revenue verticals.

Source: 2024 Annual letter to shareholders

Robotics (Industrial Automation): Built through acquisitions like Universal Robots (UR - collaborative robots/cobots) and Mobile Industrial Robots (MiR - autonomous mobile robots/AMRs), this segment contributes ~13% of 2024 revenue. These solutions target automation across manufacturing, logistics, and warehouse operations. Although adoption is in early stages and the competitive landscape is fragmented, Teradyne outperformed a declining market.

2024 Revenue: $365M, down 3% | Q4 2024: $98M, down 24%

Declined 3% YoY versus a 13% drop in the broader industrial automation market. It has outperformed peers 8 of the 9 years in the past and claims to have the highest gross margins due to product differentiation

Other (Product Test): This includes System Test (Defense/Aerospace, Production Board Test) and Wireless Test and accounts for ~12% of 2024 revenue.

System Test was flat at $201M

Wireless Test declined to $130M

Combined segment revenue dropped 4% YoY due to continued market weakness

Geographically, key revenue contributors in 2024 were Korea (25%) and Taiwan (21%), followed by the US and China (13% each).

Profitability

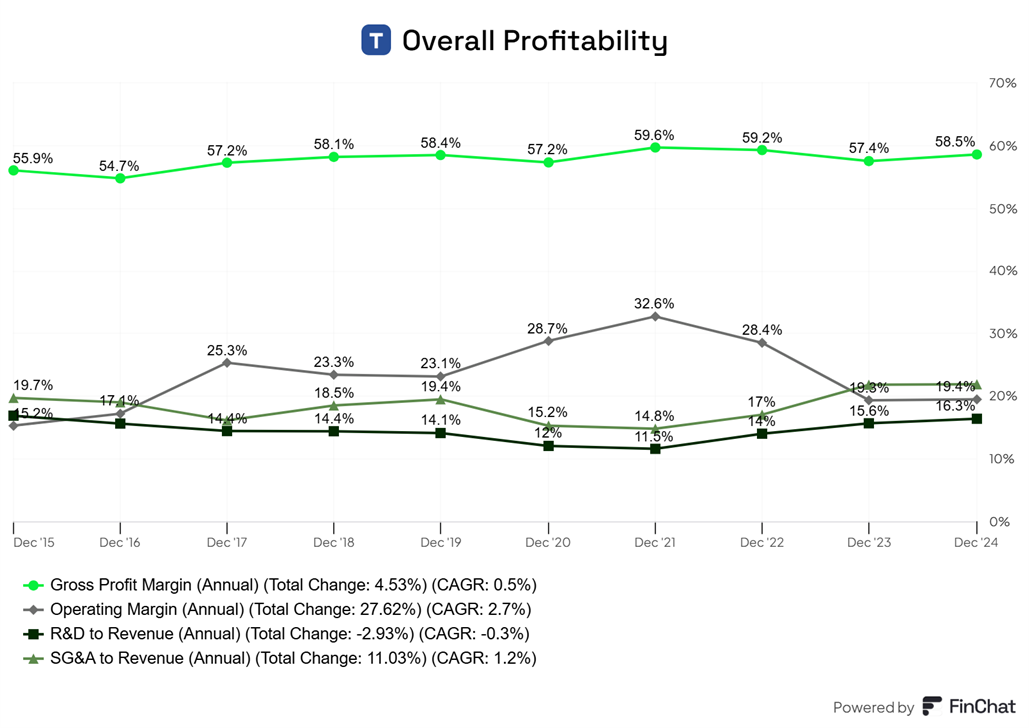

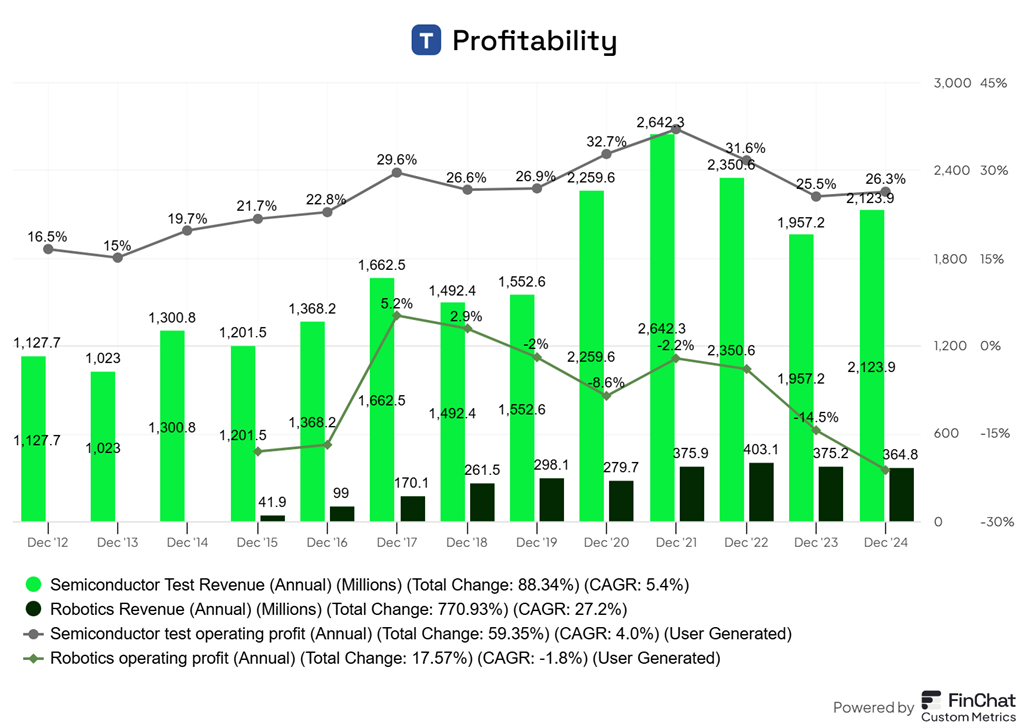

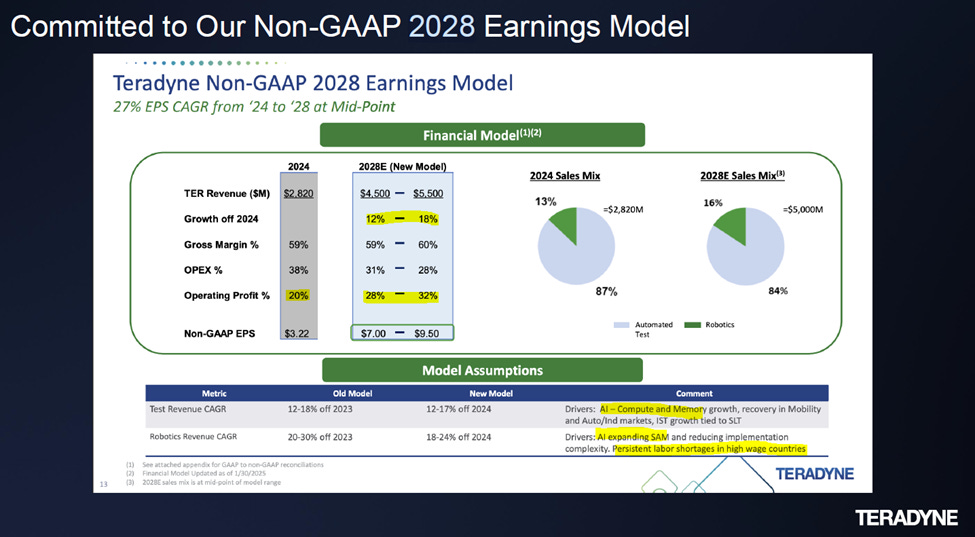

Teradyne maintains strong profitability, especially in the ATE segment, due to its technological edge. Gross margins reached 58.5% in FY2024, up from 57.4% in 2023, though slightly lower than the 2022-2021 peak levels which exceeded 59%. Margins are sensitive to industry cycles but have consistently remained above 57% since 2017. Operating margins peaked during 2020–2022 with high sales but normalized to 19% in 2023. By 2028, management expects that Operating margin will exceed 28% on a non-GAAP basis from 20.4% in 2024. A key factor in sustaining its leadership is heavy investment in R&D, with annual spend exceeding 15% of revenue.

