in capital markets, it is a fundamental truth that if a business generates exceptional profit margins, competitors will inevitably enter the market, undercut pricing, and attempt to steal market share. Left unchecked, those excess margins will eventually compress down to the company’s cost of capital.

Unless the business possesses an economic moat. A moat is a structural, durable competitive advantage that protects a company’s cash flows and pricing power over a long time horizon. In our bottom-up fundamental analysis, identifying the specific source of a company’s moat is arguably the most critical step before we even open a valuation model.

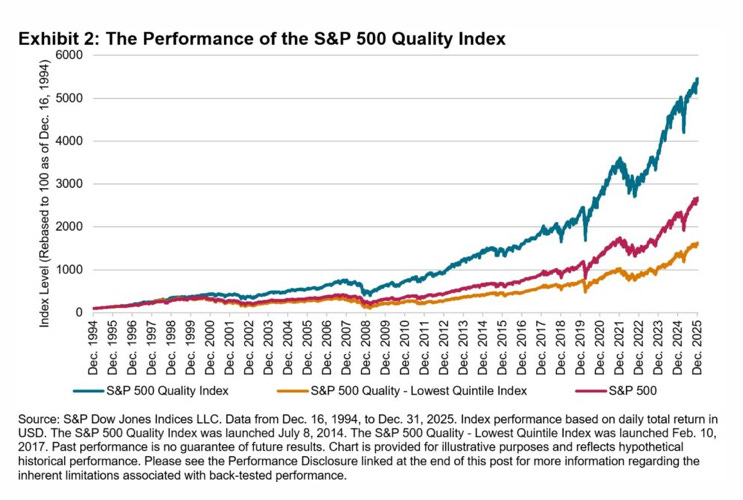

The Historical Data: Why Moats Matter

Focusing on structurally advantaged businesses isn’t just a theoretical exercise; it drives tangible long-term outperformance.

A strong indicator of a durable competitive advantage is a Return on Invested Capital (ROIC) consistently remaining above 15%. High ROIC combined with steady organic revenue growth demonstrates that a company is generating significant shareholder value with every dollar it reinvests into its operations.

The Four Pillars of a Competitive Advantage

We typically categorize structural advantages into four pillars. Here is how they look in practice:

1. High Switching Costs

The operational friction, financial cost, or risk of migrating away from a product is simply too high for the customer.

Autodesk ($ADSK): When an entire engineering or architectural firm standardizes its workflows, BIM models, and technical training on Revit and AutoCAD, ripping out that software to save a few dollars on a competitor’s license introduces unacceptable operational risk.

Cloud Infrastructure (AWS & Google Cloud): When an enterprise builds its backend architecture and databases natively on a cloud provider, moving to a competitor is a difficult task. It requires massive developer effort, code rewriting, and often incurs heavy data egress fees, making customer retention incredibly sticky.

2. Network Effects

The value of the product or service increases non-linearly with every new participant that joins the ecosystem.

Grab Holdings ($GRAB): We outlined this in our deep dive earlier this year. As more consumers use the super-app for ride-hailing and deliveries, merchant and driver density increases. Higher density leads to faster wait times and lower costs, which attracts even more consumers. Breaking this flywheel requires an uneconomical amount of customer acquisition spend.

Booking Holdings ($BKNG): A classic two-sided network. Travelers flock to Booking because it has the largest aggregated supply of hotels, homes and apartments globally. Conversely, accommodation providers are ‘forced’ to list on the platform because that’s where the global aggregate demand sits. Replicating this dynamic from scratch would require billions in marketing spend.

3. Intangible Assets

Patents, specialized intellectual property, or regulatory barriers that legally or practically prevent competitors from duplicating a product.

ASML Holding ($ASML): ASML holds an effective monopoly on the Extreme Ultraviolet (EUV) lithography systems required to manufacture the world’s most advanced semiconductors. Decades of hyper-specialized R&D mean a competitor cannot simply replicate their machines, regardless of capital.

