Let’s be honest, selling a high-performing stock is never easy, and it’s rarely our first choice. We prefer to hold quality businesses long-term. But when valuation stretches, and we find an alternative with what we believe is a realistic 50% upside in the next 12 months, it’s time to act.

To be fair, this company has executed impressively. Over the past five years, revenue grew at a 15.6% CAGR, operating margins expanded from the 30% range to the 40s, and free cash flow grew 17.6% annually. It’s a top-tier performer.

Still, the stock has rerated significantly. With the P/E now above 31x, nearly double the ~16x when we first bought, we think the risk/reward is no longer compelling.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

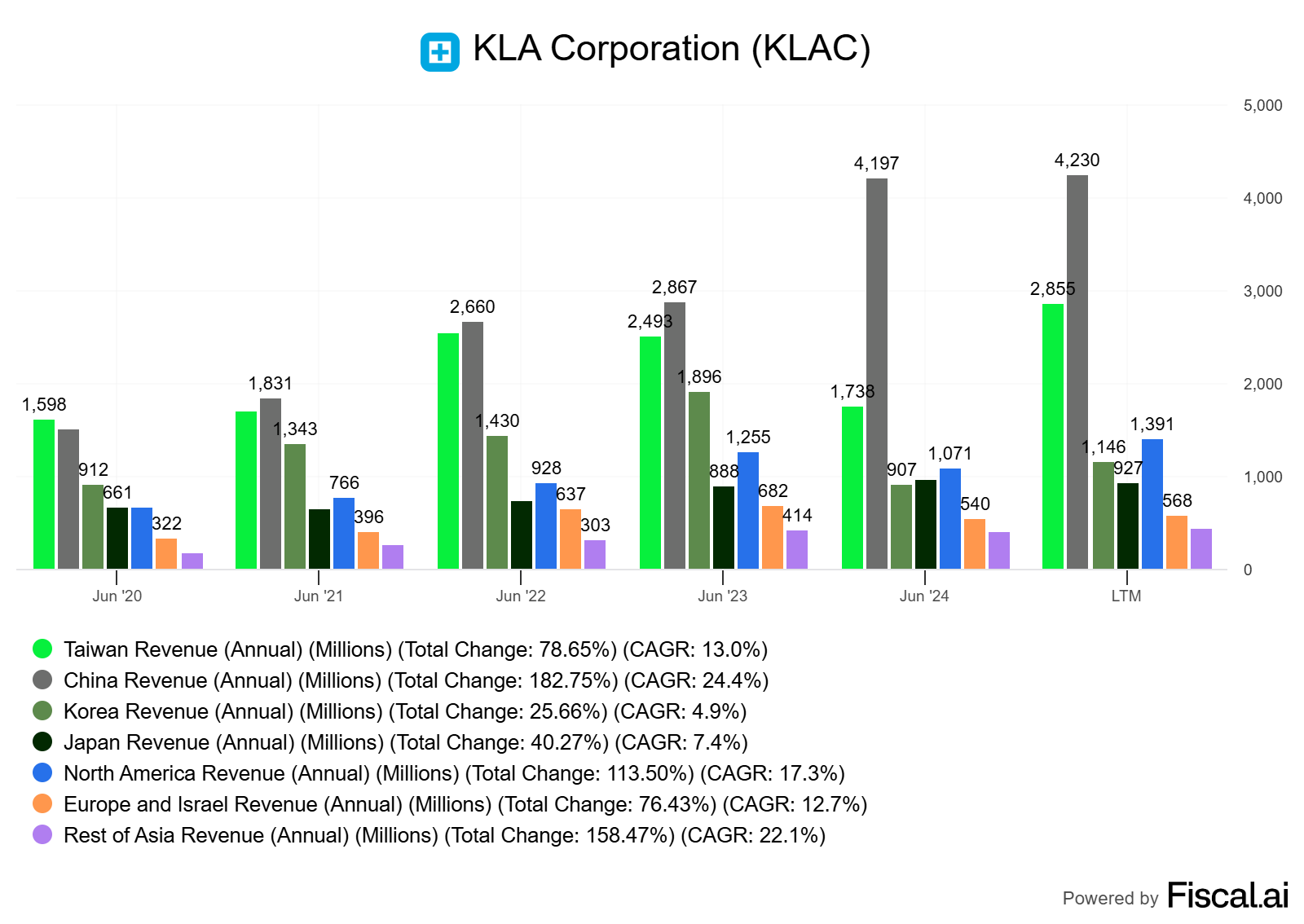

To be clear, this isn’t a call to exit immediately. KLA remains a leader, with over 56% share in process control (up 250bps since 5 years ago) and >85% in optical inspection. Additionally, KLAC 0.00%↑ stands to benefit from AI-driven chip complexity and advanced packaging trends, which boost demand for its process control machinery.

Source: KLA Corporation, Q3’FY25 earnings presentation

But with tariffs, export controls (notably in China, 26% of sales), and valuation risks, we’re stepping aside, for now.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

1. Our KLA Journey

We started building our position in April 2022 at $345, adding and trimming along the way. Our best buy was in October 2022 at $258, now up over 230%. Our September 2022 deep dives (both parts 1 & 2 still free) helped build our conviction at the time.

Back then, the stock traded at 13–16x earnings. Today, the multiple has doubled, driving significant part of the stock’s 168% return over the past 3 years (with EPS growth contributing 8.6% CAGR and multiple expansion 29% CAGR). While the company is unlikely to lose its dominant position, we believe it’s time to reallocate our 3.3% KLA position.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

2. What About the AI Tailwinds?

AI is transforming semiconductors, but not all companies benefit equally. KLA’s process control tools are critical for managing growing chip complexity and advanced packaging, especially in logic and DRAM tied to AI workloads. Still, we think growth expectations are already priced in.

Management expects the Wafer Fab Equipment (WFE) market, where KLA operates, to grow at a mid-single-digit percentage in 2025. After reaching ~$87B in 2023 and ~$100B in 2024, third-party forecasts (like Semiconductor Insights) estimate it will reach ~$138B by 2030, implying a CAGR of just 5.6%. That's solid, but not enough to support the current multiple, in our view.

3. Maintaining Strong AI Exposure While Adding New Stock

a. AI Still Drives Our Strategy

With this exit, our portfolio still maintains a 31% exposure to AI-focused stocks. Therefore, we believe our performance will continue to benefit from the ongoing technological shift. Key holdings