Robotics is currently loss-making, but management has restructured its cost base, lowering the break-even revenue threshold from $440 million to $365 million. As a result, the segment is expected to break even in 2025, compared to consistent losses in prior years.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

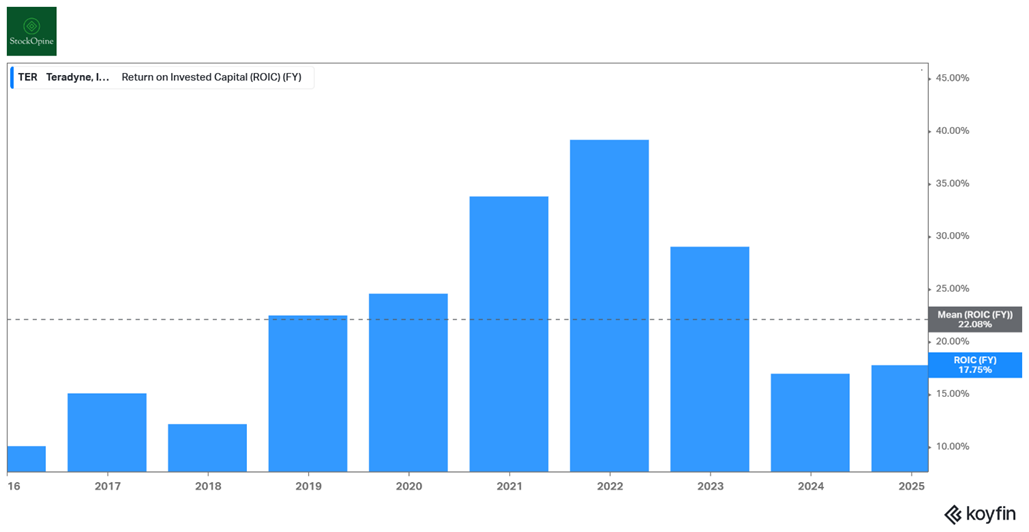

Return on Invested Capital (ROIC)

Teradyne has consistently delivered high ROIC through the cycle. For the twelve months ending December 2024, ROIC was 17.8%, down from its 2021 peak of 39.2%, but still above the PHLX Semiconductor Sector average of 17.1%. The company’s five-year average ROIC from 2020–2024 stands at approximately 27.3%.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial) / 2025 shown above is 31/12/2024

