The Future of Payments: Understanding the Payment Stack

Welcome to the guest section of StockOpine! In this section, we feature content from respected creators who are friends of StockOpine and have been invited to share their knowledge with you. Additionally, we will also collaborate with industry experts, some of whom we have personal connections with, to provide you with insightful perspectives.

Today’s article comes from

, co-host of the The Investing for Beginners Podcast and co-author of einvestingforbeginners.com.We crossed paths with Dave over a year ago and since then, he has become our favorite FinTwit creator (@IFB_podcast). Dave shares educational content tailored for beginner investors, using simplified language that makes it easy to grasp essential concepts. Occasionally, he also shares company analyses that are accessible to newcomers in the investment world. His work is topnotch and we encourage you to explore it.

Today’s article (estimated read time ~50 minutes) delves into the payment stack, an area where investors often find themselves confused due to the various definitions circulating within the payment space. This article aims to provide clarity by outlining the 5 essential stages of the payment flow, assisting you in identifying the key players in each stage and concludes with valuable insights from Dave on the future of payments.

The Future of Payments: Understanding the Payment Stack

Analysts expect global payment revenues to grow to $3.3 trillion by 2026, according to McKinsey, after returning to their historical 6 to 7 percent growth rate following the pandemic, which saw drops in global payment revenues of 5 percent to $1.9 trillion in 2020.

Source McKinsey 2022 Global Payments Report

The future of payments continues to evolve, and many believe that cash is dead. The trend towards electronic payments only accelerated during the pandemic, a change already underway.

Many investors have taken advantage of this change by jumping on board the payments train by investing in such companies as PayPal (PYPL), Square (SQ), Visa (V), and Mastercard (MA), among countless others.

The payments space remains crowded, competitive, and the pace of change continues to accelerate.

In today's post, I wanted to unpack some players to understand who is who and why they continue to grow in relevance.

Today we will discuss the different terminology and how they interact along the payment processing chain so you can better understand the economics of that chain, along with any investment opportunities.

It can get a little confusing with terminology such as payment processors, merchant banks, issuing banks, interchange fees, and payfacs, to name a few.

But, after reading today's post, you will better understand.

1. How Payments Work

2. Understanding the Fees Earned in Payments

3. The Payment Stack

4. Players in the Stack

5. Future of payments

1. How Payments Work

Credit Suisse estimated in 2020 that the total opportunity, or TAM (total addressable market), for global payments totals $240 trillion across card payments, with the greatest expansion in Asia/Pacific, Latin America, and Eastern Europe.

Source: Andreessen Horowitz Fintech Sales Vertical SaaS

That is a tremendous opportunity for a variety of players across the board.

So what is involved in payment processing?

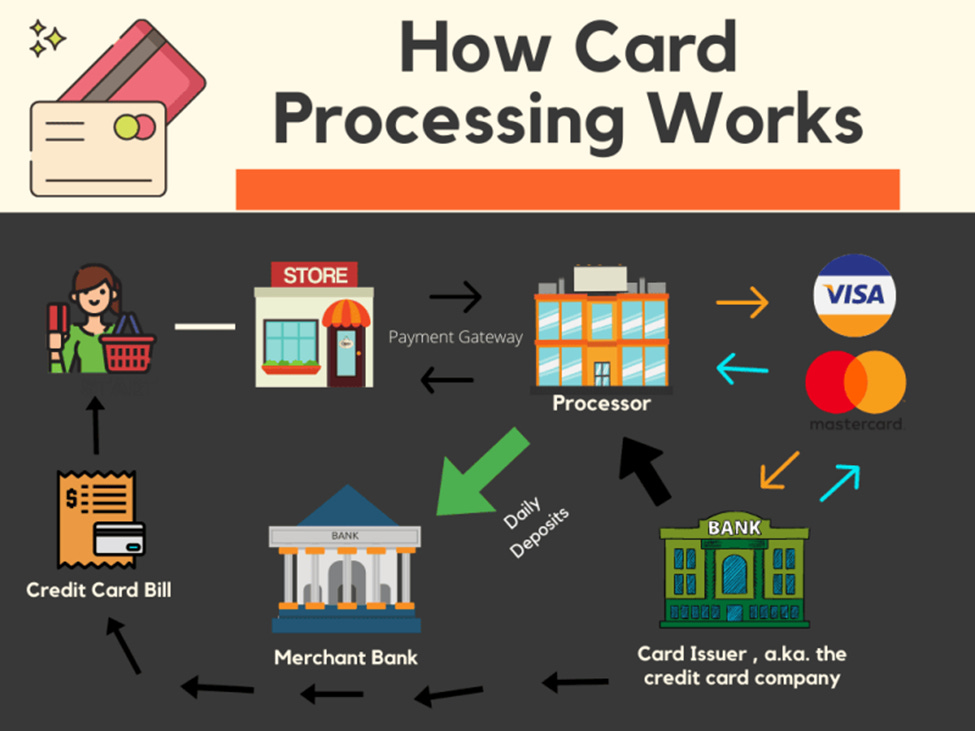

Payment processing is the operation that occurs when we use a payment method such as a debit or credit to buy something online or in-person.

