The Art of Position Sizing: Inside the StockOpine Framework

How we balance high conviction, risk management, and the flexibility needed to capture long-term winners.

A premium subscriber recently asked how we think about position sizing. While stock selection gets all the glory, portfolio construction is often what determines long-term performance.

At StockOpine, our primary objective is to own high-quality winners for the long term within a focused portfolio of roughly 20 companies. This number isn’t arbitrary. It’s based in academic research by Elton and Gruber (1977), who showed that a randomly selected portfolio of about 20 to 30 stocks eliminates most unsystematic (company-specific) risk.

According to their findings, a 20 stock portfolio carries total risk only about 28% above the minimum achievable level (a stock portfolio with 3,290 securities). That gap narrows to roughly 20% with 28 securities and about 10% with 60 securities. The takeaway is that the marginal benefits of diversification decline rapidly, while the effort and cost required to monitor additional holdings increase significantly.

However, position sizing is not an exact science. It is a continuous balance between conviction and humility. The recent market swings have prompted us to re-examine our rationale, acknowledge its limitations, and consider where increased flexibility might offer an edge.

1. Why Sizing Matters

Before diving into our rules, it is important to understand why we don’t just buy an index or stick rigidly to one factor. Investment styles tend to move in cycles, alternating between extended phases of outperformance and underperformance.