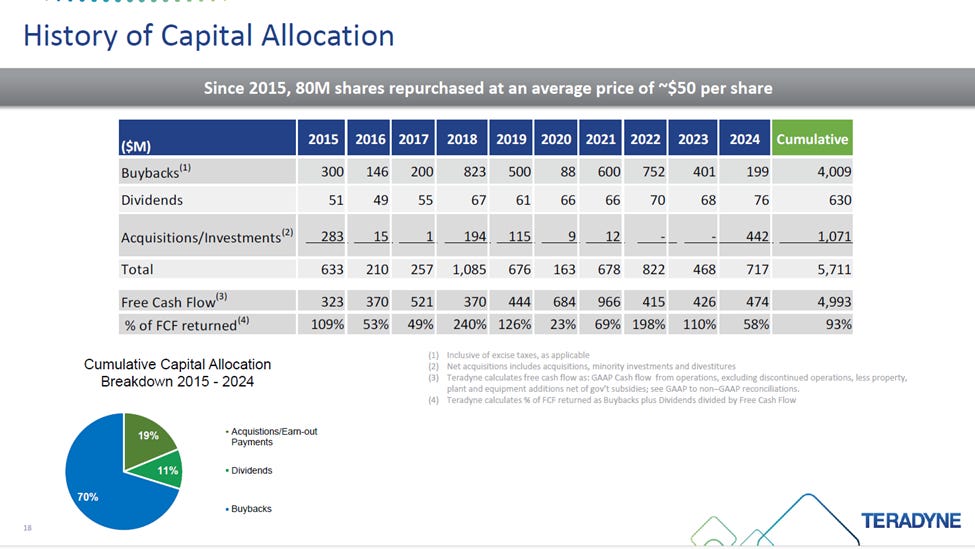

Capital Allocation

The company follows a disciplined capital allocation strategy, prioritizing R&D investment, moderate capital expenditures (around 5.4% of sales over the past decade, 7% in 2024), strategic acquisitions, and shareholder returns. Notable acquisitions include UR, MiR, and the pending acquisition of Quantifi Photonics (expected to close in Q2 2025). Teradyne also strengthened its power semiconductor test capabilities via a strategic partnership with Infineon, which included acquiring Infineon’s ATE team in Germany, an important move for EV and renewable energy chips.

The company continued share repurchases under a $2 billion program announced in January 2023, buying back $199.4 million in 2024 at an average price of $114.63 (Vs $400.5 million in 2023 at $102.50). Meanwhile, it plans to repurchase $400 million in 2025. Teradyne also pays a $0.12 quarterly dividend, yielding 0.69%. Through 2015 to 2024, 93% of free cash flow was returned to shareholders. Notably, share repurchases totaling $4.0 billion over this period resulted in a one-third reduction in shares outstanding; an aggressive capital return strategy often seen in so-called "capital cannibals".

Source: Teradyne Earnings presentation Q4’24

Balance sheet

Teradyne has a strong balance sheet, with $599.7 million in cash and short-term investments and no debt beyond $76.7 million in lease liabilities, providing flexibility to support growth.

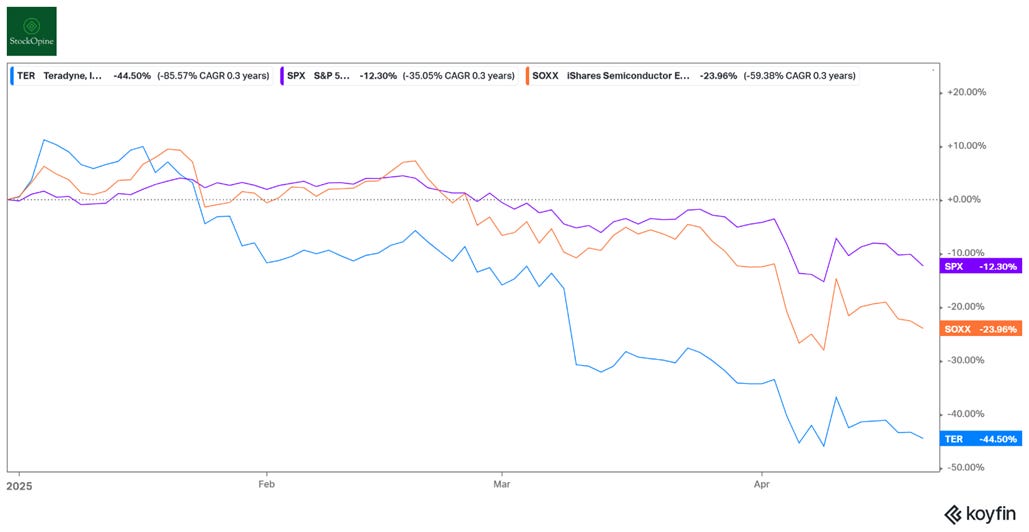

Recent Stock Price Decline

The company’s stock has significantly underperformed both the market and semiconductor sector in 2025. A major factor was the weaker-than-expected Q1 2025 guidance issued in January, with projected revenue of $680 million at the midpoint, sequentially down from $753 million in Q4 2024. Further pressure came from an uptick in R&D expenses in Q4 2024 by 25.6%, which did not yield proportional revenue growth in the Robotics segment. This raised investor concerns about the efficiency of capital deployment and potential margin pressure.

