Industry overviews are reintroduced as part of our product revamp, and we want to give you a heads-up. This is a high-level analysis where we explore an industry and its peers from a 30,000-foot view, helping you get acquainted with the sector and offering one or two interesting ideas.

For the charts, we're using Koyfin, which you can access at a 20% discount via our affiliate link. Additionally, StockOpine annual paid subscribers are eligible for a 3-month free trial, just shoot us an email.

1. Key Competitors

Diageo (Ticker – DGE): A British multinational alcoholic and non-alcoholic beverage company with a portfolio of over 200 brands. Well-known brands include Guinness (beer), Smirnoff (vodka), Johnnie Walker (Scotch whiskey), and many more.

Pernod Ricard (Ticker – RI): A french producer of iconic alcoholic beverages, including Malibu (rum), Chivas Regal (whiskey), Jameson (whiskey), and Absolut (vodka).

Brown-Forman Corporation (Ticker – BFB): A US-based company that owns some of the world’s largest brands, including Jack Daniel’s (whiskey), Diplomatico (rum), and El Jimador (tequila).

Anheuser-Busch InBev (Ticker – ABI): The world’s largest brewer, headquartered in Belgium, specializing in alcoholic beverages such as beers and soft drinks. Notable beer brands include Budweiser, Corona (outside the U.S.), Natural Light, and Stella Artois.

Constellation Brands (Ticker – STZ): The largest beer importer in the U.S., specializing in beer, wine, and spirits. Constellation owns among others the U.S. and Mexico rights to the Corona brand, as well as Modelo Especial and Pacifico.

Carlsberg (Ticker – CARLB): A Danish multinational brewer with over 670 labels and about 140 brands. Its well-known beer portfolio includes Tuborg, Kronenbourg 1664, Somersby, and more.

Heineken (Ticker – HEIA): A Dutch brewer with over 170 beer brands. Famous brands include Heineken, Sol, Amstel, Birra Moretti, Desperados, and many more.

Note (10 Feb 2025): 1Dkr = $0.14, €1=$1.03, £1=$1.24

2. Market size and forecasts

Statista (published in Feb 2024) valued the global alcoholic drinks market at $1.6 trillion in 2023, projecting a Compound Annual Growth Rate (CAGR) of 5.5% from 2024 to 2028, reaching approximately $2.1 trillion. Meanwhile, ISWR (June 2024) forecasted the global Total Beverage Alcohol (TBA) market to grow at a modest +1% CAGR in both volume and value over 2023-2028.

a. Key Market Drivers & Risks

Premiumization trends remain intact, though slowing, particularly in the premium tier ($22.5 - $30.5 per 75cl bottle). The super-premium segment (+$30.5 per 75cl bottle) continues to grow, driven by millennial and female cohorts.

Non-alcoholic beverages are on the rise. Diageo saw ~56% growth in its non-alcoholic portfolio for 1H FY25, while the global non-alcoholic market increased by 29% in 1H 2024. Projections for the US non-alcoholic market estimate it will reach $5 billion by 2028, with a volume CAGR of 18%.

Headwinds include GLP-1 drugs, changing consumer habits, and tariffs, making the industry's growth outlook uncertain.

With Diageo recently withdrawing its mid-term organic sales growth guidance of 5%-7% and Pernod Ricard revising its growth outlook to 3%-6% for FY27-FY29 (down from 4%-7%), the industry's future is uncertain.

At best, the industry may see flat to marginally positive growth, with non-alcoholic trends and premiumization serving as a defensive buffers rather than strong growth accelerators.