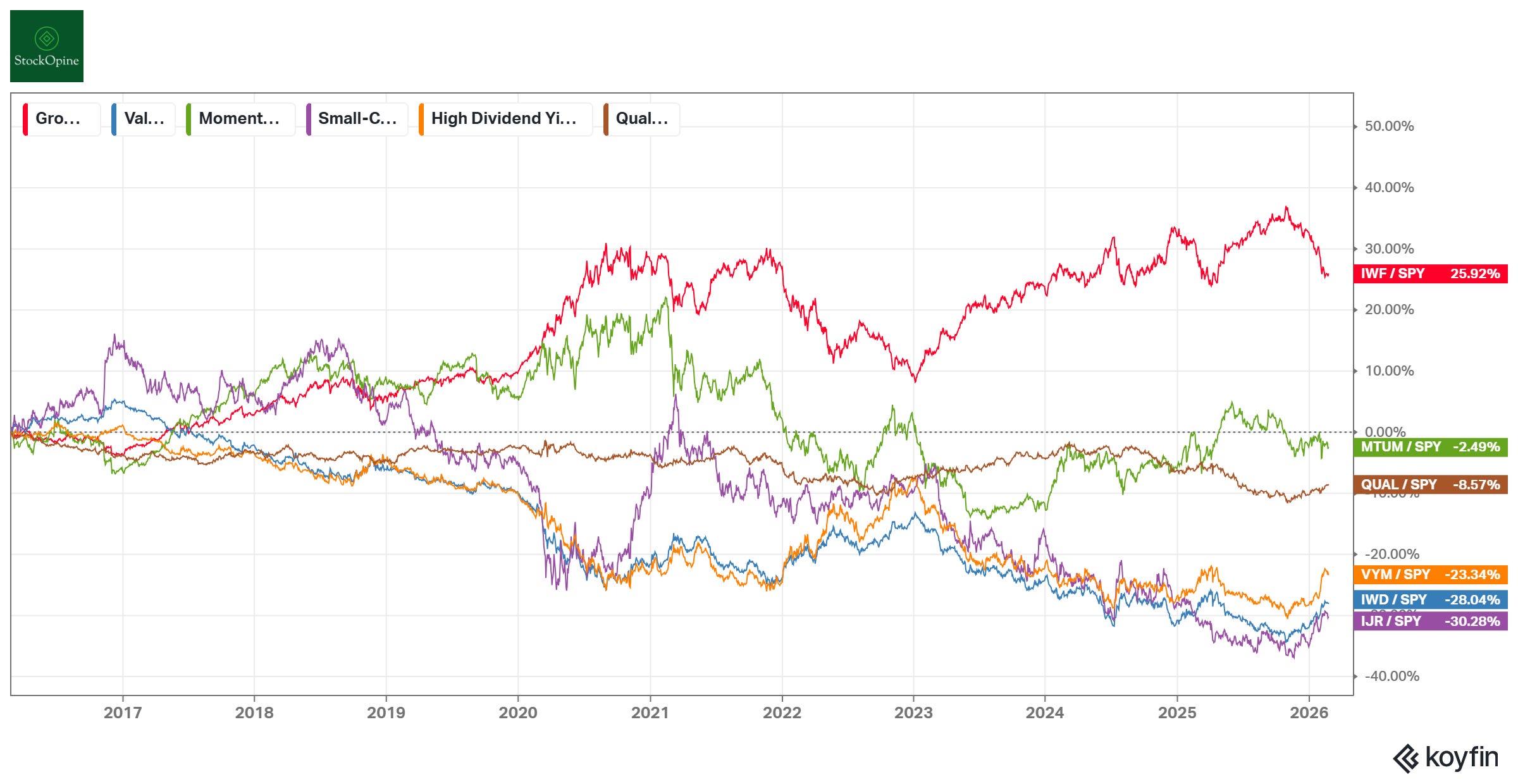

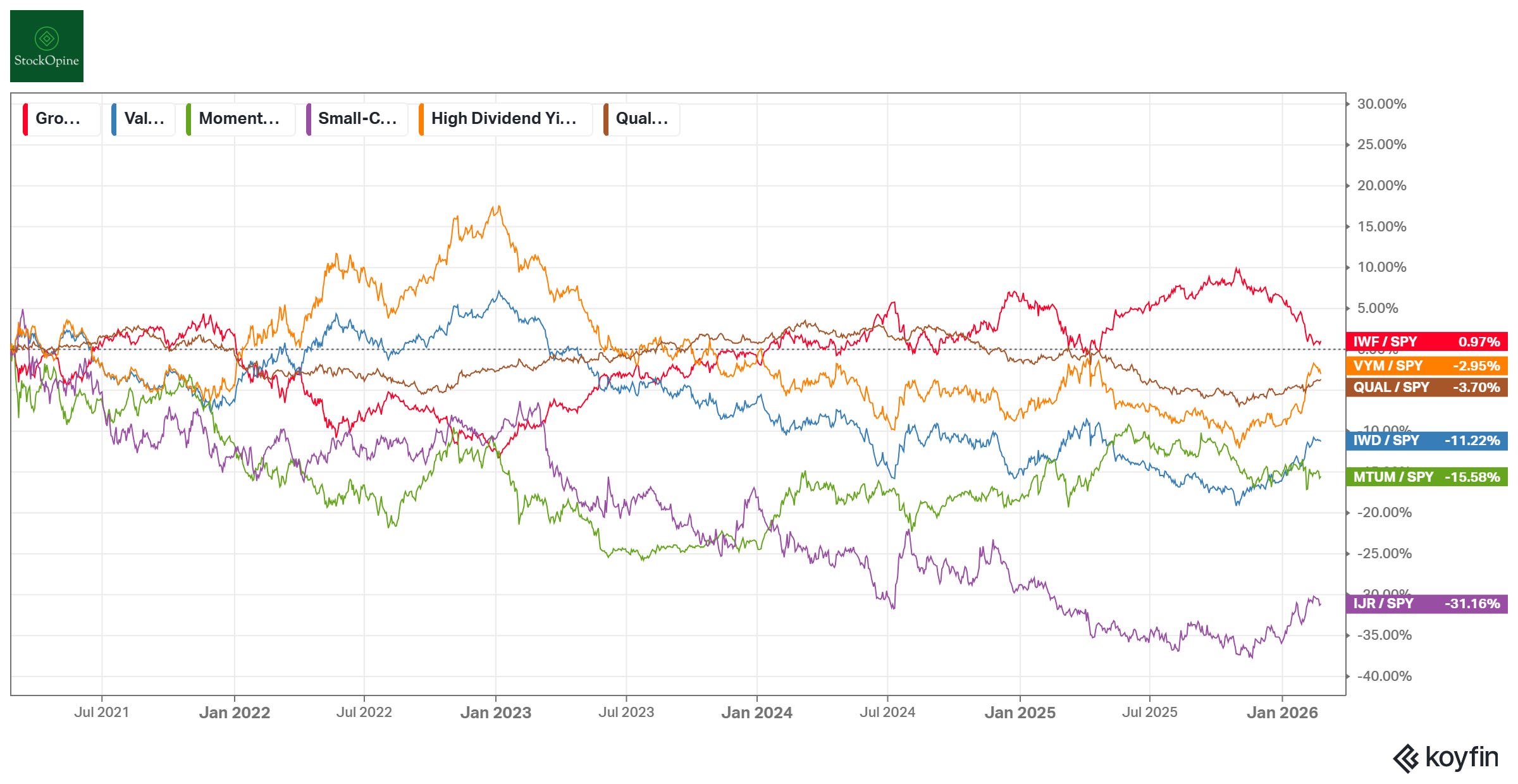

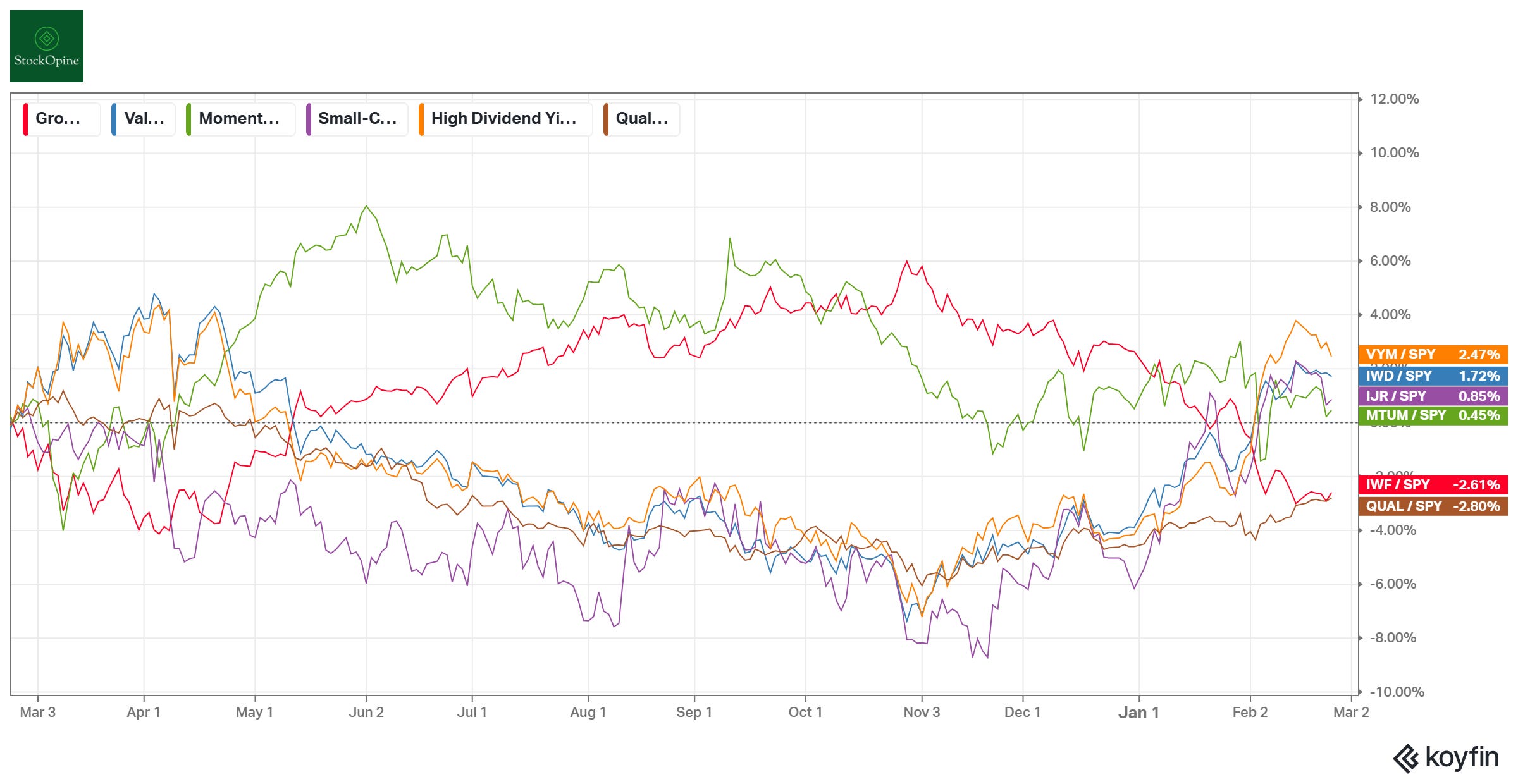

As illustrated by the Koyfin charts below showing various factor ETFs against the S&P 500 (SPY) over 10-year, 5-year, and 1-year horizons, no single strategy wins all the time. Growth dominates over the decade, but value and momentum have their distinct periods to shine. Because the market tide shifts, picking the right winners and managing their weight in the portfolio is important.

10-Year Horizon

Over the last decade, Growth (IWF) has significantly outperformed, while small-caps and value have lagged.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

5-Year Horizon

The 5-year view shows more variance, with recent dips in growth bringing it closer to the average.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

1-Year Horizon

In the short term, the picture is messy. Different factors fight for outperformance, highlighting the difficulty of relying solely on broad factor exposure.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Given this variability, here is how we currently approach sizing, and how we are thinking about evolving it.

2. The Initial Entry: Conviction Vs Bias

