We outperformed the index in Q2, a small but meaningful step toward our long-term investing goals. This wasn’t by chance. At the start of the quarter, we believed our portfolio was fundamentally stronger than the index and saw no need for changes. That conviction paid off.

On June 24th, however, we made a deliberate adjustment: exiting one position and entering another that appeared deeply undervalued. As Q3 began, we also initiated a stake in a high-quality compounder and topped up a stock we believe has been unfairly beaten down. We’ll elaborate on these moves shortly.

These trades are part of our ongoing effort to refine the portfolio’s risk/reward profile and ultimately, compound outperformance over time.

Before diving into the Q2 2025 Portfolio Update, here’s a quick recap of the long-form articles and stock ideas we shared this quarter, in case you missed anything!

Stock ideas

Deep Dives

1. Tariffs - still in play

Uncertainty around tariffs continues, and trying to predict the outcome seems futile given the recent moves (letters to Japan, South Korea) and the pause extension from July 9 to August 1. The Vietnam agreement is a positive, 20% tariffs on most exports, 40% on transshipped goods, but China remains the big unknown.

With that, let’s move on to performance, portfolio insights and the rationale behind this quarter’s moves.

2. Portfolio Performance

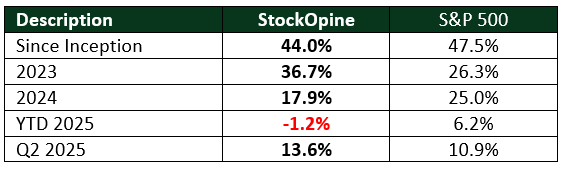

As of June 30, 2025, our Q2 return was +13.6%, outperforming the S&P 500 by 270bps (10.9%). While we’re still trailing the index YTD (-1.2% vs. +6.2%), largely due to a tough Q1, our worst since StockOpine began, we’re encouraged by the strong rebound this quarter.

Since inception (Jan 28, 2022), our portfolio has delivered a cumulative return of +44.0% (annualized +11.3%), versus the S&P 500’s +47.5% (annualized +12.0%). We're narrowing the gap, and we believe the recent portfolio additions position us well to outperform over the long term.

Source: S&P Dow Jones Indices, Broker, StockOpine analysis

3. Portfolio Insights

We recently introduced the following metrics to help evaluate the quality of our holdings and identify underperformers. You can refer to this article for the rationale of using each metric.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers), StockOpine analysis

Our portfolio continues to meet the minimum quality thresholds we’ve set, though there’s been some minor deterioration in valuation metrics compared to the previous quarter. On the positive side, return on invested capital (ROIC) improved by 40bps.

When stacked against the S&P 500, our portfolio currently lags in headline metrics like profitability (25.9% vs. 26.9% for the index), ROIC (21.4% vs. 23.2%), and revenue/EPS growth (9.2% and 12.7%, respectively). But we’re not concerned. These figures still reflect a high-quality portfolio, and we believe the businesses we hold are well-positioned for long-term compounding.

What gives us even more confidence is the relative upside potential: our portfolio has a 4.1% free cash flow yield versus 2.7% for the index, and trades at an EV/EBITDA multiple of 18.2x which is about 18% lower than the index.

This quarter, we went a step further by introducing a simple scoring system to give a quick snapshot of each holding’s quality, purely based on four key financial metrics:

EBIT margin for profitability

ROIC for capital efficiency

5-year EPS CAGR for growth, and

FCF/EV yield for valuation

Each metric is scored on a scale:

0 if the result is below 70% of our threshold

0.5 at 70%

1.0 at 100%

1.5 if it exceeds 130% (and capped there)

This doesn’t capture everything, especially intangible factors like brand strength, leadership quality, or companies in transformation phases. But it's a useful starting point for spotting strengths and weaknesses at a glance.

It’s not the full picture, just a lens to begin with.