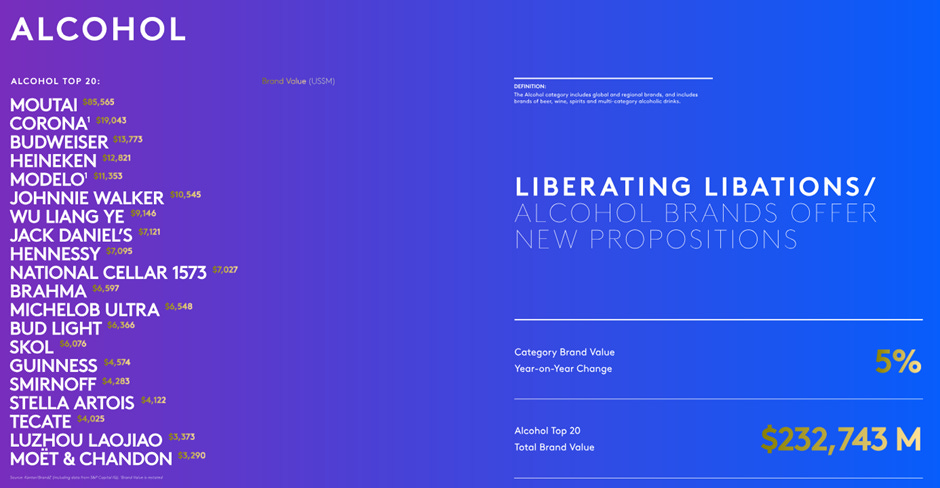

b. Brand Value

Kantar released its 2024 ranking of the top 20 most valuable beverage brands, with China’s Kweichow Moutai leading the pack at a staggering $85.6 billion, far surpassing the rest. Following Moutai, four beer brands made the list, with Corona securing the second spot at $19 billion. Meanwhile, Johnnie Walker ranked 6th with a brand value of $10.5 billion.

Source: Kantar BrandZ Most Valuable Global Brands 2024

To put things into perspective and better understand what each of the seven companies we’re analyzing owns, here’s a breakdown in table form:

As seen, Anheuser-Busch InBev and Diageo have the strongest portfolios in terms of brand value.

c. Industry Developments

Tailwinds

For completeness, key tailwinds include growth in non-alcoholic beverages, new small packaging (Diageo’s "Architecture" concept), that supports moderation and affordability, and premiumization. According to IWSR, the no-alcohol market across the top 15 markets is expected to grow at a +5% volume CAGR (2023-2028), with beer at +6%, wine at +5%, and spirits at +10%. In the US, no-alcohol spirits are the fastest-growing segment within the broader spirits category, with a +60% five-year CAGR through 2024, outpacing the growth of no-alcohol wines and beers.

Headwinds

As previously mentioned, the industry faces several structural headwinds, including GLP-1 drugs, Gen Z’s preferences, and alcohol moderation. According to Bevtrac data, 50% of consumers moderating their alcohol consumption are driven by prioritization of wellbeing, 30% are influenced by economic factors, and 20% by health concerns. Additionally, regulation and tariffs remain key risks for the industry.

During Diageo’s latest earnings call, an analyst raised questions about these structural headwinds and management provided the following insights:

Gen Z (born 1997-2012) shows a preference for moderation, but household penetration is at +3%, with Gen Z adopting moderation faster than Millennials. This is also evident in the trend of "zebra stripping", alternating between alcoholic and non-alcoholic drinks within the same evening.

Beverage companies with strong non-alcoholic portfolios (e.g., Diageo’s 0.0 Guinness) are well-positioned to benefit from this trend.

On GLP-1, Diageo acknowledged that it’s still early to measure its impact. While there’s some data available, they believe it’s difficult to distinguish the effects of GLP-1 from the broader moderation trend that has been ongoing for decades. For premium spirits, where the industry (especially big players) is focused, the impact is deemed minimal.

Tariffs, affect all companies, especially in the tequila and Canadian whisky segments. With 45% of Diageo's US net sales reliant on spirits sourced from these regions, pricing and proper inventory management are crucial. While they might have passed on price increases in the past, it’s uncertain if they can do so at scale again, especially since consumer prices are already quite high.

Additionally, a recent NCSolutions survey found a 36% increase in participation for Dry January this year, and 49% of Americans plan to reduce their alcohol consumption in 2025, marking a 44% increase from 2023. Notably, 39% of Gen Z plans to stay alcohol-free throughout the year, compared to just 19% of Millennials/Gen X and 10% of Boomers. However, given the small sample size of 1,131 US adults, the actual long-term behavior of Gen Z remains uncertain.

Finally, regulation is a growing risk within the alcoholic beverage industry. Many countries have adopted stricter policies on alcoholic beverage advertising, putting increasing pressure on key industry players due to rising costs and administrative burdens.

To conclude, the headwinds facing the industry significantly outweigh the tailwinds, thus investing in these companies comes at a risk. However, it is worth noting that many of these companies are currently trading at their lowest valuation levels.

3. Key Metrics

Revenue Growth

No clear winner emerges, as all companies experienced a decline during COVID followed by a recovery. Over the five-year period, Carlsberg ranks first, having avoided negative territory for an extended time. Although not reflected in the Koyfin chart for the full year 2024, it achieved 2.4% organic revenue growth, outperforming the rest. Heineken follows, benefiting from higher growth, with ABI close behind; both showing more stability but dipping into negative territory recently. STZ ranks fourth, trailing slightly.