When we complete our analysis on a new company, we typically aim for a starting position of 3% to 5%. This depends on our conviction level derived from financial metrics (growth, earnings quality, ROIC), Total Addressable Market (TAM), management quality, and valuation.

If a company is a clear quality compounder, we start with at least 3%.

For turnover stories or mean reversion expectations, where the range of outcomes is wider, we start lower. (e.g., we started Leslie’s at 2%, and unfortunately, even adding 1% later proved to be a poor decision).

Additionally, we apply a ‘cooling-off period’ after deep research to counteract recency bias (the tendency to be overly optimistic just because you just spent hours studying the bull case). Starting at 3% allows us to have ‘skin in the game’ while reserving the right to watch an earnings call or two to confirm our thesis before scaling up.

3. Managing the Position: Adding on Weakness and Strength

Once a stock is in the portfolio, fundamentals and price action impact our next moves, but only within strict limits.

Adding on Weakness (but aiming to avoid the “Falling Knife”): If a high-conviction company’s stock price falls due to short-term issues, we are attracted to buying more. However, we have a theoretical limit that a single position should not exceed 8-10%* of invested capital at cost. At some point, you have to step back. This prevents catastrophic losses if the thesis is fundamentally broken and we were wrong.

*Exceptions: Mega-cap compounders like Google and Amazon have historically held very high weights in our portfolio because they earned this right through sustained, proven execution.

Adding on Strength: We are also willing to average up (as we did with Booking, Alphabet, and Amazon). If a company’s execution and economic moat prove stronger than our initial expectations, we will add to the position even if the share price has increased. That said, once a holding exceeds 10% of the portfolio, we typically stop adding and allow it to run, provided the fundamentals remain intact.

4. The Art of Selling: Why We Might Trim Instead of Exit

Selling is harder than buying. We focus on clear red flags: a thesis that deteriorates over a two-year period, weak communication (withdrawing guidance, repeated overpromising), or chronic operational underperformance. These were the reasons we exited positions such as Diageo, Lululemon, Reckitt, and Rentokil.

That said, not every setback warrants a sale. We try to distinguish between structural and temporary factors. For example, we held Evolution through EU regulatory fencing issues and Asia cyberattacks, and Greggs during its heavy investment phase. Short-term noise is different from long-term erosion.

