Skyline Champion Corporation – What went wrong?

Skyline Champion (“Skyline” or “SKY”) reported its Q4’23 results on the 30th May 2023, reporting revenues of $491.53M below consensus estimates of $538.33M (-8.69%), an EBIT of $68.77M below estimates of $73.5M (-6.44%) and EPS GAAP of $1 above estimates of $0.95 (5.71%).

Net sales declined by 23% year-on-year (“YoY”) driven by a drop in U.S homes sold of 25.5%, partially offset by a growth in Average Selling Price (“ASP”) of U.S homes of 5.6% while gross and adjusted EBITDA margins contracted by 120bps and 350bps, respectively.

Due to the unfavorable performance, share price plunged by 10.6%, to $57.66 (as of May 30th), and thus we decided to evaluate whether there is light at the end of the tunnel.

Did management underestimate the drop?

The drop in sales of 15.6% sequentially was well above the management estimates of a high single digits decline while an adjusted EBITDA margin of 15.5% was below the 16% achieved in FY22.

Back in Q3’23, management expected “As we move toward the end of our fiscal 2023, we reiterate our expectations of margins normalizing back to fiscal 2022 levels as we anticipate headwinds to our product mix…” Laurie Hough, CFO

Clearly management underestimated the fall in sales, as retail inventory destocking continued in Q4’22, while Community REITs paused orders to destock as well. It is worth noting that Retail and Communities were 48% and 33% of sales for FY23, respectively.

Moving into FY24, management anticipates a sequential decline in first quarter revenue in the mid-single-digit range, which per our calculations translates to a YoY drop of 36% or 27% if we exclude the FEMA revenues. EBITDA margin for FY24 is expected to be similar to FY22 at around 16%, primarily due to headwinds from the product mix. Consumer demand has shifted towards smaller homes, which are more affordable in the current high-interest-rate environment.

Considering that capacity utilization is down from 66% in prior quarter to 59% due to a new facility opened (Pembroke) and the expectation of 2 more plant openings for FY24 we do expect utilization to drop and operating deleverage to hit margins.

Anything below a 15% margin would translate to a need of revisiting our February 2023 SKY valuation and thesis in detail (Valuation can be found in the deep dive à Skyline Champion Corporation – A Compelling Investment Opportunity). In any case, we will be sharing an updated high level valuation at the end of this report.

Leading and growing market share. Is this still the case?

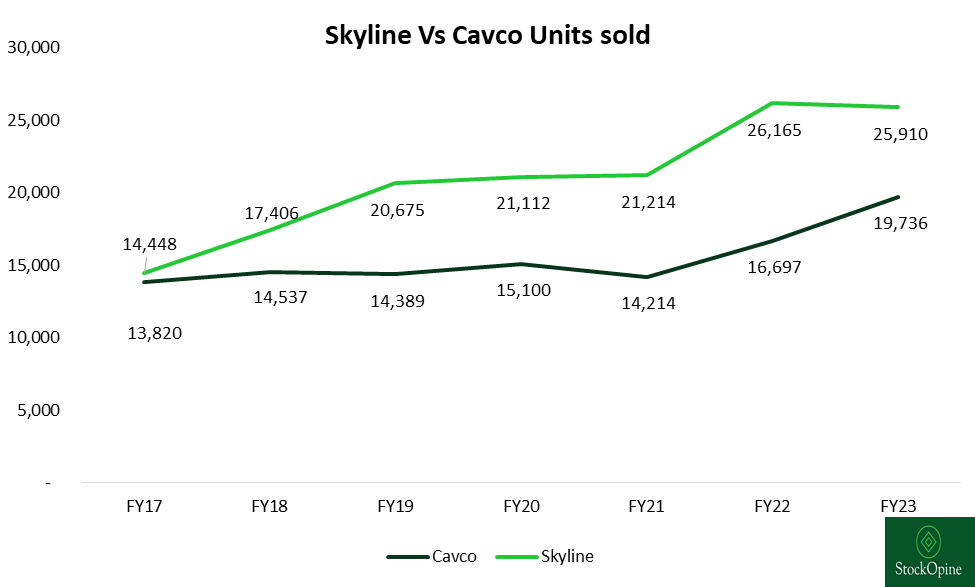

In our write-up we mentioned how SKY managed to improve its market share over the years. Currently, its US manufactured housing share stands at 20.4%, up from 19.3% in FY22. Nevertheless, per our calculations, Cavco’s (“CVCO”) market share seems that it has increased from 13% to 14.9% showing higher market share gains. This is not necessarily bad but something worth monitoring.

Source: 10K filings, StockOpine analysis, Note: Total units, not limited to HUD-code

In terms of total units sold (not limited to HUD-code) CVCO performed way better than SKY in FY23 depicting an increase of 18% Vs a 1% decline for SKY (mainly impacted by Canada volume decline of 20.6%). A similar trend is observed in HUD code homes, as SKY grew by 1.2% in US and CVCO by 10%. As 88% of Skyline's units sold were HUD-coded homes, comparing HUD-code unit sales provides a more representative comparison.