Among the rest, Diageo's decline has stabilized, but credit is due to BFB for remaining in positive territory longer than Diageo. Overall, beer companies performed better, further underscored by Diageo’s Guinness, which marked its eighth consecutive half-year of double-digit growth. One reason for the lag in spirits is consumer trade-down behavior driven by economic uncertainties.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Profitability

Although revenue has been volatile, profitability has remained relatively stable for key market players. Constellation Brands leads the competition with a 34% EBIT margin and consistently higher margins over the five-year period, while Diageo follows closely in second place with an approximate 29% margin, though recently declining. The chart also highlights that spirits companies generally have higher margins than beer companies due to premiumization, with BFB and Pernod Ricard following this trend. The exception is Constellation Brands, which, despite having ~75% of its sales in beer, maintains beer margins of ~38%, showcasing clear operational efficiencies.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Asset Turnover

Carlsberg and STZ demonstrated the best recent trends in asset turnover ratio (revenues/total assets), reflecting improved asset efficiency. In terms of rankings, Carlsberg takes the top spot with the highest ratio, followed by Heineken and Brown-Forman. Diageo ranks fourth, showing better asset efficiency than five years ago but still at a modest 0.4x.

One limitation of this ratio, without deeper analysis, is that companies investing heavily in acquisitions may see their asset base grow without a proportional increase in revenue, while subsequent impairments (though indicative of poor capital allocation) can artificially boost the ratio. This is why observing trends over time is key to a proper assessment.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Annual Premium Members! Get a 3-MONTH FREE Koyfin trial ($147 value—covers your StockOpine subscription!). 🎁

Email info@stockopine.com to claim it!

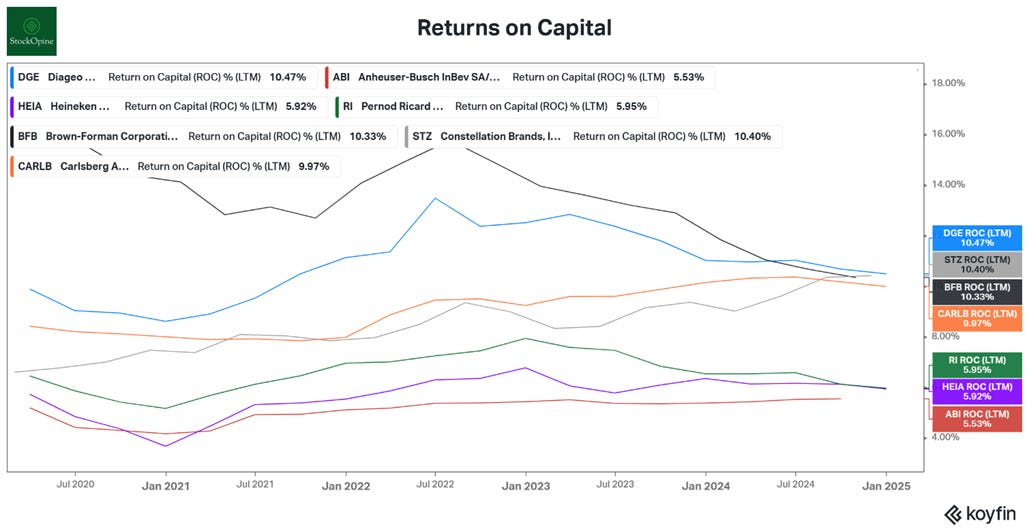

Returns on Capital

As noted in our previous industry overviews, Return on Capital (ROC) is, in our view, one of the most critical metrics for assessing a company's ability to convert capital into profit and a strong indicator of capital allocation efficiency. On a last-twelve-month basis, Diageo ranks first with a ROC of 10.5%, an improvement from five years ago. While BFB’s ROC is similar at 10.3%, its declining trend, aligned with falling profitability and asset turnover, raises concerns, placing it second. STZ and Carlsberg follow, both showing a promising upward trajectory.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