What does that look like when we swipe our card?

It revolves around a cycle from the buyer (us) to our bank and back to the merchant, with a few stops to ensure accuracy and fraud prevention.

The payment cycle begins with our decision to buy that present for our significant other for $100 from the jewelry store. The authorization process begins when we press the confirmation or buy button on the POS (point-of-sale) terminal or online.

Next, the merchant (jewelry store) forwards a request to the acquirer, which the acquirer passes along to the card scheme (Visa/Mastercard) associated with our debit/credit card.

The card scheme or Visa/Mastercard forwards that request to our card issuing bank (JP Morgan) and JP Morgan checks to ensure we have the $100 in our account to pay for the gift.

If we clear that hurdle, the confirmation is sent back through the loop to the jewelry store, which submitted the request originally.

Along that path, there are several players:

Merchant (jewelry store)

Acquirer (Fiserv)

Card Scheme (Visa)

Issuing bank (JP Morgan)

All of those above players split up the associated fees by enabling the above transaction, and each player gets a different slice of the pie.

For example, the merchant that charges us the $100 for the item receives back $98, and the acquirer, card scheme, and issuing bank divvy up the balance of the $2.

Next, let's cover the actual process more so we understand the process.

Card processing, either online or in the store, happens in three distinct processes:

Authorization

Settlement

Funding

Let's first look at how cards are authorized:

The cardholder presents their card in person or virtually to a merchant in exchange for products or services. The request might come in the form of a card terminal in-store, POS (point-of-sale) system, or through the e-commerce gateway on the merchant's website. Payment processing can also occur through a merchant's mobile or in-app process.

Once the payment is received, the merchant sends an authorization request to the payment processor.

For example, the payment processor sends the request through the appropriate network, Visa or Mastercard. The payment eventually reaches the issuing bank.

The issuing bank makes the authorizations, including CVV numbers, validation, and expiration dates.

Then the issuing bank either approves or declines the transaction.

The issuing bank then sends the approval or denial back the way it came to the card association, merchant bank, and back to the merchant.

Pretty simple, huh?

An easy way to think about the flow is to visualize a highway. First, we get on the highway headed for our destination, in this case, the issuing bank. We get on our highway through a ramp (merchant processor); once on the highway, we choose which direction to go (credit card association, Visa/Mastercard); once we decide on the direction, we arrive at our destination, the issuing bank.

Now, let's look at a simplified settlement process and funding of card payments.

Merchants send authorized batches of transactions to their payment processor, often at the end of the business day or predetermined time.

The payment processor details the transactions to the card associations, who communicate the appropriate information to the issuing banks on their networks.

The issuing bank debits the cardholder's account for the transaction.

The issuing bank then transmits the funds to the merchant bank minus interchange fees.

The merchant bank deposits the funds in the merchant's account.

Pretty simple, huh? Considering this all happened overnight when it used to take days. It allows the merchant to get their money quicker, helping their cash flows.

2. Understanding The Fees in Payments

The payment fees or that $2 is the slice of the pie that each component of the payment flow receives for their actions in the flow.

In many cases, it breaks down to pennies or fractions of pennies, but when you consider that Visa transacted over 258 billion transactions in 2022, and PayPal processed over 22.3 billion in 2022, those pennies will add up to substantial sums.

Graph courtesy of All Things Fintech

The total processing fees breakdown into three main groups:

Interchange fee: the issuing bank takes the largest slice of the pie, called the interchange fee. These interchange fees will vary depending on various factors, such as the type of card used (credit/debit), industry, and sale amount.

Visa and Mastercard set the interchange fees, which they update bi-annually. At last check, there were well over 300 interchange fees and many breakdowns like this simple example; 2% of the sale volume + $0.10 per transaction.

For our example above, that would work out as $100 x 2% + $0.10 equaling $2.10.

Assessment fees: the fees that the card schemes such as Visa and Mastercard charge for their services. Visa and Mastercard include the assessment fee in the interchange fee, and many confuse the interchange and assessment fee as the same.

The typical rate for the assessment fee is 0.10% + $0.02 per transaction, so returning to our jewelry store purchase would work out as $100 x 0.10% + $0.02 equaling $0.12.

They bundle the assessment fee with the interchange, meaning no additional fees to the merchant for processing a Visa/Mastercard card. The issuing bank (JP Morgan) pays Visa their assessment fee out of the interchange fee.

Markup fee: this is the fee that the merchant acquirer or the payment processor charges the merchant for enabling the payment through their POS. The amount of the markup will depend on the type of industry, monthly processing volume, amount of sale, card type, and type of transaction (present or not present).

The typical structure for markup fees is a percentage of the sale plus a per-transaction fee. For example, 0.25% + $0.10; back to our example, $100 x 0.25% + $0.10 equals $0.35.