This was followed by additional downward revisions during the March Analyst Day, including lowered expectations for Q2 2025 and full-year 2025 growth. The revised Q2 guidance projected flat to -10% sequential growth versus the earlier estimate of 5–10% growth, and full-year 2025 revenue guidance was reduced from mid-teens growth to 5–10%.

A concern is that H2 2025 revised guidance embeds a 14.4% year-over-year growth assumption, which is viewed as overly optimistic given recent headwinds. Management during the analyst day, cited delays in customer project timelines and capital expenditure reviews rather than outright cancellations, largely attributed to uncertainties around tariffs, trade restrictions, and export controls.

In response to the softer near-term outlook, multiple analysts downgraded the stock and lowered their target prices. The average price target declined from around $137 in March 10th to approximately $111 by today, contributing to a continued downward spiral in the stock. Nevertheless, consensus remains optimistic on Teradyne’s long-term strategic positioning.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

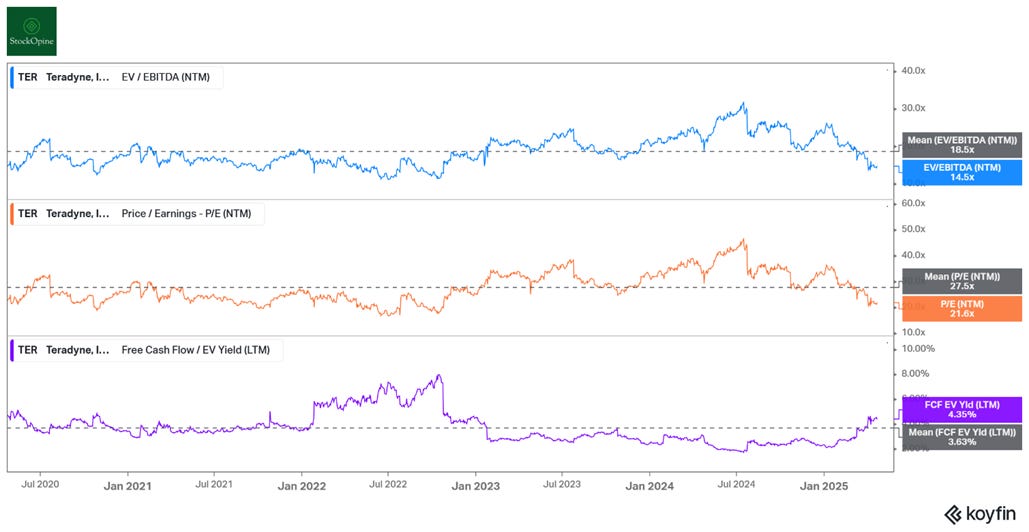

2. Valuation

Teradyne’s stock closed at $69.80 on April 21, 2025, with a 52-week high of $163.20 and a low of $65.80. Its year-to-date performance stands at -43%, while the current analyst price target of $111 implies a potential upside of approximately 59%.

The company currently trades at the following valuation multiples:

EV/EBITDA (NTM): 14.5x (vs. 5-year average of 18.5x)

P/E (NTM): 21.6x (vs. 5-year average of 27.5x)

Free Cash Flow / EV yield (LTM): 4.36% (vs. 5-year average of 3.63%)

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Looking ahead, consensus estimates project EPS growth of 19.7% annually over the next five years (in line with management expectations of doubling EPS by 2028), implying a PEG ratio of 1.1x. This growth suggest that current valuation multiples are not excessive. For comparison, the SOXX ETF, which tracks the 30 largest U.S. semiconductor firms, has an average P/E of 21.8x, EV/EBITDA of 14.9x, and FCF/EV yield of 4.0%.