Advanced Micro Devices ($AMD): The structural complexity of their chiplet designs and their deeply protected x86 architectural licenses create an impenetrable barrier to entry. A startup cannot legally or technically spin up tomorrow and begin manufacturing competing server processors.

4. Cost or Scale Advantage

The ability to sustainably produce or distribute goods at a lower cost than peers, often creating a flywheel that widens over time.

Pool Corp ($POOL): In a highly fragmented industry, their massive distribution network and localized scale allow them to source products at terms independent distributors cannot match. By serving as the single, reliable point of supply for local pool professionals, they possess an operational scale advantage that protects their market share.

Amazon ($AMZN): The scale of Amazon’s fulfillment and logistics infrastructure allows them to deliver products faster and cheaper per unit than almost any retailer on earth. Replicating this physical footprint today would require hundreds of billions of dollars, giving Amazon a nearly insurmountable structural edge.

Spotting the Cracks: When Moats Erode

A moat is rarely breached overnight. It is a slow bleed that shows up in the financials long before it completely destroys the underlying business.

When reviewing earnings reports line-by-line, we look for three indicators that a structural advantage is beginning to erode:

Persistent Margin Compression: If margins begin to contract in a stable macroeconomic environment, it is often a sign the company has lost its pricing power.

PayPal ($PYPL): In recent years, PayPal’s unbranded processing business, Braintree, expanded rapidly, but at the cost of compressed margins. Braintree’s volume grew much faster than PayPal’s premium branded checkout segment. Because unbranded processing is increasingly viewed as a commodity-like service, it lacks the pricing power of branded checkout, which led to overall transaction margin pressure. This margin compression signaled to the market that PayPal’s competitive advantage was under intense pressure from peers. At PayPal, the new CEO Enrique Lores, who took over in March 2026, is currently driving a massive turnaround effort. He is focusing on simplification, cost savings through AI adoption, and reinvesting in higher-margin areas but that doesn’t mean that he can turn the ship around.

Management Tone Shifts: Listen closely to earnings calls. When executives suddenly shift their strategic narrative or acknowledge aggressive competitor pricing, it is an admission that their product is facing commoditization.

Adyen ($ADYEN.NV): In the first half of 2023, Adyen reported slowing growth in North America alongside EBITDA margin compression, causing its stock to lose over 40% of its value in a single day. During this period, competitors like Braintree were aggressively trying to capture market share at any cost. Adyen’s management realized that they had underinvested in their sales and account management teams, forcing a strategic shift to aggressively hire new staff to properly sell their platform and defend their market position. The margin compression proved to be temporary; as their hiring initiative concluded, operating leverage returned, and EBITDA margins expanded back to 50% for the full year 2024.

Deteriorating Fundamentals and Market Share: The most glaring red flag. If a company’s core product is disrupted by a paradigm shift, the financial collapse is usually swift and permanent.

BlackBerry ($BB): BlackBerry is the ultimate case study of a technological moat evaporating. In 2008, the company possessed a massive structural advantage driven by its secure enterprise network and hardware, reaching a peak market capitalization of approximately $75 billion. At its height, BlackBerry controlled over 50% of the US smartphone market and its stock hit an all-time closing high of $139 in April 2008. However, as the computing paradigm shifted and competition from Apple’s iPhone intensified, their product became obsolete. The moat was destroyed. By the end of 2008, their market cap had already plunged to $23 billion. Fast forward to July 2026, and the stock is trading around $11, leaving the company with a market cap of roughly $6.4 billion. It is a brutal reminder that a temporary technological lead is not a permanent moat.

The Bottom Line

A great product or a temporary technological lead is not a moat. If you are investing for the long term, you must ask: What structural barrier prevents a well funded competitor from eroding this company’s margins in five years?

If you cannot clearly identify the moat, the future cash flows are not secure. However, it is vital to remember that even the widest moat does not guarantee a successful investment if the price is wrong. Valuation drives returns. Buying an extraordinary business with a durable moat only works if you have the patience to demand a margin of safety.