To further delineate the fees, both the interchange rate and assessment fee are non-negotiable, meaning that if you choose to process debit cards or credit cards with a Visa or Mastercard logo on the card, those fees are mandatory, and there are no negotiating them, with either your bank or Visa/Mastercard.

They are the cost of doing business if you are a merchant, and to allow payments; you need to accept both Visa and Mastercard branded cards because those are the cards your customers carry in their wallets, real or virtual.

The markup fees are the only negotiable fees, and you can work out different rates with the merchant acquirers or companies that help you process your electronic payments. Many acquirers offer different rates to get the merchant's business, from lower rates if you process higher volumes to different rates for online payments versus in-person checkouts.

Let's look at these economics in a chart to explain how this works for the different players along the chain.

At the end of the payment process, the jewelry store receives $97.55 after running the payment through the payment process, with the various players receiving their slice of the pie through the cycle.

Remember that the time from submitting payment to approval takes seconds, which is mind-boggling.

Remember that many fees, over 300, depend on what card you use and how that payment processes. For example, there are different rates for debit cards versus credit cards, and whether they process in-person or card-not-present.

These rates also depend on which bank issues the cards, the requirements behind the Durbin Amendment regulating debit card usage, and the fees charged.

Ultimately, you don't have to memorize every type of transaction and fee; instead, it is important to understand the process and flow, the economics behind the transactions, and how those economics drive the different players in the flow.

3. The Payment stack

There are five major players in the payment processing flow, some with different names, doing the basic job described in our jewelry store example.

Some players occupy more than one role in the payment processing flow, which can get convoluted, but I will try to clarify everything in a tidy box.

According to Worldpay, cards and digital wallets occupy more than 70% of e-commerce and 79% of in-store transactions, and across the payment value chain, there are five main players:

Customer

Merchant

Issuer

Acquirer

Card network

Customer

Also known as the cardholder if they pay with a credit or debit card. Customers are the end-user who begin the payment processing chain by initiating the payment with the merchant. Customers gain from the convenience of using electronic payments for goods and services online or in-person, sometimes as rewards or cash-back on their purchases.

Think of the customer as the starting point of the payment cycle, and visualize yourself paying for your items at Target, online, or in person. We all know you can't get out of Target without spending at least $100.

Merchant

To accept any electronic payment, online or in-person, the business needs to open a merchant account. The merchant establishes an account with the acquirer to settle the funds or push the transaction through the cycle and back to Target.

Target gains from participating in that network by attracting and retaining customers with a fast and efficient checkout. Merchants are the customers at this point of the payment cycle; for example, Target uses acquirers to enable payments online or in-person to receive payments for their goods and services from us, the customer.

Examples of merchants abound, but here is a sample:

Target

Home Depot

McDonald's

Lululemon

Reebok

Kroger

Issuing Bank / Issuer

The issuing bank, or issuer, is the financial institution, typically a bank, that issues cards to the customers. The issuing bank provides either debit or credit cards and makes payments on the customer's behalf. The issuers also manage the payment authentication process, ensuring adequate funds to complete the purchase.

The issuers receive the transaction information from the acquirer and respond by approving or declining the transaction.

For approvals, the process involves ensuring the transaction is valid, guaranteeing the card belongs to a cardholder, and that the account has enough funds or credit to complete the requested transaction.

And finally, the issuing bank or issuer sends a response code back to the acquirer through the payment network.

The issuer receives the largest part of the payment pie, receiving the lion's share of the interchange fee, which Visa and Mastercard set.

The issuer receives the largest portion because they take on the largest share of risk in the transaction flow; by guaranteeing the payment, they assume any default risk.

The issuing bank often distributes their cards to cardholders with a particular brand, Visa or Mastercard, which allows them to process over those networks. Other branded cards, such as American Express and Discover, have networks.

For example, Bank of America could issue their debit and credit cards with a Visa logo, while Capital One might issue them with a Mastercard logo.

Acquirer

The acquirer, or acquiring bank, is the bank or financial institution that enables payments for the merchants.

They provide the merchant with the software and hardware to enable payments for the customers via a POS in the store or online through the merchant's website.

The acquirer, also known as the merchant acquirer, is customer-facing, and they have a personal connection with the merchant to provide payment services. In many cases, they physically go to the merchant to sell them on processing their payments with their services.

The merchant acquirer uses their software/hardware to capture the transaction information and route it through the appropriate card network (Visa/Mastercard) to the cardholder's issuing bank for transaction approval.

After approval of the transaction by the issuing bank, the merchant acquirer settles the payment with the merchant, typically within two business days.

The amount settled with the merchant (Target) exceeds the interchange, card scheme, and acquiring fees. Any additional fees associated with refunds, reversals, and disputes will settle simultaneously.

It can get confusing here; the merchant acquirer can also be the issuing bank or issuer acquirer. That means that the same financial institution that issues your debit card also acts as the processor for Target.