While these multiples don’t scream "cheap" for a company like Teradyne with consistently strong returns on capital, a dominant position in ATE, and long-term optionality through robotics, trading at market-average multiples appears conservative.

Another lens to view valuation is through free cash flow. Assuming a 10% required rate of return and FY2024 free cash flow of $474 million, the market is currently pricing in a 5.3% perpetual FCF growth rate (using the formula: g = r – (FCF (1+g) /EV)). This assumption appears conservative, given Teradyne’s internal target of $1.255 billion in FCF by 2028, representing a 27.6% CAGR over four years, driven by operating leverage and its 2028 earnings model. Of course, free cash flow and earnings are cyclical, but today’s valuation is no longer a premium one. When a company in a duopoly trades at just 9x its expected 2028 free cash flow, it’s difficult to argue it’s expensive.

Source: Teradyne’s March 2025 analyst presentation

3. Catalysts

We believe that mid-to-long-term catalysts are in place to eventually drive revenue and EPS growth, potentially reversing Teradyne’s recent downward price trend. However, near-term catalysts are limited. That said, we see three potential developments that could impact the stock over the next 6–12 months.

First, a shift in tariff policy could provide a broader lift to the semiconductor sector.

Second, an optimistic tone during the upcoming earnings call on Monday, April 28, 2025, could act as a short-term catalyst. If management raises its outlook for Q2, the full year, or even 2026 EPS, the stock could rebound. Conversely, any confirmation of prolonged recovery delays, an increasingly realistic scenario given ongoing uncertainty, would likely drive the stock lower.

Third, visible progress on the Robotics profitability plan could help restore investor confidence in the segment. Management has made it clear that their goal is not just growth, but profitable growth:

“And criteria #2 is that we're here to make money, that having this growth happen without translating into operating margin is not particularly interesting.”

Their ambition to become the #1 player in collaborative and mobile robotics hinges on achieving sustainable margins.

Mid-Long term Catalysts

Vertically integrated customers/partners: These are companies that own the full hardware stack and design their own custom AI accelerators or processors. Examples include Google’s TPUs for AI workloads, Amazon’s Graviton, Trainium, and Inferentia chips, as well as Meta’s MTIA and Tesla’s self-driving chips. These are highly complex, next-generation chips, and as hyperscalers deepen their involvement in chip design and production, they require advanced and reliable test solutions, like those provided by Teradyne, to ensure performance and efficiency.

Importantly, these AI-driven customers tend to have more durable business models than traditional cyclical players, expanding Teradyne’s addressable market. Today, 9 of the top 12 companies by market cap are involved in AI, and Teradyne counts 8 of those 9 as customers in its Semiconductor Test business, some with 100% share. On the Product Test side, it serves 4 of them, and 3 are Robotics partners or customers.

What’s the runway? It’s not just about testing semiconductors anymore, there’s growing demand for testing final products as well. Add to that the rapid pace of product cycles, and Teradyne’s advanced robotics solutions are increasingly relevant. This all points to a long and compelling growth runway.

