Why does Margin expansion often lead to multiple expansion?

Why does Margin expansion often lead to multiple expansion?

Knowledge exchange with Heavy Moat Investments

After a few discussions with Niklas, who runs

, we’ve decided to launch this Q&A to share knowledge with our subscribers. There are no commitments regarding the frequency; we will simply share our views when time permits. Therefore, comments will be open to everyone to allow fruitful discussions.The question we aim to answer is: Why does margin expansion often lead to multiple expansion?

response:

We believe that margin expansion often leads to multiple expansion because it demonstrates improved operational efficiencies for a company. When a company's margins consistently expand, especially when compared to its peers, it signals a sustainable business model, indicative of a competitive advantage or a 'moat’.

This heightened profitability attracts investors, resulting in increased demand for the company's stock. Consequently, the market assigns a higher valuation multiple to the stock, reflecting the improved potential for future earnings growth. Over time, as future sustainable profits catch up to the higher multiple, the valuation multiple will appear more in line with the quality of the company.

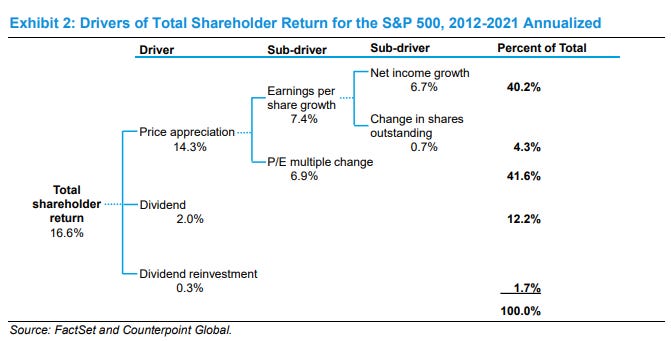

As history suggests (as depicted in the screenshot from the Morgan Stanley article below, which is a recommended read), profit expansion is equally crucial as multiple expansion for the total returns of a stock over the long term. We believe that earnings expansion serves as a signal of optimism, prompting investors to incorporate higher growth expectations into the stock price, thus driving the multiple higher.

Source: Morgan Stanley Investment Management, Total Shareholder Return

Caveats: Investors might get greedy with minor or unsustainable profit expansion, and thus what causes the price to go up will eventually drag it out. So do your research to better evaluate the reasons.

response:

I’ve been researching high quality companies, so called compounders, for over two years. Often over the last decade, these businesses showed:

Stable mid- to high single-digit revenue growth

Margin expansion

Increasing Returns on Capital

Teens EPS growth

20%+ Total return growth

Below we can see the examples of Cintas Corporation CTAS 0.00%↑, IDEXX Laboratories IDXX 0.00%↑ and Mettler-Toledo MTD 0.00%↑.

These businesses crushed the market by pushing all the levers a company has to pull to increase EPS and total returns faster than revenue:

Reducing shares outstanding

Pushing margins

Multiple expansion by the market

The question now arises if these businesses have seen their best days and if the market is rational in pricing them higher.

Answer

It makes sense that the market is willing to put a premium on companies with higher ROIC, a decreasing share count and higher margins. They often demonstrated a long history of outperformance and continual improvement in fundamentals and total returns. It is easy to get drawn into the past and experience FOMO.

The issue is that these companies often already exhausted a lot of the levers they can pull. Improving margins can supercharge returns over a long time. Pushing profit margins from 7.5% to 15% can be easy on a 50% gross margin business, but going from 15% to 30% is pretty hard. Both represent the same amount of leverage on earnings growth.

A similar issue can be observed with share buybacks: As the multiple increases, the buyback yield declines. A company trading at a 5% FCF yield can retire 5% of shares without taking on debt, while a company trading at a 2% FCF yield can only retire 2% a year. This massively reduces the effectiveness of the buyback lever on earnings growth.

Lastly, multiple expansion is a tool that no company can control, but here also, at some point, this becomes a headwind. A company going from a 15 PE to a 30 PE will enjoy tremendous share price appreciation. It is, however, unlikely to go from 30 PE to 60 PE.

To justify its growth based on an inverse DCF model, the company needs to accelerate growth and after these levers are pulled, it needs to come out of organic growth. Often, these businesses already have a strong market position. To accelerate top-line growth, they need to invest more cash, decreasing margins and cash to buy back shares. Sadly, that’s why many great businesses trade at lofty multiples and might not make great investments going forward. It is key for investors to stay rational and not get focused on the past. Only forward returns matter.

If you enjoyed this format and would like to see similar posts in the future, please hit the like button, share your comments, and be sure to subscribe to Niklas's newsletter.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

Our posts may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

| A guest post by

|

Nice answers. Wide margins make cash flows less risky. When margins expand, it is easier to cover fixed costs including interest expenses. They also increase returns on capital and reinvestment opportunities. All of these justify higher multiples.