In other words, they occupy two slots in the payment processing cycle and also take a larger portion of the processing fees they charge Target. So when looking at the processing cycle, JP Morgan occupies two slots, merchant acquirer and issuing bank.

Card Network

The card network is the payment rail that allows all payment activity to flow across those rails between the customer, merchant, and issuer.

The payment rail is also the card brand or scheme for every card swipe, chip-and-pin, contactless, online, or card-not-present. These card networks provide the means for all card transactions to occur, and in exchange for that access, all acquirers and issuers must pay a toll or fee.

The card networks pass along information and help settle funds between the acquirer and the issuer. They also set the standards that all acquirers and issuers communicate (or protocols) and define all rules by which acquirers and issuers handle disputes.

The two most common card networks or schemes are Visa and Mastercard, which offer an open-loop system. The open-loop system connects to the customer's credit or bank account and allows multiple payment options.

The other two common card networks are American Express and Discover, both closed-loop systems. The closed-loop system links the card to a pre-paid account, typically a credit account.

American Express and Discover act as acquirers and issuing banks and set merchant interchange fees.

Others

The final two terms you might hear thrown about in conversations about payment processing are:

Payfacs or PSP: These providers offer merchants connections with multiple acquirers and payment methods like debit cards, credit cards, bank transfers, and others. The payfacs also integrate their technology with the merchant's POS to seamlessly collect and manage their payments.

Payfac's biggest benefit is the ease of use for the merchant; they offer simple turnkey solutions for payments for merchants without the headaches of setting up all the technology and systems.

The two biggest providers of these services are Stripe and Adyen, with Square offering the same services to small and micro-businesses.

Payment gateways: these companies offer a technical layer that collects the clients' payment credentials on the merchant side and securely sends them to an acquirer. The leader in this space is Braintree, owned by PayPal.

4. Players in the stack

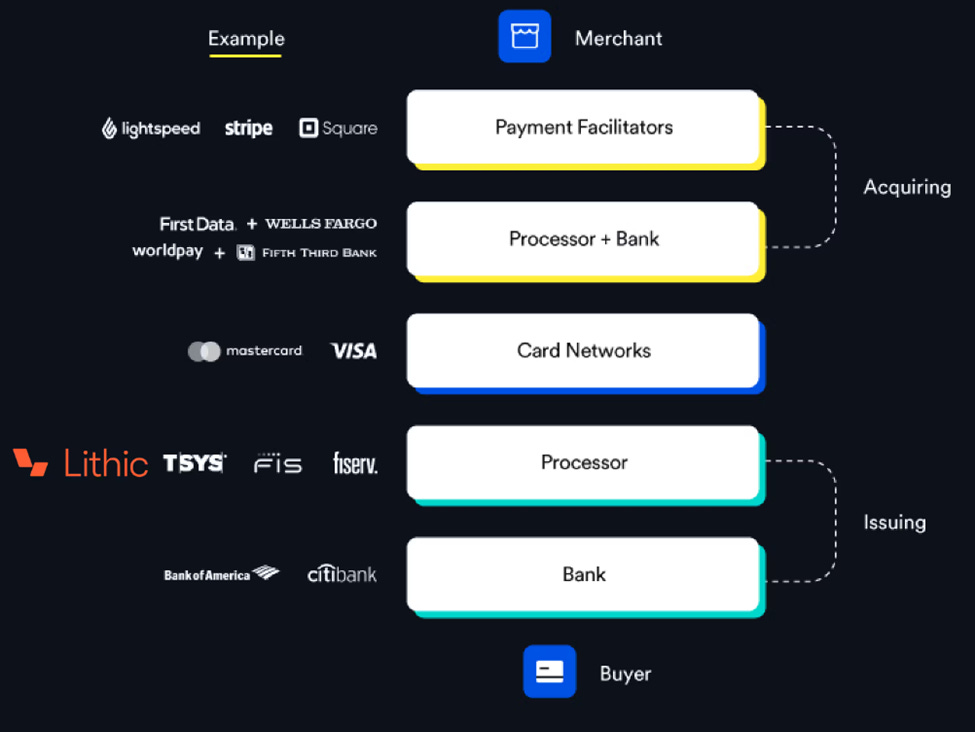

Now that we understand the ecosystem and the flow of payments let's dive into the particular players in the stack.

Understand there are LOADS of different companies operating in the fintech space. And many of them cross over into different parts of the stack.

Source: Finix, Contrary Research

For example, JP Morgan operates as an issuing bank and merchant acquirer (Chase Paymentech).

Payment Facilitators (Payfacs)

These businesses are probably the most exciting part of the payment stack and are where a lot of energy goes to find the best investments.

Companies such as Stripe, Block (Square), PayPal, Adyen, Checkout, Payoneer, and Lightspeed are some of the many.

Adyen

Adyen is a global payment processor started in 2004 and has headquarters in Amsterdam, Netherlands, and offices in over 70 countries.