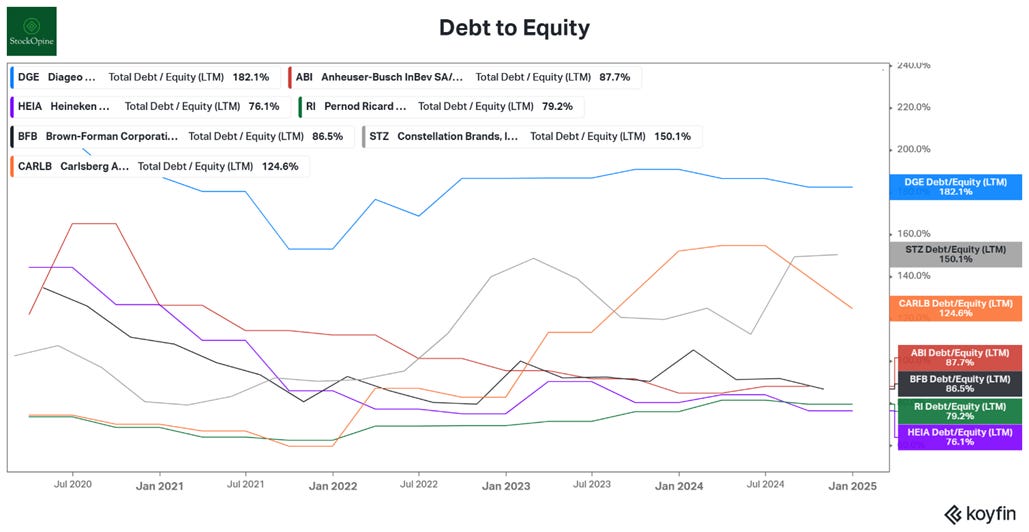

Debt to Equity

Diageo has the highest debt-to-equity ratio among peers at 182%, posing the greatest financial risk. This increases the likelihood of a dividend cut, though the company recently announced it would keep dividends flat, while also halting share repurchases in the last half. Another risk is the potential need to dispose of assets to fund growth or acquire new brands. This is why rumors about possible sales in Guinness and stake in Moët Hennessy (which management denied, fortunately, given Guinness' strong growth) generated some optimism among investors.

On the other end, Heineken holds the best position, with a steady decline in leverage over the past five years, now at 76%. It is followed by Pernod Ricard (RI), which has maintained a stable leverage ratio at 79%. BFB and ABI rank third and fourth at 86.5% and 87.7%, respectively, both showing deleveraging from five years ago.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Valuation

Using the EV/EBITDA metric, which indicates a business's relative valuation, we see that the industry is trading well below its 5-year average EV/EBITDA (NTM) due to the overall alcohol moderation trends. Carlsberg has the lowest multiple at 7.5x (not shown in the chart due to Koyfin’s limitations) compared to its 5-year average of 10.4x, while Brown-Forman has the highest ratio at 13.6x but also the largest deviation (10.8x) from its 5-year average of 24.4x.

As this analysis looks at the ratio in isolation, since factors like moat, financial health, and earnings quality are assessed in the metrics we looked earlier, we rank them based on deviation from their 5-year average. BFB ranks first with a 10.8x deviation, followed by STZ at 5.2x (15.4x – 10.2x), RI at 4.6x (15.8x – 11.2x), and Diageo at 4.3x (17.3x – 13x).

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Estimated EPS growth

Finally, we examine analysts' EPS growth expectations over the next five years. While the chart reflects how expectations have evolved over time, the key focus is on future growth. Based on the latest estimates, Carlsberg leads with 10.5%, followed by ABI at 9.7%, STZ at 9.1%, and Heineken at 8%.

On another note, spirits companies like Diageo and Brown-Forman, which previously faced negative and declining growth expectations, are now seeing upward revisions, whereas Pernod Ricard remains a laggard.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

4. Total score & Conclusion

Note: In each category, we assign 3 points to the top-ranked company, 2 points to the second, 1 point to the third, and 0.5 points to the fourth. Equal weighting is applied across all categories to mitigate personal biases, except for Returns on Capital, which we consider one of the most critical ratios in assessing a company. Therefore, we've doubled the score for this metric.

Based on our findings, there is no clear-cut winner among Diageo (DGE), Brown-Forman (BFB), Constellation Brands (STZ), and Carlsberg (CARLB). However, if we had to highlight one company for further analysis, it would be Carlsberg, as it ranked first in three metrics and showed an improving trend in Returns on Capital, narrowly trailing the top performers.

At StockOpine, we conducted a deeper dive into Diageo. If you're interested in learning more, here are a couple of links that might be of interest.

Did you enjoy this overview? Let us know in the poll.

A top down analysis is not sufficient. Large listed companies are global, not U.S. only.

liquor is a very region business. a brand's strength various across different regions. Also, different regions have different demographics and culture both drive demand. lastly, distribution is super important as well. Johnnie Walker is more a mid class drink while luxury in Latin America. Cognac XO sales are stronger in Asia than in the U.S..

besides, Canadian whiskey and tequila are made inside of the countries not just the raw material.

Sometimes when things look bleak there are opportunities. Perhaps there will be activists or consolidations (mergers) that may occur.

It wasn’t that long ago that Brown Forman fought against an offer.

Plus, we don’t know the long term side effects of GLP-1 or at least I don’t. Although, I don’t mind reading about people drinking less.

Excellent article.