We have also learned that selling purely on valuation can be costly. We bought KLA around $300 in 2022 and sold near $900 in 2025 because it appeared expensive. Today, it trades close to $1,500.

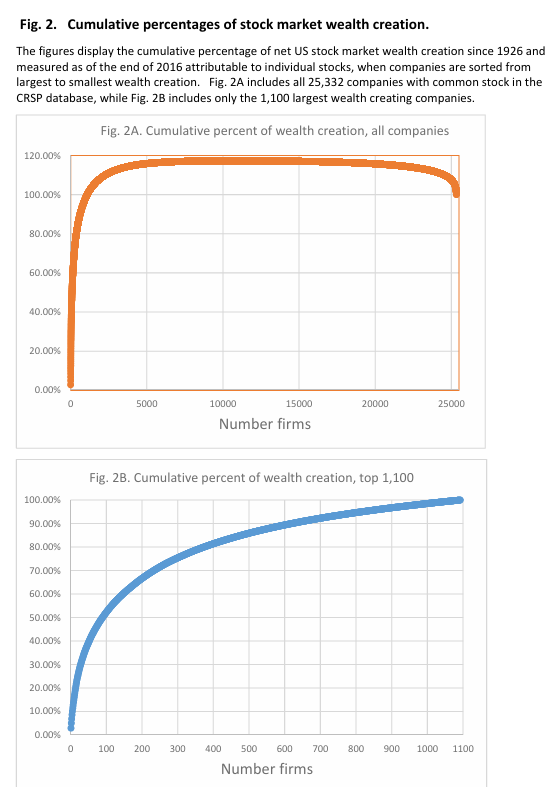

The data supports this lesson. A 2018 study by Professor Hendrik Bessembinder found that just 4.3% of U.S. listed companies (top 1,092 firms) from 1926 to 2016 generated 100% of net wealth creation above Treasury bills. The remaining ~96% collectively matched the return of risk-free bonds (9,579 firms (37.81%) generated positive lifetime wealth, but their gains were fully offset by the wealth destruction of the remaining 14,661 firms (57.88%)).

Source: Do Stocks Outperform Treasury bills? - Hendrik Bessembinder - May 2018

Therefore, fully exiting a high-quality compounder because the valuation feels stretched risks eliminating one of the rare companies that drives long-term portfolio returns. That’s why we now prefer trimming over full exits.

When AMD quickly grew from a 5% to 8% position, we reduced exposure to manage risk but retained a core 5% holding to participate in the AI upside. Trimming protects capital; maintaining a core position preserves asymmetry.

5. Future Evolution: The Case for Flexibility (The Peter Lynch Approach)

Sticking rigidly to 20 stocks means that to add a new idea, an existing one must be sold. This can lead to passing on a great new idea just to avoid cutting a solid existing holding.

We are considering an approach similar to that used by Peter Lynch. While managing the Fidelity Magellan Fund from 1977 to 1990, Lynch delivered a 29.2% annualized return. At times, he held hundreds, even over 1,000 stocks. Many of these were very small positions, often initiated to monitor a company more closely, with capital scaled up only as conviction strengthened and the thesis proved correct.

We see value in being flexible enough to expand our holdings to 25 or even 30 companies by introducing smaller “starter” positions (e.g., 1.5%). Why? Because we missed meaningful opportunities in stocks like Micron (pitched at $117, now $418) and Teradyne (pitched at $69, now $329) simply because the portfolio felt “full.”

A 1.5% starter position creates optionality. If the thesis proves wrong, the impact on the portfolio is limited and easily absorbed. If it develops into the next Micron, that small initial allocation can meaningfully enhance overall returns.

This framework acknowledges that we won’t get everything right, but it also ensures we don’t exclude the next great compounder due to artificial capacity constraints.

Excellent article packed with insights! The midas touch for me was the last part about considering a move to a Lynch style portfolio via small starter positions. The willingness to try out new ideas shows both mental flexibility and ambition to improve which I believe are key traits to long term success in the markets 👍🏻 Coincidentally, I have also open up to the idea of small starter positions where previously I was dogmatic about a full position. 😁