Adyen specializes in processing payments for e-commerce merchants, and it offers a variety of payment methods, including credit cards, debit cards, and alternative payment methods.

Adyen has been growing rapidly in recent years. In the five years from 2018 to 2022, the company's processed volume grew from €159 billion to €767.5 billion. Its net revenue grew from €348.9 million to €1,330.2 million, and its EBITDA grew from €181.9 million to €728.3 million.

Several factors have driven Adyen's growth, including its global reach, support for various payment methods, and fraud prevention tools. The company has also benefited from the growth of e-commerce in recent years.

Adyen is a well-established and profitable company with a strong track record of growth. The company is well-positioned to continue its growth in the years to come.

Stripe

Stripe is a global payment processor that began in 2010. The company has headquarters in San Francisco, California, and offices in over 40 countries. The company remains private, one of the few we will cover today.

Stripe specializes in processing payments for online businesses, and it offers a variety of payment methods, including credit cards, debit cards, and alternative payment methods.

Stripe has been growing rapidly in recent years. The five years from 2018 to 2022, the company's processed volume grew from $100 billion to $817 billion. Its net revenue grew from $2.5 billion to $5.5 billion, and its EBITDA grew from $1.2 billion to $2.9 billion.

Driven by several factors, Stripe's growth has relied on its easy-to-use platform, competitive pricing, and fraud prevention tools. The company has also benefited from the growth of e-commerce in recent years.

Stripe is a well-established and profitable company with a strong track record of growth. The company is well-positioned to continue its growth in the years to come.

Here are some additional details about Stripe's business and financial performance:

Stripe's customers include many businesses, from small startups to large enterprises.

Stripe is available in over 40 countries and supports over 135 currencies.

Stripe has raised over $2.2 billion in funding from investors such as Peter Thiel, Sequoia Capital, and Andreessen Horowitz.

Stripe received over $50 billion valuation based on its latest funding round.

Stripe is a leading player in the global payment processing industry. And many investors anticipate the day they go public so they can own Stripe.

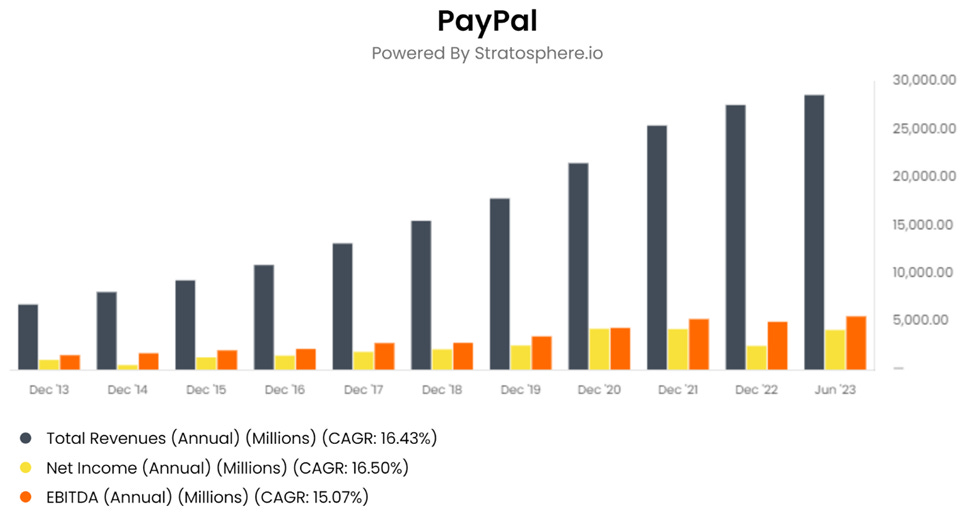

PayPal

PayPal is an online payment system founded in 1998—the company headquarters in San Jose, California, with offices in over 200 countries. PayPal allows users to send and receive money online, and it offers a variety of payment solutions for businesses of all sizes.

PayPal is one of the most popular online payment systems in the world. The company has over 431 million active users and processes over $1,425 billion in payments yearly. Many businesses, from small startups to large enterprises, use PayPal.

PayPal offers a variety of payment solutions for businesses, including:

Online payments: PayPal allows businesses to accept payments from customers online through the PayPal website or the PayPal app.

In-store payments: PayPal offers a variety of in-store payment solutions for businesses, including the PayPal Here card reader and the PayPal Zettle card reader.

Mobile payments: PayPal offers a payment solution called Pay in 4, allowing businesses to accept customer payments in four installments.

PayPal also offers a variety of features for businesses, including:

Fraud protection: PayPal offers a variety of fraud protection tools to help businesses protect themselves from fraud.

Reporting and analytics: PayPal offers businesses a variety of reporting and analytics tools to help them track their sales and payments.

Customer support: PayPal offers businesses 24/7 customer support to help them with problems.

PayPal contains more recognizable fintech brands like the PayPal button, Braintree, and Venmo.

Here are some additional details about PayPal's business and financial performance:

PayPal's revenue in 2022 was $27.5 billion.

