Zoom: Assessment of Enterprise, Competition, and Valuation

Our analysis will dive into two key aspects: Zoom's progress within the Enterprise and Online business and its strategic positioning across several product segments, notably Zoom Meetings, Phone, and Contact Center. Furthermore, we conduct a revised DCF valuation and a Reverse DCF valuation.

For those seeking to obtain an understanding of Zoom’s business, we recommend to refer to our prior snapshot report on the Company (Zoom Video Communications – Snapshot).

Content:

1. Enterprise Customers

2. Online Customers

3. International Sales

4. Valuation

5. Conclusion

1. Enterprise Customers

Zoom’s enterprise customers are those who are engaged by either a direct sales team, resellers, or strategic partners. Zoom has placed a strong focus on serving the enterprise customers and its success is partly dependent on the Company’s ability to grow the Enterprise segment. This is because enterprise customers tend to exhibit higher switching costs and provide opportunities to sell more products and services (land and expand).

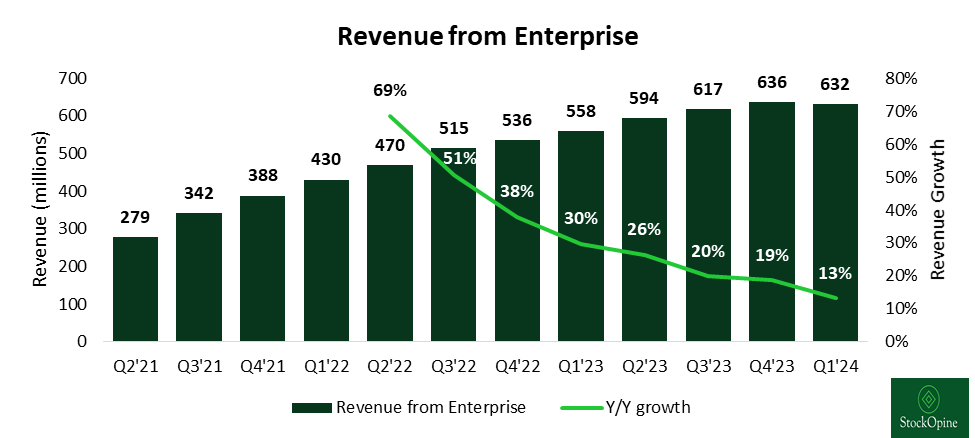

At the outset of the pandemic, during Q1’21 (ending April 2020), enterprise revenue constituted 60% of the Company's total revenue. However, in the subsequent quarter, Q2’21, this proportion receded to 42%, reflecting a surge in usage among online customers which mainly include small and medium-sized businesses (SMBs) and individuals. Since that time, the enterprise segment has been gradually reclaiming its share, contributing to 57% of the total revenue in the most recent quarter, Q1’24.

Source: Zoom Earnings Presentations, StockOpine analysis

In Q1’24, Zoom had $632 million in revenue from enterprise customers, reflecting a 3-year CAGR of 48%, although its growth rate decelerated to 13% year-over-year. Growth in enterprise business was driven by acquiring new customers and by selling more products and seats to existing customers.

Source: Zoom Earnings Presentations, StockOpine analysis

Based on management's guidance for Q2’24, where total revenue is projected to reach $1,113 million at the midpoint and includes online revenue of ~$480 million, it is implied that Enterprise revenue growth for Q2’24 will further decelerate to 7% year-over-year (totaling $633 million), and to a 6% growth rate for the entire year. The deceleration in revenue growth, coupled with concerns about competition, particularly from Microsoft's Teams, stand out as prominent factors deterring investors from the company.

Management has emphasized that the slowdown is not attributed to increased competition, but rather stems from the restructuring of its sales division to focus on upmarket, the staff reduction undertaken in Q1’24, which saw a reduction of 15% in employees and from the current macro environment.

The key changes highlighted by management for the sales division restructuring include:

Restructuring of the Zoom Phone Sales team

Appointment of Graeme Geddes as the new Chief Sales Officer

Hiring a leader in Europe to lead the go to market strategy

Adding more sales reps in the Contact Center team

Looking ahead, management envisions a reacceleration of both online and enterprise revenue as we progress into FY25.

Moving into the broader market of Unified Communication as a Service (UCaaS) we also observe an overall deceleration of growth for 2023 (estimated growth at ~12.5%) as the market saw exponential growth during the pandemic. Additionally, numerous companies downsized their workforce in 2023, optimizing their cost structure, thereby impacting the number of users/seats, and ultimately revenues of the industry.

Looking ahead, the global UCaaS market is poised for substantial expansion, projected to grow from $32B in 2023 to $86B by 2030, at a CAGR of 15%.

On the product side, we observe that the growth of enterprise revenue, in the most recent quarters, is mainly derived from its Phone offering, for which management announced that it exceeded 10% of revenue in Q1’24. Zoom Phone has seen an exponential growth since its launch, surpassing 5.5 million seats in Q4’23 (Jan 2023) which is up from 4 million seats in August 2022 (after Q2’23 – Jul 2022) and 2 million seats in August 2021.

All else equals, this translates to an annual recurring revenue (assuming 10%) of $442M. Assuming 5.8 million seats for Q1’24 (rather than 5.5 million in Q4’23) this will translate to an average $76.2 revenue per seat. If the same revenue per seat is used for August 2022, ARR would translate to $305M representing ~7% of annual recurring revenue.

What do we make out of this? Since Q2’23 until Q1’24, Zoom Phone ARR grew by 45% while Enterprise excluding Phone was relatively flat at ~1%. Although Zoom Phone is growing, the results for the rest of the Enterprise segment are not enticing.