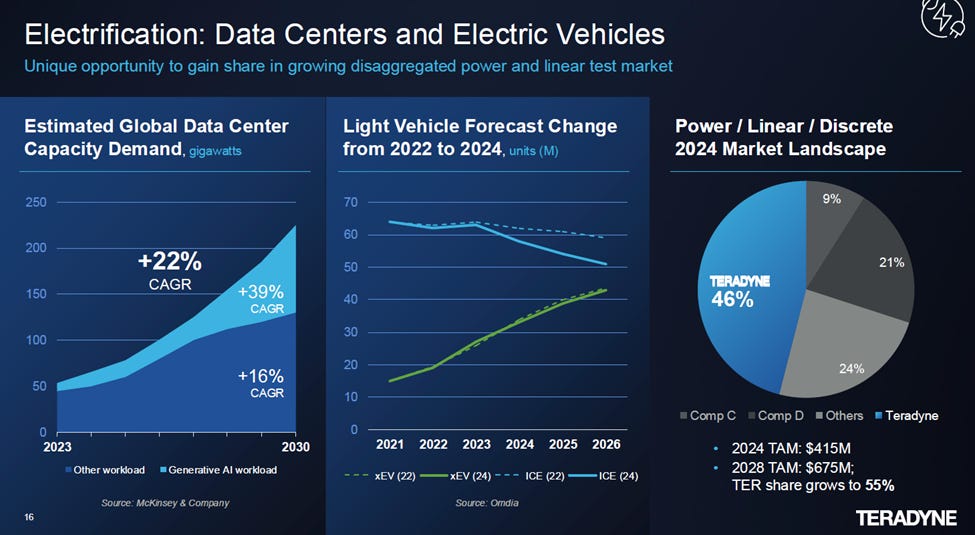

Electrification (Automotive & Infrastructure): The rise of renewables, electric vehicles, and data centers underscores the growing demand for power, particularly efficient, high-performance semiconductors. As illustrated in the chart on the left, data center gigawatt capacity demand is expected to quadruple by 2030. This surge will drive demand from hyperscalers, utilities, and infrastructure providers for power semiconductors based on gallium nitride (GaN) and silicon carbide (SiC), materials that offer superior efficiency and thermal performance.

This is where Teradyne’s acquisition of Infineon’s ATE team in Germany comes into play. The team enhances Teradyne’s capabilities in power semiconductor testing, a key enabler for this next-generation infrastructure.

On the automotive side, the second chart highlights the projected growth in electric vehicles, another secular driver for Teradyne. EVs typically contain twice as many semiconductors as internal combustion engine vehicles, and they increasingly rely on GaN and SiC chips to maximize range and minimize charge time. The Infineon ATE team brings expertise in discrete power testing, a specialized area that supports this transition.

The third chart brings it all together; Teradyne’s Power/Linear and Discrete segment. From a 46% share in a $415M TAM, Teradyne aims to grow to a 55% share in a $675M TAM, reinforcing the long-term growth potential in electrification-linked testing solutions.

Source: March 2025 Teradyne’s analyst day presentation

Pervasive application of AI: In semiconductor testing, AI drives demand for more advanced chips, particularly in compute, DRAM, and networking, and is expected to expand into mobile, automotive, and storage. This trend has already created opportunities in high-bandwidth memory, where Teradyne has gained share.

Looking ahead, the rollout of edge AI (e.g., smartphones with on-device AI capabilities) is expected to further expand Teradyne’s TAM in mobile. Key enablers include next-gen technologies like 2nm nodes and LPDDR6 memory. As of 2024, only around 15% of smartphones, just over 200 million, are AI-enabled, and many still lack compelling user experiences. However, by 2028, penetration is expected to reach approximately 70%, or ~900 million units, significantly boosting semiconductor complexity and driving a recovery in mobile-related memory testing demand.

In robotics, AI is transforming product functionality, enabling smarter, more adaptive automation. For example, the new MiR Pallet Jack uses AI to recognize and handle pallets even if they are damaged, wrapped, or obscured, improving reliability and unlocking broader use cases. Robotics revenue driven by AI grew from $1 million in 2023 to $11 million in 2024, with expectations to exceed $150 million by 2028.

Internally, AI is also enhancing Teradyne’s operations, improving service delivery, product development, and process efficiency. With exposure to AI-driven growth in the cloud, at the edge, and within enterprise operations, Teradyne is uniquely positioned to benefit across the full AI adoption cycle.

Shareholder Returns: Ongoing commitment to returning cash via dividends and buybacks provides support for total shareholder return.