PayPal's net income in 2022 was $2.5 billion.

PayPal's market capitalization is over $68.9 billion.

PayPal remains one of the leaders in the industry and probably one of the more frustrating ones as well. With the potential turnover in the management, many investors eagerly anticipate new leadership to take PayPal to new heights.

If you want to dig deeper into PayPal, I strongly encourage you to check out Stock Opine's fantastic article.

Block (Square)

Block, Inc. (formerly Square, Inc.) is a financial technology company that provides payment processing, point-of-sale (POS) software, and other financial services to businesses of all sizes. The company was founded in 2009 by Jack Dorsey and Jim McKelvey.

Block's flagship product is Square, a POS system that allows businesses to accept credit and debit cards. Square also offers a variety of other products and services, including:

Cash App: A mobile payments app that allows users to send, receive, and invest money.

Afterpay: A buy now, pay later service that allows customers to make purchases and pay for them over time.

Tidal: A subscription-based music, podcast, and video streaming service.

TIDAL HiFi: A high-fidelity music streaming service.

Spiral: A team of engineers building open-source, decentralized financial tools.

TBD: A team of engineers building an open developer platform to make accessing Bitcoin and other blockchain technologies easier.

Cash App users (monthly transacting actives) hit 54 million in Q2 2023 while Square’s gross payment volume (GPV) in 2022 exceeded $203 billion.

Here are some additional details about Block's business and financial performance:

Block's revenue in 2022 was $17,531 million.

Block's net income in 2022 was $(540.1) million.

Block's market capitalization is over $38.26 billion.

Block has one of the best platforms with both Square and Cash App, but Bitcoin adds complexity to their focus. Additionally, they remain the only unprofitable payfac.

Processors

Processors remain the dominant players in the fintech space. These companies offer the largest payment processing across the space.

Businesses like Chase Paymentech, the leader in the space, Fiserv, Global Payments, and FIS are the leaders. But the space has a ton of disruption coming from the likes of PayPal (Braintree), Adyen, and Block, among many others.

Other banks such as Wells Fargo, Citibank, and Fifth Third Bank also offer these services.

Source: Credit Suisse

Fiserv

Fiserv is a financial technology company that provides payment processing, digital banking, and other financial services to banks, credit unions, retailers, and other organizations. The company began in 1984 and headquarters in Brookfield, Wisconsin.

Fiserv's business model provides integrated financial technology solutions that help its customers improve their efficiency, profitability, and customer service. The company's products and services include:

Payment processing: Fiserv provides payment processing solutions for various channels, including point-of-sale (POS), e-commerce, and mobile payments.

Digital banking: Fiserv provides digital banking solutions that help banks and credit unions offer customers various online and mobile banking services.

Risk management: Fiserv provides solutions that help banks and credit unions protect themselves from fraud and other financial risks.

Compliance: Fiserv provides solutions that help banks and credit unions comply with regulations.

Analytics: Fiserv provides analytics solutions that help banks, and credit unions gain insights into their businesses and make better decisions.

Fiserv's business model is successful because it offers a wide range of integrated financial technology solutions that meet the needs of various customers.

Fiserv operates as a jack of all trades in the fintech world, and they acquired First Data in 2019, which provided them with all kinds of options.

Clover's processing platform enables them to compete with Block and PayPal in the SMB space. Their e-commerce platform, Carat, allows them to compete with Adyen. And the core business is core banking, which provides the plumbing for banks, and is the largest provider of Zelle for banks.

Fiserv's financial performance in 2022:

$17.3 billion in revenues with growth of 9.3% YoY

$2.53 billion in net income

$6.89 billion in EBITDA

Fidelity Information Services ($FIS)

Fidelity Information Services is one of the leaders in processing. The company operates the Worldpay platform, which it acquired 2019 for $43 billion.

The Worldpay acquisition allows FIS to offer the following:

Payment processing

Digital banking

Risk management

Compliance

Analytics

Frankly, the WorldPay acquisition hasn't played out well for FIS, and the company is now looking to spin off the company.

FIS generated $14.5 billion in revenue TTM, up 1.3%

Net income equaled -25.3 billion in 2022 because of the write-down of goodwill from the Worldpay acquisition

EBITDA equaled $4.1 billion

Card Networks

The card networks, Visa and Mastercard, act as toll roads or payment rails for the payment flow. They enable the pass-through from processors to banks and back to the merchant. They provide security, verification, and protocols.

Visa and Mastercard dominate the landscape as a duopoly in the fintech world. Visa processed 14.5 trillion transactions, and Mastercard handled over 6.9 trillion transactions.

Each company has one of the world's most popular logos and brands.

Visa and Mastercard also set the fee processors to charge merchants, but most revenue goes to the issuer bank. Many confuse Visa and Mastercard as cardholders; they are not. They only provide logos, not credit or debit cards. Instead, those come directly from your bank.