As mentioned earlier, Zoom’s success in growing upmarket and its expansion within its existing client base will be critical in re-accelerating revenue. On that front, it appears that the Company performs well, as customers contributing more than $100,000 in TTM revenue increased by 23% year-over-year showcasing a smoother deceleration in growth. As of Q1’24, those customers represented 29% of revenue, up from 24% in Q1'23 and 20% in Q1’22.

Source: Zoom Earnings Presentations, StockOpine analysis

Speaking of expansion within existing client base; the trailing twelve-month (TTM) Net $ Expansion Rate for Enterprise Customers, which represents how much existing Enterprises customers are spending relative to prior year stands at 112%, meaning that existing customers spend 12% more than the prior year. This compares to, 115% in FY’23, 130% in FY’22, and 152% in FY’21. Assuming that Enterprise revenue growth will decelerate further by the year end, it is expected that the Net $ Expansion Rate will follow.

In the below chart, we compare the TTM Net $ Expansion Rate for Enterprise Customers to TTM Enterprise Revenue growth, aiming to identify the revenue growth that comes from new enterprise customers, which should approximate the incremental rate between the two.

Source: Zoom Earnings Presentations, StockOpine analysis

From the above, we observe signs of stabilization for revenue growth from new customers at high single digits, which is encouraging, although this metric might drop in the next couple of quarters given management’s guidance for FY24.

What contributes to the decline in the net expansion rate of existing customers? The decline might result from existing customers transitioning to alternative providers, such as Microsoft Teams or from internal factors such as the sales division restructuring or reductions in seat numbers due to streamlining of cost structures / workforce reductions by clients. We believe it is a combination of these factors.

If Zoom maintains a rate above ~110% and we observe new clients growth of 5%, it will demonstrate ability to grow in line with the market which is projected to grow by 15%. Any deviation should be closely monitored.

Competition

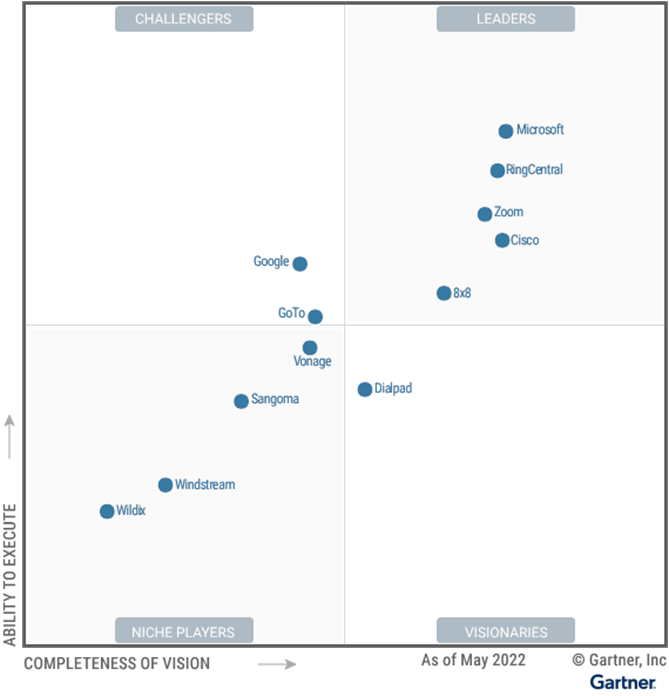

Zoom competes with the likes of Cisco through Webex, bundled solutions like Microsoft Teams and Google Meet whereas on the phone space, Cisco, RingCentral, 8x8 are considered key competitors. On the contact center landscape, the key competitors identified are NICE Ltd through its CXone offering, Five9 (which Zoom attempted to acquire in the past) and Genesys through its Genesys Cloud CX solution. Overall, the complete offering in the collaboration space is Unified Communications as a Service (“UCaaS”) where Zoom appears to be a leading player.

For starters, in November 2022 it was named as a Leader in the 2022 Gartner® Magic Quadrant™ for UCaaS, for the third time in a row while under G2 (a well-known peer to peer review site) Zoom was classified as Leader for UCaaS Platforms, Video Conferencing but appears to be falling behind Microsoft Teams, for VoIP(Voice over internet protocol (VoIP) and although it just started, it is also a leaderfor Contact Center, yet behind a number of its key peers.

Source: Gartner (November 2022)

a. Zoom Vs Cisco

Source: Zoom and Cisco filings, Stratosphere.io (use coupon code STOCKOPINE for a 25% discount), StockOpine Analysis | Note: [1] Q1’24 for Zoom is the respective Q3’23 for Cisco and both are presented as Q1’24 in the above chart so as to allow comparisons [2] Cisco: Collaboration consists of Meetings, Collaboration Devices, Calling, Contact Center and Communication Platform as a Service (CPaaS) offerings.

Running the first peer-to-peer review (below we compare it with Microsoft Teams, RingCentral etc.) it appears that Zoom has outpaced Cisco, widening the gap over the last two quarters. Cisco Webex is mainly used by organizations and a more fair comparison would be against Zoom’s Enterprise revenues. As it can be observed from the above chart, the gap is closing, as Zoom’s Enterprise revenues account for 64% of Cisco’s Collaboration revenues over the past quarter compared to ~24% back in Q2’21 (quarter ended July 31, 2020).

A possible explanation for Cisco’s declining share appears to be the fact that Cisco’s channel partners have also formed partnerships with Microsoft, Zoom and RingCentral. Additionally, Cisco's perceived higher pricing in comparison to competitors (as reported by Gartner) may have contributed to this trend.