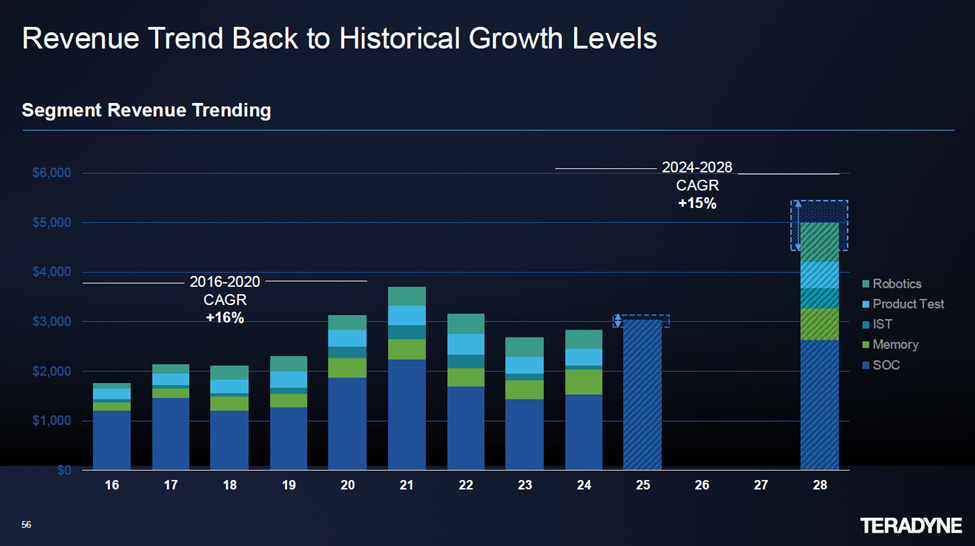

For context, the following slides, shared during the March 2025 Analyst Day, outline Teradyne’s growth expectations, including a 15% revenue CAGR, operating margins exceeding 30%, and free cash flow projected to surpass $1 billion by 2028.

4. Risks to Consider

Semiconductor Industry Cyclicality: Teradyne's financial performance is closely tied to the inherently cyclical nature of the semiconductor industry, which leads to fluctuating demand for Automated Test Equipment and challenges in forecasting revenue. As such, assumptions in valuation models can quickly become outdated. On the bright side, secular growth trends in AI, electrification, and robotics may help the company better weather future downturns.

Geopolitical and Trade Uncertainty: Tariffs, export controls, particularly US restrictions targeting China, and general trade tensions continue to cloud visibility and reduce addressable markets. The impact is evident: in 2021, Teradyne and Advantest each held around 40% market share, but Teradyne has since ceded share as approximately $1 billion in China business shifted away due to US regulation.

Competitive Pressure: Although Teradyne operates in a duopoly with Advantest in ATE, competitive dynamics remain fierce. Beyond China, a key driver of share loss since 2021 has been lagging performance in the compute segment, where Advantest outpaced Teradyne. While Teradyne led during the mobile era, it's now playing catch-up in the AI era. In robotics, competition is even more fragmented, with major industrial automation firms and agile startups fighting for share. That said, Teradyne remains focused on profitable growth and retains the flexibility to exit unprofitable initiatives if necessary.

Customer Concentration: Teradyne relies heavily on a small number of large customers, particularly in compute and mobile. Changes in these customers’ investment plans or market position can materially impact Teradyne's results. That said, with the top five customers accounting for 36% of revenue, the concentration is notable but still within a manageable range.

Leadership Transition: Rick Burns, president of the Semiconductor Test division (which represents ~75% of total revenue), will retire on June 1, 2025. He has been with the company since 2007 and led the division since 2020. His departure introduces potential execution risk. However, his successor, Shannon Poulin, former COO of Altera and a 22-year Intel veteran, brings deep compute expertise. Greg Smith CEO stated, “We wanted someone who knew compute inside and out, and that’s what Shannon is delivering”.

Now for the engaging part, a couple of questions to make sure you like this format (and improve it if needed), plus a question to help track your expectations on the stock’s future returns.