Both companies remain incredibly profitable, with growing revenues. For example:

Mastercard:

$23.5 billion in revenue TTM

Gross margins equal 100%

Operating margins equal 57.1%

FCF margins equal 45.9%

Visa:

Visa generated $31.8 billion in revenue TTM

Gross margins of 97.7%

Operating margins of 67.1%

FCF margins of 52.8%

Bottom line, Visa and Mastercard remain integral to the movement of money worldwide. They also offer some of the most profitable businesses out there.

The duopoly also has withstood, so far, many assaults on their moat. The biggest risks they face currently remain government regulation and crypto.

Bank Issuers

A bank issuer is a financial institution providing consumers and businesses with payment cards, such as credit and debit cards. Bank issuers also process payments made with these cards.

Chase Paymentech is a bank issuer that JPMorgan Chase owns. Chase Paymentech provides payment processing services to merchants of all sizes, including online, brick-and-mortar, and mobile merchants.

Chase Paymentech also provides various other services to merchants, such as fraud prevention and risk management services.

According to JP Morgan, Chase Paymentech processed over $1.4 trillion in payments in 2022, a 20% increase from 2021. Because they operate within one of the largest banks in the US, they have a distinct advantage in adding merchants to their ecosystem, especially if the customer already banks with JP Morgan.

Remember, banks are the ones issuing customers' debit and credit cards. But they can also act as a processor, similar to Adyen and Fiserv.

For example, most large banks, Citibank, Wells Fargo, and US Bank offer payment processing at some level, but Chase Paymentech remains the leader.

Others

The fintech space is huge, and there are so many players in the space.

Fintech has grown exponentially over the past three years, and various players have sprouted up in various niches. The fintech providers hope to fill in the gaps in how we use our money.

For example, we have companies helping us manage our bills, transfer money globally, take out mortgages, and manage crypto.

Speaking of crypto, in 2022, crypto-only accounted for 0.2% of global e-commerce transactions, so there is a long way to go there.

If I were to cover all of them, we would be looking at a 10,000-word post, so in the interest of brevity, below is a list of some of the others in the space:

Affirm – BNPL

Klarna – BNPL

Apple Pay

Google Pay

Paytm – India

WeChat Pay – China

Mercado Libre – Brazil

Dlo – Uruguay

Revolut – England

Wise - England

5. Future of payments

We have discovered that the fintech space is huge, with a long runway ahead. The industry continues to grow and expand, with the best still ahead.

Source: PwC

Cash is dead, well, not really, but many in the fintech space believe the way we pay is changing and will only accelerate.

The VC spending on fintech levels continues to accelerate and indicate growth in the space. This from CB Insights:

"In 2022, global fintech funding reached $75.2 billion, a 46% drop from 2021 but a 52% increase from 2020. The funding slowdown was especially severe in the year's second half, with Q4'22 funding at $10.7 billion, the lowest quarterly level since 2018."

The recent explosion of AI represents the next frontier in tech, and fintech is no exception. AI will allow current companies to build up existing tech, opening up big potential and applications.

And growth in fintechs continues to escalate.

As of 2023, there are over 26,300 fintech startups worldwide. This is up from around 12,000 in 2019. The number of fintech startups has more than doubled in the last two years.

The Americas have the most fintech startups globally, with 11,651 as of May 2023. The EMEA region (Europe, the Middle East, and Africa) has 9,681 fintech startups, and the Asia Pacific region has 5,061.

Fintech continues to seep into every aspect of our financial lives, for example:

Payments – PayPal, Stripe, Adyen

Personal finance – Mint, Rocket Money, Personal Capital

Investing – Sofi, Wealthfront, Robinhood

Insurance – Lemonade, Oscar, Root

Banking – Chime, Varo, N26

Lending – Upstart, Prosper, LendingClub

Cybersecurity – Cloudflare, Crowdstrike, Avast

AI – Nuance, Palantir, Kensho

Blockchain – Bitcoin, Ethereum, Coinbase

Open banking and embedded payments are two of the most disruptive trends in fintech today. They are having a major impact on how financial services are delivered and are poised to revolutionize the industry in the coming years.

Open banking is a system that allows third-party developers to access customer banking data through Application Programming Interfaces (APIs). This allows developers to create new financial products and services that are more personalized and convenient for consumers.

For example, a developer could create a budgeting app that automatically imports data from a user's bank account or a lending app that can instantly assess a user's creditworthiness.

Embedded payments technology allows merchants to integrate payment processing into their websites or apps. Eliminating the need for customers to leave the merchant's website or app to complete payment.

Embedded payments are becoming increasingly popular, offering consumers a more seamless and convenient checkout experience.

Both open banking and embedded payments are having a major impact on the current state of fintech. They are enabling fintech companies to create new, innovative financial products and services that are more personalized and convenient for consumers. This leads to increased competition in the financial services industry, ultimately benefiting consumers.

Source: FIS Global Payments Report

In the future, open banking and embedded payments will help to revolutionize the financial services industry.

They can make financial services more accessible, affordable, and transparent for consumers. They can also help to improve financial inclusion by making it easier for people to get the financial services they need.

Here are some specific examples of how open banking and embedded payments are being used to innovate in the financial services industry:

Personal finance: Fintech companies are using open banking to create new personal finance apps that help consumers track their spending, budget their money, and save for goals.

Investing: Fintech companies are using open banking to create new investment apps that make it easier for consumers to invest their money. These apps can automatically import data from a user's bank account, so they can see how much money they have to invest and what investments are available to them.

Insurance: Fintech companies are using open banking to create new insurance products that are more personalized and affordable for consumers. These products can use data from a user's bank account to assess their risk profile and offer a more competitive rate.

Lending: Fintech companies are using open banking to create new lending products that are more accessible and affordable for consumers. These products can use data from a user's bank account to assess their creditworthiness and offer them a loan with a lower interest rate.

Open banking and embedded payments are just two of the many ways that fintech is changing the financial services industry.

The financials of open banking and embedded payments are still in their early stages but growing rapidly.

According to a report by Juniper Research, the global open banking market expects to reach $330 billion by 2027, up from $57 billion in 2023. The report also predicts that the global embedded payments market will reach $183 billion by 2027, up from $65 billion in 2022.

The growth of open banking and embedded payments stems from several factors, including the increasing popularity of mobile banking, the growing demand for personalized financial services, and the need for financial institutions to improve their customer experience.

Regulatory changes in many countries are also supporting open banking and embedded payments.

For example, the European Union's Payment Services Directive (PSD2) requires banks to open their APIs to third-party developers. Leading to a surge in the development of new open banking applications.

Finally, we need to address crypto.

Cryptocurrency and blockchain technology are having a major impact on the fintech industry.

They are enabling new and innovative financial products and the development of services, and they are also changing how financial institutions operate.

Here are some specific examples of how cryptocurrency and blockchain technology are impacting fintech:

Payments: Cryptocurrencies such as Bitcoin and Ethereum can make payments without needing a third party, such as a bank, making payments more convenient and cheaper for consumers.

Investing: Cryptocurrencies can invest in various assets, including stocks, bonds, and real estate, providing investors with more diversification and the potential for higher returns.

Lending: Cryptocurrencies can lend money to others without a traditional bank. Giving borrowers more credit access can also provide lenders with higher yields.

Regtech: Fintech companies can use blockchain technology to develop regtech solutions that help financial institutions comply with regulations. This can help financial institutions reduce compliance costs and improve risk management.

Cybersecurity: Fintech companies can use blockchain technology to develop cybersecurity solutions that protect consumers and financial institutions from cyberattacks.

Overall, the impact of cryptocurrency and blockchain technology on fintech is still in its early stages, but it is growing rapidly.

These technologies can potentially revolutionize the financial services industry and significantly benefit consumers and businesses.

But crypto faces some headwinds.

Here are some of the challenges that cryptocurrency and blockchain technology face in the fintech industry:

Regulation: Cryptocurrency and blockchain technology are still relatively new and are not yet well-regulated in many countries. This can make it difficult for fintech companies to develop and offer products and services that use these technologies.

Acceptance: Cryptocurrencies are not yet widely accepted as a form of payment by merchants. This can make it difficult for consumers to use cryptocurrencies to make purchases.

Volatility: The price of cryptocurrencies is very volatile, making them risky investments and difficult for financial institutions to offer cryptocurrency products and services.

Fraud: There is a risk of fraud associated with cryptocurrency and blockchain technology.

Despite these challenges, cryptocurrency and blockchain technology are still having a major impact on the fintech industry.

These technologies can potentially revolutionize the financial services industry and significantly benefit consumers and businesses.

6. Investor Takeaway

The fintech industry has a long runway ahead of it and many potential investments for savvy investors.

If you are looking for "safer" investments, you have more established players like JP Morgan; if you want cutting edge, you have crypto.

How we manage, spend, and move our money is undergoing a tremendous change, and we are still in the early innings of the changes.

Many changes remain coming to the industry because of the fast-improving tech, i.e., AI, plus the many regulatory changes still to come.

We will likely see a different type of money management in the next 50 years than we have seen for the last 100 years.

Most think cash is dead, which is likely true, but we have a way to go before it finally dies.

The coming fintech revolution will increase access to financial resources than we have ever seen, hopefully improving the global economy and conditions.

Areas like South America, India, and Africa still have a long way to go before reaching saturation of how we bank, which bodes well for those regions' fintech industry and people.

And we didn't even cover the digital currencies coming to governments and how they could impact our uses of money.

The bottom line, there remains a ton to like about the industry, and we remain in the early innings.

As always, thanks for reading, and I hope you found something of value here. If I can further assist, please don't hesitate to reach out.

Until next time, take care and stay safe out there,

Dave

Thank you for reading Dave's work today. We hope it provided you with valuable insights and expanded your understanding.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

Our posts may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

| A guest post by

|